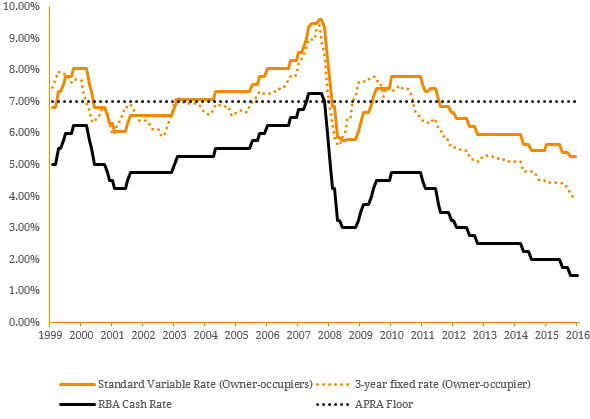

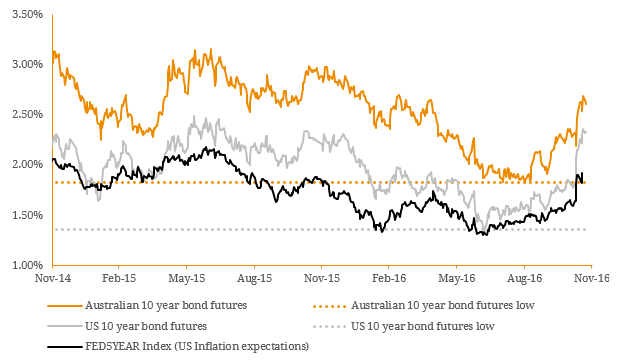

In December 2014, the Australian Prudential Regulation Authority (APRA) wrote to all Australian Deposit-Taking Institutions (ADIs) stating that mortgages should be stress tested under the scenario that interest rates rise at least 2% above current loan rates, setting the minimum rate (floor) at 7%. This suggestion highlighted that serviceability tests should be calibrated at an interest-rate set at a level considered ‘through the cycle’. In other words, interest-rates could at some point in the life of a 30-year loan normalise to more historical average levels (~6.00 – 7.00% p.a.). For the purposes of this article we examine the relationship between the Standard Variable Mortgage Rate (SVR), the Reserve Bank of Australia (RBA) cash rate and global bond yields and how they impact the four major banks as they represent ~83% of total residential mortgage lending. Australians have benefited from a low interest rate environment for the majority of the past decade but it is easy to forget that there have been periods over the past sixteen years that mortgage interest-rates have in fact been above the 7% floor set by APRA (Figure 1). Figure 1. Average Australian mortgage SVR (pre-discounts)  Source: RBA, APRA Whilst we are not suggesting that the SVR will reach 7% in the near term, it is important for borrowers and investors alike to understand the drivers of interest rate movements and how this in turn influences movements in mortgage rates. As Figure 1 clearly shows, there is a strong correlation between the RBA cash rate and the SVR mortgage rate. One of the primary objectives of the RBA is to maintain price stability. Therefore, as Australian inflation expectations remain within the RBA’s target band of 2-3% (on average over the cycle) there is no real pressure on the RBA at the moment to increase the cash rate. However, Australia’s longer term interest rates have moved higher in recent months. This has been largely driven by the US Treasury 10-year bond yield which started to rise long before November’s US Presidential election (Figure 2). Figure 2. Australian & US 10-year bond futures yield during 2016

Source: RBA, APRA Whilst we are not suggesting that the SVR will reach 7% in the near term, it is important for borrowers and investors alike to understand the drivers of interest rate movements and how this in turn influences movements in mortgage rates. As Figure 1 clearly shows, there is a strong correlation between the RBA cash rate and the SVR mortgage rate. One of the primary objectives of the RBA is to maintain price stability. Therefore, as Australian inflation expectations remain within the RBA’s target band of 2-3% (on average over the cycle) there is no real pressure on the RBA at the moment to increase the cash rate. However, Australia’s longer term interest rates have moved higher in recent months. This has been largely driven by the US Treasury 10-year bond yield which started to rise long before November’s US Presidential election (Figure 2). Figure 2. Australian & US 10-year bond futures yield during 2016  Source: Bloomberg One of the reasons for US (and therefore global) bond yields rising since mid-2016 has been the rise in the US Federal Reserve’s (Fed) 5–year, 5-year forward inflation break-even rate index. This index is a widely-watched market indicator of US inflation expectations, and although it is an imperfect gauge of real world activity it is nonetheless a sign of a growth optimism in the US economy. The 5-year, 5-year inflation breakeven rate is calculated from the difference between prices for normal government debt and bonds where the coupon is linked to the rate of consumer price inflation. As a result, global bond markets have priced in a higher probability that the Fed will hike interest rates in their December meeting (as the US incoming administration are expected to favour pro-growth economic policies which are naturally inflationary in nature). In Australia, this has meant a steepening (Figure 3) of the Australian government yield curve as the RBA are now expected to remain on hold for much of 2017 (therefore limiting the increase in yield of shorter dated bonds). On the other hand, longer term bonds have moved higher in yield, influenced by the move in longer term US bond yields and inflation expectation. Figure 3. Australian government yield curve before and after the presidential election

Source: Bloomberg One of the reasons for US (and therefore global) bond yields rising since mid-2016 has been the rise in the US Federal Reserve’s (Fed) 5–year, 5-year forward inflation break-even rate index. This index is a widely-watched market indicator of US inflation expectations, and although it is an imperfect gauge of real world activity it is nonetheless a sign of a growth optimism in the US economy. The 5-year, 5-year inflation breakeven rate is calculated from the difference between prices for normal government debt and bonds where the coupon is linked to the rate of consumer price inflation. As a result, global bond markets have priced in a higher probability that the Fed will hike interest rates in their December meeting (as the US incoming administration are expected to favour pro-growth economic policies which are naturally inflationary in nature). In Australia, this has meant a steepening (Figure 3) of the Australian government yield curve as the RBA are now expected to remain on hold for much of 2017 (therefore limiting the increase in yield of shorter dated bonds). On the other hand, longer term bonds have moved higher in yield, influenced by the move in longer term US bond yields and inflation expectation. Figure 3. Australian government yield curve before and after the presidential election  Source: Bloomberg Given the regulatory requirements given to Australian banks over the past few years and the subsequent drag on profitability, there now may be an incentive for the major banks to reprice Australian mortgage products upwards to protect margins. The major banks may choose to do this by either restricting credit further via further tightening of credit standards and therefore engaging in a form of credit rationing, or perhaps by repricing lower quality (or underperforming loans) in the hope that borrowers will seek an alternative and cheaper mortgage provider (as a way of protecting the bank balance sheet against a future rise in impairments as interest rates start rise and overcommitted borrowers struggle with repayments). Overall, the possibility of higher mortgage rates is now much more realistic than before.

Source: Bloomberg Given the regulatory requirements given to Australian banks over the past few years and the subsequent drag on profitability, there now may be an incentive for the major banks to reprice Australian mortgage products upwards to protect margins. The major banks may choose to do this by either restricting credit further via further tightening of credit standards and therefore engaging in a form of credit rationing, or perhaps by repricing lower quality (or underperforming loans) in the hope that borrowers will seek an alternative and cheaper mortgage provider (as a way of protecting the bank balance sheet against a future rise in impairments as interest rates start rise and overcommitted borrowers struggle with repayments). Overall, the possibility of higher mortgage rates is now much more realistic than before.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Jun 26, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Jun 26, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.