Security covenants play a crucial role in investor protection and serve as a major contributor to credit analysis. While financial institutions such as banks and insurance companies are subject to regulatory requirements, a security’s covenant package is instrumental to downside protection when investing in non-financial corporate debt issuers. Covenants are legally enforceable conditions that borrowers (the issuer) and lenders (the investors) agree upon at time of issuance. The agreement typically outlines an issuer’s pledge to operate within certain limits and is defined in the security’s legal documentation such as an information memorandum or prospectus. If a specified limit or condition is breached by the issuer, the legal documentation also specifies cure periods and remedies available to security holders. The security trustee is responsible for monitoring these covenants and may take action against the issuer on behalf of the investors if violation has occurred. Covenants can be either affirmative or negative. Affirmative (or positive) covenants are clauses that require a borrower to perform specific actions. Examples complying with certain laws, maintaining assets and/or submitting certain reports beyond typical disclosure requirements. On the other hand, negative covenants are established to restrict the issuer from certain actions that would reduce their ability to service the obligations of the security. These limits can be specified in the form of a financial ratio which are tested on a periodic basis. The objective of these ratios generally involve capping leverage while creating floors for earnings, cash flow and overall liquidity. These are known as financial covenants. However, all covenants can be subject to various exceptions and further conditions which highlights the importance of reading the fine print. While breach of a covenant can result in outright default, it can also trigger other conditions such as a credit rating downgrade or a step-up in the coupon rate/interest margin. For securities with discretionary distributions (such as hybrids), there are negative covenants which dictate whether the issuer must defer distributions to security holders until a breach is reversed. On the other hand, if a certain financial metric reaches a specified threshold, it may allow the issuer to pay dividends, commence a share-buyback or engage in asset sales or divestments. Ultimately covenants can take many different forms and a highly specific to the security and underlying issuer. Negative covenants which require issuers to adhere to financial metric limits (such as below) can be subject to maintenance or incurrence tests. Maintenance tests requires the issuer maintains compliance with a metric to avoid default. For example, a maintenance test could be a maximum gearing ratio of 50%, which if the company exceeded, would result in default. However, using the same example, an incurrence test would only be violated if the company actively incurred additional debt to the point where gearing exceeded 50% but not if total capital declined and caused gearing to increase. Common types of negative covenants and associated financial covenants:

| Limitation | Examples Financial Covenant /Clause |

| Indebtedness | Gearing Ratio, Leverage Ratio |

| Liquidity | Interest Coverage Ratio |

| Secured Indebtedness | Secured Gearing Ratio, Negative Pledge |

| Asset Sales | Tangible Net Worth |

| Shareholder Distributions | Maximum of NPAT, other conditions |

| Transactions with Affiliates | Minimum Cash Balance of Issuer |

| On being Acquired | Change of Control Event |

- Gearing Ratio (Debt to Total Capital): This ratio illustrates the amount of debt proportionate the group’s total capital (total debt + equity) and can be used to limit total company indebtedness.

- Leverage Ratio (Debt to EBITDA): Reflects how many times greater a company’s debt pile is greater than its annual EBITDA. This metric can be used as a limitation of indebtedness.

- Interest Coverage (EBIT or EBITDA to Interest Expense): This metric calculates the how many times a company’s EBIT or EBITDA can cover its interest expense. Interest coverage is sometimes calculated on a semi-annual basis but generally is an annualised figure.

- Secured Gearing Ratio (Secured Debt to Total Capital): Typically used for unsecured or subordinated debt which is not secured by the company’s assets. On the other hand, secured debt has first right over the company’s assets if it is in default. The ratio calculates the amount of secured debt as a proportion to the company’s total capital (total debt + equity) and be used to restrict secured debt incurrence.

- Negative Pledge: A covenant that prevents the issuer from raising additional secured debt. As a result, the issuer will not ‘pledge’ any of its assets as security giving investors of unsecured or subordinated debt less security.

- Restricted Payments to Shareholders: This covenant limits the power of equity holders and generally limits dividend distributions to a maximum percentage of Net Profit After Tax (NPAT). As mentioned, these restrictions pay be lifted if a certain threshold or target is reached.

- A Change of Control Clause: This clause is designed to protect investors where a change in ownership could damage credit quality. The covenant generally gives security holders the opportunity to choose to redeem their holdings upon a change of control at par value or a premium to par value.

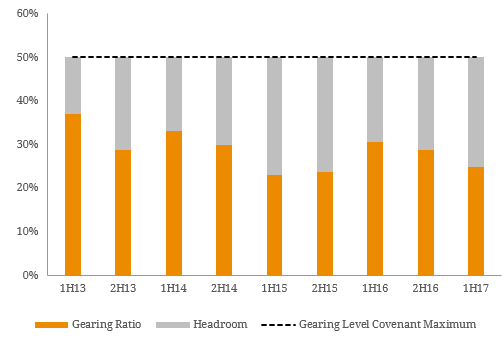

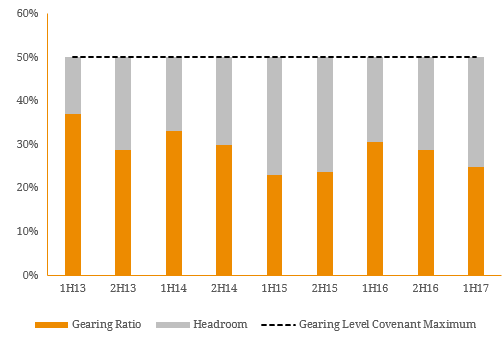

Covenants are only one piece of the credit analysis puzzle but nonetheless, are a key component of a security’s risk profile. While an issuer’s fundamentals, underlying industry and valuation can make a potential debt investment attractive, the covenant package can alter this the significantly to point where the security becomes uninvestable. As a result, covenants are a balancing act between operational flexibility for the company and mitigation of downside risk for the investor. They are crucial to the investment process and allow investors to benchmark the credit quality of the security against the covenant requirement to assess if credit is improving or deteriorating. For this reason, it is imperative that investors can competently dissect and analyse security covenants. Figure 1. Example of a Corporate Financial Covenant and Credit Quality over time.  Source: BondAdviser, Company Reports.

Source: BondAdviser, Company Reports.