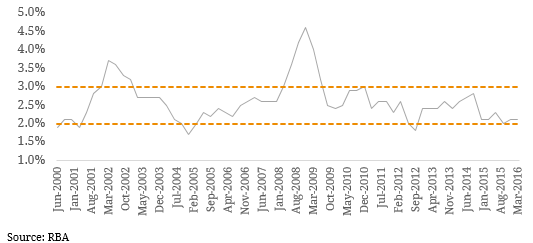

Inflation-Linked Bonds (also known as ‘linkers’) can either by issued by Commonwealth of Australia, State Governments or corporations. These securities are structured so their coupon payments are linked to the current inflation rate. When coupons are set at a fixed rate, inflation erodes the purchasing power of interest payments over time. Inflation-Linked Bonds mitigate this risk and can be particularly useful for those invests at or near retirement. The value of these instruments are linked to inflation expectations. The face value of a Linker is typically adjusted each quarter for movements in the Consumer Price Index (CPI). This equates to the Nominal Value (NV). Fixed rate interest payments are usually paid quarterly in arrears on the nominal value. If deflation occurs and the nominal value falls below the face value of bond the interest payments will be based on face value. At maturity the holder receives the nominal value or the initial face value (whichever is greater). The CPI measures the price changes of a ‘basket’ of goods that cover a large proportion of expenditure for the average Australian household. Since the adoption of a 2-3% inflation by the Reserve Bank of Australia (RBA) in 1996, the CPI has broadly tracked an annual increase broadly within this range. Figure 1. CPI (excluding volatile items) against the RBA Target Inflation Range  Although corporations can issue linkers, these securities are primarily dealt with by the Federal and State governments. In 2009, the AOFM made a commitment to increase inflation-linked bond issuance. This is shown in Figure 2. Figure 2. Treasury Inflation Linked Bonds Outstanding

Although corporations can issue linkers, these securities are primarily dealt with by the Federal and State governments. In 2009, the AOFM made a commitment to increase inflation-linked bond issuance. This is shown in Figure 2. Figure 2. Treasury Inflation Linked Bonds Outstanding

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Oct 28, 2025Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Oct 28, 2025Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.