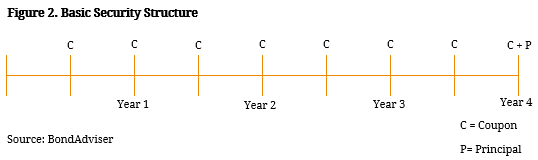

The fixed income asset class is the broad classification for debt securities that pay a specified distribution over a defined period. A fixed income security is always issued with a specified face value called the principal. Over the life time of the security, an investor will receive periodic interest payments and repayment of face value at maturity. As a result, the investor is effectively lending capital to the issuer in return for interest, similar to a mortgage between a bank and a homeowner. For example, holders of a 4 year fixed rate security that pays interest semi-annually will receive 8 periodic interest payments over the security’s life time. At the end of the 4-year period the investor will be repaid the principal. Figure 1. Basic Security Structure  The above example illustrates a fixed income security in its simplest form. However, security structures can vary significantly depending on different features. Features that define the structure of a fixed income security include its type of interest payment (floating, fixed, inflation-linked), the interest payment amount (which is linked to the credit quality of the issuer), its term (perpetual, callable or fixed term) or its position on the capital structure (secured, unsecured or subordinated). Additionally, fixed income is generally defined by the underlying issuer – Government, State Government or Corporations.

The above example illustrates a fixed income security in its simplest form. However, security structures can vary significantly depending on different features. Features that define the structure of a fixed income security include its type of interest payment (floating, fixed, inflation-linked), the interest payment amount (which is linked to the credit quality of the issuer), its term (perpetual, callable or fixed term) or its position on the capital structure (secured, unsecured or subordinated). Additionally, fixed income is generally defined by the underlying issuer – Government, State Government or Corporations.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Nov 7, 2025Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Nov 7, 2025Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.