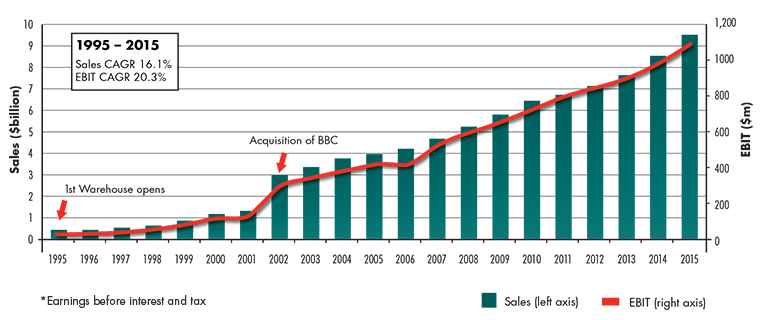

Buoyant trends in residential building investment, an improving outlook on household discretionary income and growth in the number of households have supported the growth in the Hardware and Building Supplies Retailing industry over the past five years. This growth is also a function of consumer choice for DIY home improvement renovations and repairs. Bunnings (as subsidiary of Wesfarmers) was an early entrant to this industry (1994) and is now the leading retailer in this sector. Approximately 15 years later Woolworths decided they wanted to be part of this growth industry and partnered up with US based Lowes Companies Inc (who were experienced and had significant success in this industry) in a JV called “Masters”. Unfortunately 5 years into the strategy Woolwoorths have pulled the pin on the operation and in turn Lowes have exercised a put option on the JV to exit. This is a story of an extremely successful retailer failing in a growth industry primarily because of aggressive expansion plans on an unproven concept with underwhelming locations.

Master’s has been a drag on Woolworths for a number of years with rollout costs exceeding expectations and sales underwhelming to say the least. From a credit perspective the failure of Masters was the primary reason why Standard and Poors downgraded the credit rating of the group in August 2015. Woolworth was spending so much time trying to fix this business model that it took it eye off the prize and was loosing market share in food retailing. This led to a number of profit downgrades and subsequently the now downgraded rating was put on negative outlook again. Woolworths’ lease-adjusted debt to EBITDA is expected to reach 3.2x exceeding the 2.8 or 2.9 times needed to maintain it current rating. Following the announcement of a divestment of Masters S&P made no change to its BBB+ ratings or negative outlook but noted that the divestment of the unprofitable venture was favourable to Woolworths’ credit profile. The credit rating agencies are now more concerned with the performance of Woolworths’ Supermarkets division than Masters and given there is still no update on a new CEO the long term direction of the company is still uncertain. Theoretically a closure of Masters should be beneficial for Bunnings. The problem is Masters is too small to make any difference to the performance of Bunnings. So what does Wesfarmers do? They expand into the UK market by entering into an agreement to acquire Homebase (the No 2 Home Improvement player in the UK). The intention is to rebrand the business as Bunnings and refurbish the entire store network. This move was also a little concerning to Standard and Poors because they “do not believe the funding plan adequately mitigates the financing risks associated with this transaction. The adjusted debt load will increase by about A$2.5 billion. We therefore expect that Wesfarmers’ debt to EBITDA will be about 2.75x and funds from operations (FFO)-to-debt will be about 26% in fiscal 2016, before improving to the bottom of our expectations for the rating in fiscal 2017.” Ultimately Wesfarmers has stretched the borrowing a little to far for S&P to be confident that they wont be backed into a false sense of security again (like with Masters). The concerns stem from the group’s existing debt facilities in conjunction with significant off-balance-sheet operating leases will impact key credit metrics. Wesfarmers’ need to keep A) debt to EBITDA below 2.5x or below and/or B) FFO to Debt to below 28%. Although this negative outlook is not ideal for the group it is too early to make the call on whether Wesfarmers will be successful in implementing the Bunnings strategy in the UK. We are more inclined to watch the local battle between Coles, Woorworths and ALDI play out because this is still the main game in terms of credit worthiness.

Master’s has been a drag on Woolworths for a number of years with rollout costs exceeding expectations and sales underwhelming to say the least. From a credit perspective the failure of Masters was the primary reason why Standard and Poors downgraded the credit rating of the group in August 2015. Woolworth was spending so much time trying to fix this business model that it took it eye off the prize and was loosing market share in food retailing. This led to a number of profit downgrades and subsequently the now downgraded rating was put on negative outlook again. Woolworths’ lease-adjusted debt to EBITDA is expected to reach 3.2x exceeding the 2.8 or 2.9 times needed to maintain it current rating. Following the announcement of a divestment of Masters S&P made no change to its BBB+ ratings or negative outlook but noted that the divestment of the unprofitable venture was favourable to Woolworths’ credit profile. The credit rating agencies are now more concerned with the performance of Woolworths’ Supermarkets division than Masters and given there is still no update on a new CEO the long term direction of the company is still uncertain. Theoretically a closure of Masters should be beneficial for Bunnings. The problem is Masters is too small to make any difference to the performance of Bunnings. So what does Wesfarmers do? They expand into the UK market by entering into an agreement to acquire Homebase (the No 2 Home Improvement player in the UK). The intention is to rebrand the business as Bunnings and refurbish the entire store network. This move was also a little concerning to Standard and Poors because they “do not believe the funding plan adequately mitigates the financing risks associated with this transaction. The adjusted debt load will increase by about A$2.5 billion. We therefore expect that Wesfarmers’ debt to EBITDA will be about 2.75x and funds from operations (FFO)-to-debt will be about 26% in fiscal 2016, before improving to the bottom of our expectations for the rating in fiscal 2017.” Ultimately Wesfarmers has stretched the borrowing a little to far for S&P to be confident that they wont be backed into a false sense of security again (like with Masters). The concerns stem from the group’s existing debt facilities in conjunction with significant off-balance-sheet operating leases will impact key credit metrics. Wesfarmers’ need to keep A) debt to EBITDA below 2.5x or below and/or B) FFO to Debt to below 28%. Although this negative outlook is not ideal for the group it is too early to make the call on whether Wesfarmers will be successful in implementing the Bunnings strategy in the UK. We are more inclined to watch the local battle between Coles, Woorworths and ALDI play out because this is still the main game in terms of credit worthiness.