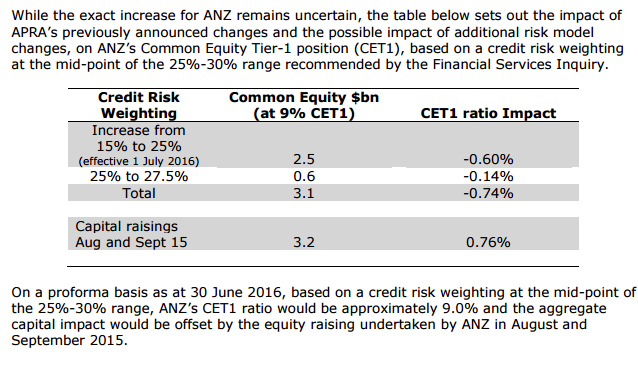

ANZ Banking Group’s Chief Executive Officer, Shayne Elliot, provided markets with an unaudited third quarter 2016 financial year (3Q16) update. The key take-outs were: Group – Statutory net profit after tax was $4.3 billion with the cash profit down 3% to $5.2 billion. Group Net Interest Margin (NIM) was described as being stable. Institutional – The continued rebalancing and restructuring of this business has resulted in a $15 billion decrease in the Credit Risk Weighted Assets (CRWA) occurring in 3Q16. Although divisional revenue decreased less than the reduction in the CRWA. It resulted in a positive impact on NIM by ~5 basis points. Provisions – The 3Q16 total provision charge was $1.4 billion comprising of individual provisions of $1.34 billion and collective provisions of $60 million (up on 1H16 by 52.5%, 50.2% and 7.1% respectively). The bottom of the credit cycle has clearly passed with ANZ’s total provision charge, gross impaired assets and 90+ day home loan delinquencies (inclusive of hardship change) all trending up over FY16. Capital – As at 30 June 2016 ANZ’s Core Tier 1 (CET1) ratio was 9.7%, Tier 1 ratio 11.8% and the Total Capital Ratio 14.4%. This was well above APRA’s regulatory minimum requirement of 8%. ANZ also commented on APRA’s revised mortgage RWA target on 8 August, providing additional insights as to how the CET1 capital ratio could be impacted:  Source: ANZ ASX company announcement 8 August 2016. ANZ said that a 1% increase (or decrease) from the mid-point (27.5%) would have an impact on the pro forma CET1 ratio of approximately 6 basis points due to he capital raised in August/September 2015. The Leverage Ratio remained flat over the quarter at 5.1%; Continue to expect the FY16 result for the group to be broadly in line with expectations as 4th quarter seasonal factors have benefited ANZ historically. This update is neutral from a credit point of view.

Source: ANZ ASX company announcement 8 August 2016. ANZ said that a 1% increase (or decrease) from the mid-point (27.5%) would have an impact on the pro forma CET1 ratio of approximately 6 basis points due to he capital raised in August/September 2015. The Leverage Ratio remained flat over the quarter at 5.1%; Continue to expect the FY16 result for the group to be broadly in line with expectations as 4th quarter seasonal factors have benefited ANZ historically. This update is neutral from a credit point of view.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Apr 14, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Apr 14, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.