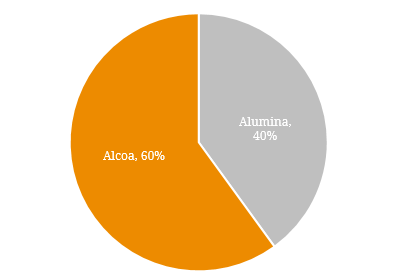

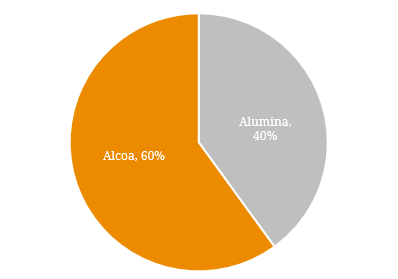

In recent months, Alumina Limited (ASX: AWC) has been media spotlight regarding an ongoing legal dispute with its major business partner Alcoa. Both companies form part of the world’s largest Alumina business, Alcoa World Alumina and Chemicals (AWAC), which is involved in bauxite mining as well as alumina refining and smelting. Figure 1. AWAC Ownership  Source: Company Reports In early 2016, Alcoa proposed a corporate separation in which Alcoa would cease to partner with Alumina in AWAC and instead create a new legal entity to hold this interest. This was vigorously defended by Alumina and in September both parties agreed to terminate litigation and instead amend the AWAC joint venture agreement. However, the demerger is still scheduled to go ahead and will split Alcoa into Arconic (new name for Alcoa Inc.) and Alcoa Upstream Corp (which will hold the 60% AWAC ownership) which is materially weaker from a financial perspective. As a direct consequence of its new partner, Alumina was given a double notch credit rating downgrade from Standard & Poor’s. With less cyclical ‘downstream’ assets now removed from the partnership, Alcoa Corp has a greater exposure to the underlying Alumina market price and as the weaker Alcoa Corp will now be the operator and majority owner of AWAC assets and this in turn significantly increases counterparty risk for Alumina. As a result, we can expect the credit profile of Alumina to be closely tied to the actions and operating performance of the newly formed entity. Alumina currently has single bond outstanding that matures in 2019 which is available to wholesale investors only (no prospectus being issued) and is not listed on the Australian Securities Exchange. While off limits to retail investors, this security highlights the importance of understanding relevant clauses and provisions. Under the documentation, the bond is subject to coupon step-up provisions and following the credit rating announcement the coupon rate stepped up from 5.50% p.a. to 7.25% p.a. to reflect the higher level of risk. Any subsequent credit rating upgrade will reverse the coupon rate step-up. While this has increased the bond’s expected return (yield), this is not without increased risk as the probability of default has risen. Under our credit risk classification, Alumina as a standalone entity has moved from 9 (Upper-Medium) to 12 (High) on our credit risk spectrum shown in the diagram below. Figure 2. Exponential Relationship between Credit Quality and Probability of Default

Source: Company Reports In early 2016, Alcoa proposed a corporate separation in which Alcoa would cease to partner with Alumina in AWAC and instead create a new legal entity to hold this interest. This was vigorously defended by Alumina and in September both parties agreed to terminate litigation and instead amend the AWAC joint venture agreement. However, the demerger is still scheduled to go ahead and will split Alcoa into Arconic (new name for Alcoa Inc.) and Alcoa Upstream Corp (which will hold the 60% AWAC ownership) which is materially weaker from a financial perspective. As a direct consequence of its new partner, Alumina was given a double notch credit rating downgrade from Standard & Poor’s. With less cyclical ‘downstream’ assets now removed from the partnership, Alcoa Corp has a greater exposure to the underlying Alumina market price and as the weaker Alcoa Corp will now be the operator and majority owner of AWAC assets and this in turn significantly increases counterparty risk for Alumina. As a result, we can expect the credit profile of Alumina to be closely tied to the actions and operating performance of the newly formed entity. Alumina currently has single bond outstanding that matures in 2019 which is available to wholesale investors only (no prospectus being issued) and is not listed on the Australian Securities Exchange. While off limits to retail investors, this security highlights the importance of understanding relevant clauses and provisions. Under the documentation, the bond is subject to coupon step-up provisions and following the credit rating announcement the coupon rate stepped up from 5.50% p.a. to 7.25% p.a. to reflect the higher level of risk. Any subsequent credit rating upgrade will reverse the coupon rate step-up. While this has increased the bond’s expected return (yield), this is not without increased risk as the probability of default has risen. Under our credit risk classification, Alumina as a standalone entity has moved from 9 (Upper-Medium) to 12 (High) on our credit risk spectrum shown in the diagram below. Figure 2. Exponential Relationship between Credit Quality and Probability of Default  Source: BondAdviser Although this step-up will not apply until next interest period (starting November 2016), markets have priced in the credit rating downgrade throughout most of 2016 and the trading margin of the bond has widened considerably by almost 3.00%. This demonstrates the importance of investor awareness and being proactive rather than reactive (i.e. acting before the credit rating agencies) when managing fixed income investments. Note the sharp increase in September reflects when coupon step-up was triggered. Figure 3. Trading Margin History 2016

Source: BondAdviser Although this step-up will not apply until next interest period (starting November 2016), markets have priced in the credit rating downgrade throughout most of 2016 and the trading margin of the bond has widened considerably by almost 3.00%. This demonstrates the importance of investor awareness and being proactive rather than reactive (i.e. acting before the credit rating agencies) when managing fixed income investments. Note the sharp increase in September reflects when coupon step-up was triggered. Figure 3. Trading Margin History 2016  Source: BondAdviser as at 27 of September 2016 As investors, it is natural to be content with higher interest payments but we must remember the key objective to fixed income investing is capital preservation. Coupon step-up clauses are generally anticipated as shown by the Alumina’s trading margin history and triggered due to increased risk. This highlights the importance of credit research and proper due diligence to give investors investment flexibility and assess all options before it is too late and the market has swung to reflect a change in risk. Overall, coupon-step up provisions cannot be taken lightly.

Source: BondAdviser as at 27 of September 2016 As investors, it is natural to be content with higher interest payments but we must remember the key objective to fixed income investing is capital preservation. Coupon step-up clauses are generally anticipated as shown by the Alumina’s trading margin history and triggered due to increased risk. This highlights the importance of credit research and proper due diligence to give investors investment flexibility and assess all options before it is too late and the market has swung to reflect a change in risk. Overall, coupon-step up provisions cannot be taken lightly.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Jul 17, 2026 Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Jul 17, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.