The Australian fixed income market is a significant source of funds for Australian and international corporations. Senior debt is issued by corporations to finance projects and other day-to-day business activities. These types of securities can generally take four forms: In terms of the capital structure, Senior Secured

- Covered Bonds – The obligations of a covered bond are secured against a pool of assets. This means in the event of default investors have first claim to repayment from the underlying assets. In Australia these bonds are commonly issued by airports and in 2011 the Commonwealth Government gave domestic banks the right to issue these securities also. However, this has been capped by the Australian Prudential Regulation Authority (APRA) at 8% of total assets to protect depositors.

Senior Unsecured

- Fixed Rate Bonds – similar to Commonwealth Government Securities, corporate fixed rate bonds pay a constant semi-annual interest payment until maturity. However, this coupon can be subject to step-up or step-down conditions dependent on certain security-specific clauses.

- Floating Rate Notes – These securities generally pay interest on quarterly basis equal to an appropriate floating benchmark rate with a fixed margin. The benchmark rate is usually the 90-Day Bank Bill Swap Rate which resets every quarter. As a result, distribution income will fluctuate with movements in interest rates. This effectively mitigates the interest rate risk inherent in fixed coupon bonds. Floating rate notes can also be subject to changes in fixed margin depending on certain conditions.

- Indexed-Linked Bonds – As previously mentioned, corporations can issue inflation-linked bonds. These bonds are generally structured in the same manner described in the preceding section

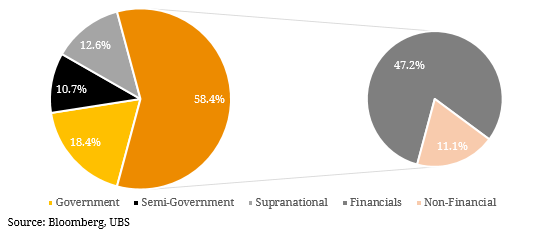

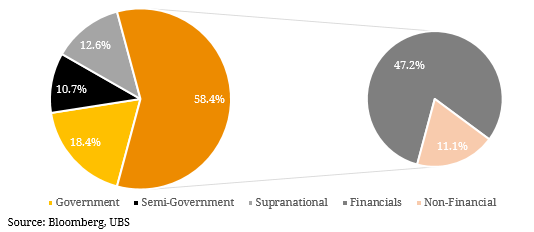

Figure 1. Corporate Australian Dollar Denominated Bond Issuance 2015  As illustrated above, the Australian corporate fixed income market is dominated by financial institutions, primarily banks.

As illustrated above, the Australian corporate fixed income market is dominated by financial institutions, primarily banks.