In context of bond valuations, accrued interest is defined as the difference between the dirty and clean price. It is the interest that has accrued but not been paid since the last payment date. In most cases securities are not traded on payment dates and therefore investors are entitled to the interest earned but have not received for the period between last payment date and settlement date. This is why the purchaser pays accrued interest plus clean . According to the Australian Financial Market Association (AFMA), accrued interest is the proportional amount based on how long investors have held the bond. This is mathematically described below:

AI=ch/d

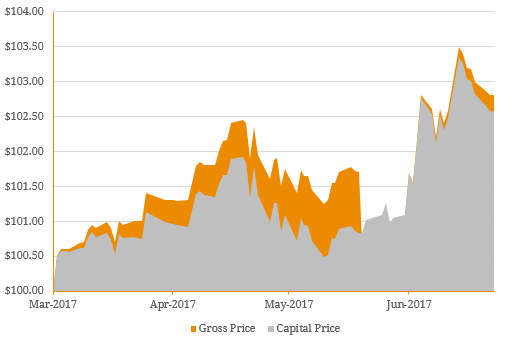

C= the periodic yield h= number of days between settlement and last payment d= number of days of the current payment period ending on the next interest payment Globally, there are a number methods to calculate accrued interest depending on pricing standards, conventions and specific to Australia how investors account for franking credits. As a rule, we follow the AFMA convention for all debt and hybrid securities. To confuse people further there are circumstances where the accrued interest amount can actually be negative. The ASX market conventions dictate an ‘ex-date’ for interest payments in the same way they dictate an ‘ex-date’ for dividends on equities. If a bond or hybrid goes ex-interest the accrued amount will drop to a negative amount until the physical cash amount is paid. From the payment date, the accrued amount increases accordingly. For example, Figure 1 shows the price history since inception of NAB Subordinated Notes 2. Its shows the accrued interest (orange) building up until the Ex-Date (8 June 2017) when its drops into negative. It then progressively builds up again, going positive on the payment Date (20 June 2017), until the next ex-date. All of the price and date information can be found in the ASX announcement seen here. Figure 1. NAB Subordinated Notes 2 (ASX Code: NABPE) Capital Price and Accrued Interest  Source: BondAdviser

Source: BondAdviser