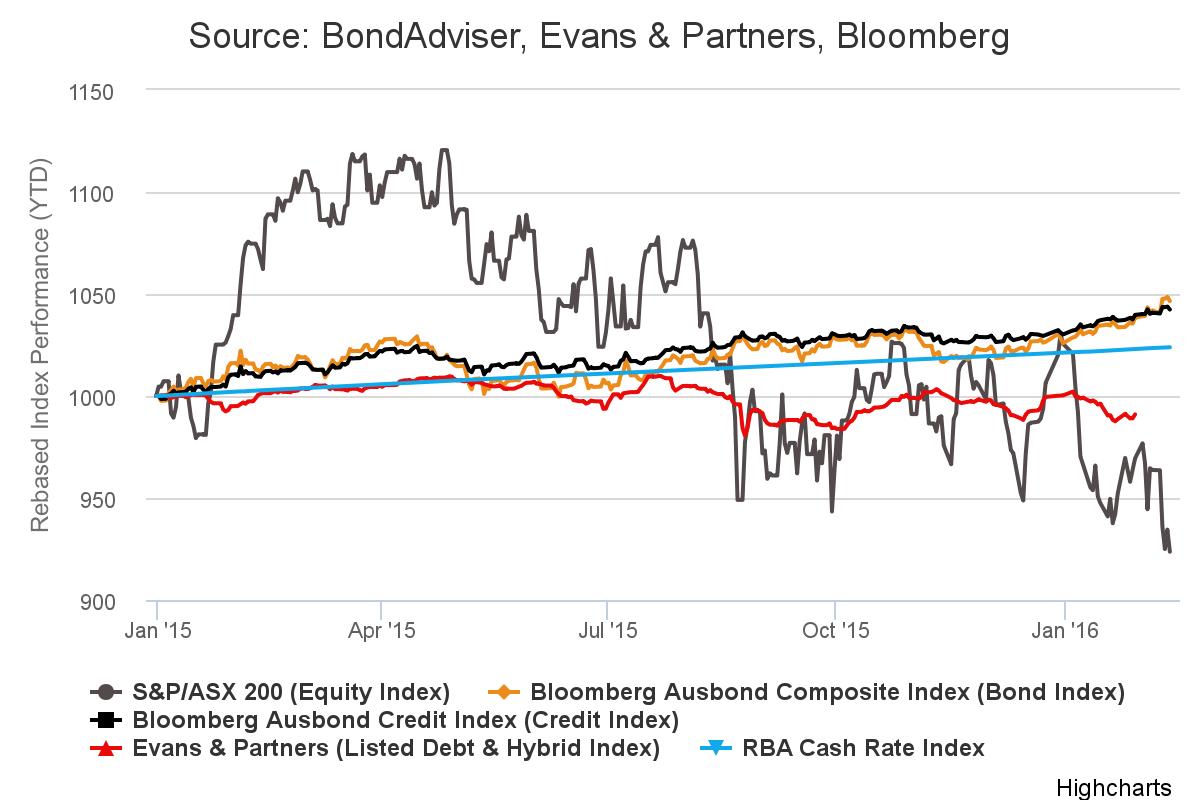

Last week was dominated by another wave of negative sentiment towards equity markets as the ASX200 closed the week down 4.16% (fell from 4,976 to 4,765 points) while the flight to quality saw the Bloomberg AUSBond Composite Index up 0.44%. Year to date the bond index has outperformed equities by 11.96%. The brunt of the selling was felt by the banks (and Macquarie) despite reasonably positive reporting from the Commonwealth Bank. This is primarily a result of what is happening to their international peers and their reliance on foreign capital. This means that the international cost of new debt is increasing which will put pressure on net interest margins which will dampen future profits. Hybrids: The Street Talk section in the Australian Financial Review (AFR) reported Goldman Sachs along with CommSec are in pole position to arrange the hybrid transaction to replace the Commonwealth Bank’s (CBA) PERLS III (ASX Code: PCAPA) $1.166 billion issue expected to be called on 16 April 2016. It will be interesting to see how seasoned investors in this market react to the initial price guidance as most of the Additional Tier 1 (AT1) hybrids issued by the four major banks (Basel III compliant) are trading significantly below the initial offer price. As a good starting point investors considering any new issues should be looking where existing 3, 4, 5, 6 & 7 year hybrids are trading in the secondary market as a guide to determine whether any primary issuance premium exists or not. This transaction has the potential to set the tone for the Australian hybrid market for the remainder of 2016. In market news the Western Australian Government is expected to announce the privatisation of the states wagering operation this week. This is the last state owned betting agency to be privatised with Tatts and Tabcorp dominating the existing landscape. The bidding is expected to be strong as both of these issuers have sufficient liquidity and solid balance sheets to take advantage of this opportunity

