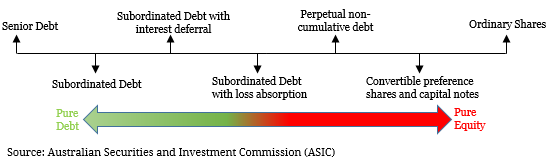

Hybrids refer to a broad classification of securities issued by corporations that structurally contain both debt and equity characteristics. In terms of the capital structure, hybrids sit subordinated debt and above equity in the capital structure and tend to offer higher yields than senior bonds. These securities rank behind subordinated debt in the priority of payment while still enjoying the equity buffer. Hybrids are structured in a more complex manner than most other fixed income instruments and generally contain embedded options. These options typically allow the issuer to either redeem the security before its specified maturity or convert the security into ordinary shares. Figure 1. Hybrid Security Spectrum  Although it is necessary to assess each hybrid on a case-by-case basis, for the purpose of this section we will describe the most common Bank and Non-Bank security structures: Bank & Insurance Hybrids Due to Australian regulation enforced by the Australian Prudential Regulation Authority (APRA), the hybrid market is predominantly utilised by banks. Under APRA, Australian banks must adhere to strict capital requirements to ensure future economic stability. As a result, these bank hybrids can either classify as Tier 1 and Tier 2 regulatory capital. These essentially act as two layers of junior debt (with Tier 2 capital ranking above Tier 1 capital and below subordinated debt and Tier 1 capital ranking below Tier 2 capital and above common equity) – refer to page 9 ‘Capital Structure’. The insurance industry also follows the principals of this regulation. Tier 2 Instruments

Although it is necessary to assess each hybrid on a case-by-case basis, for the purpose of this section we will describe the most common Bank and Non-Bank security structures: Bank & Insurance Hybrids Due to Australian regulation enforced by the Australian Prudential Regulation Authority (APRA), the hybrid market is predominantly utilised by banks. Under APRA, Australian banks must adhere to strict capital requirements to ensure future economic stability. As a result, these bank hybrids can either classify as Tier 1 and Tier 2 regulatory capital. These essentially act as two layers of junior debt (with Tier 2 capital ranking above Tier 1 capital and below subordinated debt and Tier 1 capital ranking below Tier 2 capital and above common equity) – refer to page 9 ‘Capital Structure’. The insurance industry also follows the principals of this regulation. Tier 2 Instruments

- The most common bank Tier 2 security structure is commonly referred to as ‘Subordinated Notes’. This hybrid generally pays a mandatory quarterly floating rate interest payment and typically has an optional call date whereby the issuer can redeem the notes early on that date or any interest payment date thereafter up to the final maturity date.

Tier 1 Instruments

- The popularity of ‘Capital Notes’ has increased over recent years. These securities primarily distribute a quarterly floating rate interest payment but some pay on a semi-annual basis. However, distributions on these hybrids are discretionary and therefore at the option of the issuer. Additionally, these payments are non-cumulative meaning any missed payments are not owed by the issuer. Capital Notes are classified as a perpetual investment as they have no set maturity date. Instead they are scheduled for mandatory conversion into ordinary shares and subject to optional call date(s) prior to the mandatory conversion date. These securities are primarily issued by the major banks (Westpac, NAB, Commonwealth Bank and ANZ) and Macquarie Group.

- The less commonly used bank Tier 1 security are ‘Preference Shares’. Like capital notes, preference shares are perpetual and have discretionary, non-cumulative interest payments. Preference shares are subject to optional call dates prior to the mandatory conversion date as well. Generally, the major difference between the two main Tier 1 securities is the timing of distributions. Preference Shares tend to pay interest of a semi-annual floating rate basis.

Regulatory Considerations A major reason for the push for the Capital Note hybrid has been regulation. Post 2012, new capital instrument eligibility criteria under Basel III was introduced to the Australia Banking System. This included the implementation of loss absorbing terms and conditions known as Capital and Non-Viability Trigger Events. These are common in all new style (after 2012) Tier 1 and Tier 2 hybrids. Upon the occurrence of these events this security will be converted into ordinary shares without the protection of conversion conditions. However, if conversion cannot occur for any reason the notes will be written off and all holders rights terminated. The Non-Viability Trigger is at the discretion of the regulator, APRA, while the Capital Trigger will occur if the underlying issuer is unable to maintain a Common Equity Tier 1 ratio of 5.125%. In terms of size, the Tier 1 market is substantially larger than the Tier 2 market. Figure 2. Major Bank Tier 1 Regulatory Capital  Non-Bank Hybrids Non-Bank corporations are not subject to same regulatory scrutiny as traditional Australian banks. As a result, hybrid variation is much broader in this market and almost every security is unique in its own right. However, we will outline two general security structures:

Non-Bank Hybrids Non-Bank corporations are not subject to same regulatory scrutiny as traditional Australian banks. As a result, hybrid variation is much broader in this market and almost every security is unique in its own right. However, we will outline two general security structures:

- Subordinated Notes are the most common hybrid security issued by Non-Bank corporations. These securities differ between issuers but generally have a fixed maturity date with prior optional call or conversion dates. One of the major differences between these notes and their bank counterparts are that interest payments are discretionary. However, they are cumulative meaning missed interest payments will be made once the issuer is in a position to do so. Some of this types of securities have step-up conditions whereby the coupon will receive a specified increase dependent a particular event. This step-up is typically reversed when the event ends.

- Step-Up Securities are perpetual and interest payments are discretionary but non-cumulative. These securities tend to have an optional redemption date known as the ‘Step-Up Date’. If on the step-up date the issuer chooses not to redeem the securities, the coupon will receive a specified increase until redemption. The issuer is typically able to redeem the securities at any point from the step-up date. It is possible for these securities to have multiple step-up dates. Issuer redemption will be based on the overall cost of funding. If the cost of funding is less than the coupon being paid, the underlying securities will most likely be redeemed.