Reporting Season We are now approximately 25% through reporting season with company revenue growth showing resiliance but earnings have been varied. The industrial and consumer sectors have showed disappointing results whereas utilities have surprised to the upside. Key findings from our universe are below: Suncorp Group – Since restructure to a non-operation holding company (NOHC) in 2011 the Suncorp Group (SUN) has gone from strength to strength. However, the situation today is similar to the pre-GFC era where it is difficult for a regional bank to be competitive against the majors in mortgage lending. Over the past few years they have been successful in improving their net interest margins but going forward it will be much more difficult to consistently improve margins without taking more underwriting risk. This will be challenging given the uneven regulatory framework, however the gap is closing. From a credit perspective the group has diversified income streams, it remains well capitalised and has a strong reinsurance program. Goodman Group – Goodman Group’s (GMG) first half result was strong with an operating profit before interest and tax of $452.3 million up 28% on the prior corresponding period. All divisions contributed but the development and asset management segments were the standout performers with reported EBIT growth of 39% and 66% respectively. The investment segment remains the largest contributor (43%) but growth was limited to 5.3% as the timing of asset sales impacted income over the period. Capitalisation rates continue to grind tighter (from 7.0 – 6.6%) meaning revaluation gains on the portfolio exceeded $600 million. Mirvac continues to have a strong business profile and a healthy pipeline of new developments and projects. Although the results for the first half of financial year 2016 were somewhat disappointing (although in line with expectations), the group expects operations to improve as non-strategic asset sales are finalised and a significant skew of residential settlements are realised in the second half of the year. AGL Energy has proven its ability to manage its balance sheet while optimising growth opportunities when they arise. Current energy market prices are making exploration and production very complex and a number of projects are arguably no-longer viable. In terms of their core operations demand for electricity on the National Electricity Market (NEM) looks to be improving (at least in the short term) which should allow AGL to benefit from increased generation capacity. The Commonwealth Bank of Australia reported statutory net profit of A$4.618 billion for the first half of 2016 (up 2%). Net mortgage lending growth was 6.5% (below system growth of 7.7%) over the period while the net interest margin remained at 2.06% (flat for the half but down 0.05% on the year). This result is broadly credit neutral, with all divisions contributing. 15/02/2016 – Aurizon (1H16) 15/02/2016 – Bendigo & Adelaide Bank (1H16) 16/02/2016 – Cash Converters (1H16) 16/02/2016 – Challenger (1H16) 16/02/2016 – NAB (Trading Update) 17/02/2016 – ANZ (Trading Update) 17/02/2016 – Coca Cola (FY15) 17/02/2016 – DEXUS (1H16) 17/02/2016 – Vicinity (Formerly Federations Centres) (1H16) 17/02/2016 – IAG (1H16) 17/02/2016 – Lend Lease (1H16) 18/02/2016 – AMP 18/02/2016 – Tatts (1H16) 18/02/2016 – Origin (1H16) 18/02/2016 – Telstra (1H16) 18/02/2016 – Sydney Airport (FY15)

Click below for Interactive Charts Chart 1: Bloomberg AUSBond Composite Index (Monthly) Chart 2: Bonds vs Equities 2014/15 (Monthly)

Interest Rates As stated last week interest rate expectations remain in a state of flux. The US Federal Reserve is facing increasing pressure from interest rate markets to adjust down its plan for future interest rate rises. However, there is no guarantee policy makers will change their position and hence volatility is likley to persist in the short term. Some of this uncertainty was resolved late last week in the Federal Reserve Chairman’s address to Capitol Hill but there is now news flow about negative interest rates and further quantitative easing. While this may be fact in some countries we don’t think the US will reverse its policy decision in the short term. The RBA continues to sit on the fence and follow the trajectory of employment, credit and inflation data. In his statement to the house of representatives last week Governor Stevens gave a relatively ambiguous testimony simply stating the obvious about deteriorating terms of trade and broad market volatility. As they have stated many times before the Reserve Bank board retains the “flexibility to ease policy” in the right circumstances. In February 2015, the 10-year bond yield hit an all-time low of 2.27% before lifting to highs near 3.15% on 11 June 2015. In early November 2015 there was a progressive increase in yield from ~2.60% to a high of 2.99%. However, since mid-December the flight to quality has meant the 10-year yield has given back the changes in Q4 2015 and on 11 February 2016 hit a 6 month low of 2.37% (current 2.47%). The 3-year bond has followed a similar pattern and broke out of its recent yield range (1.90 – 2.1%) in November/December 2015 reaching a high of 2.18% on 7 December 2015. It has now retraced back to 1.80%. On 12 February 2016, the ASX 30 Day Interbank Cash Rate Futures March 2016 contract was trading at 98.045 indicating a 19% expectation of an interest rate decrease to 1.75% at the next RBA Board meeting (unchanged from the previous week).