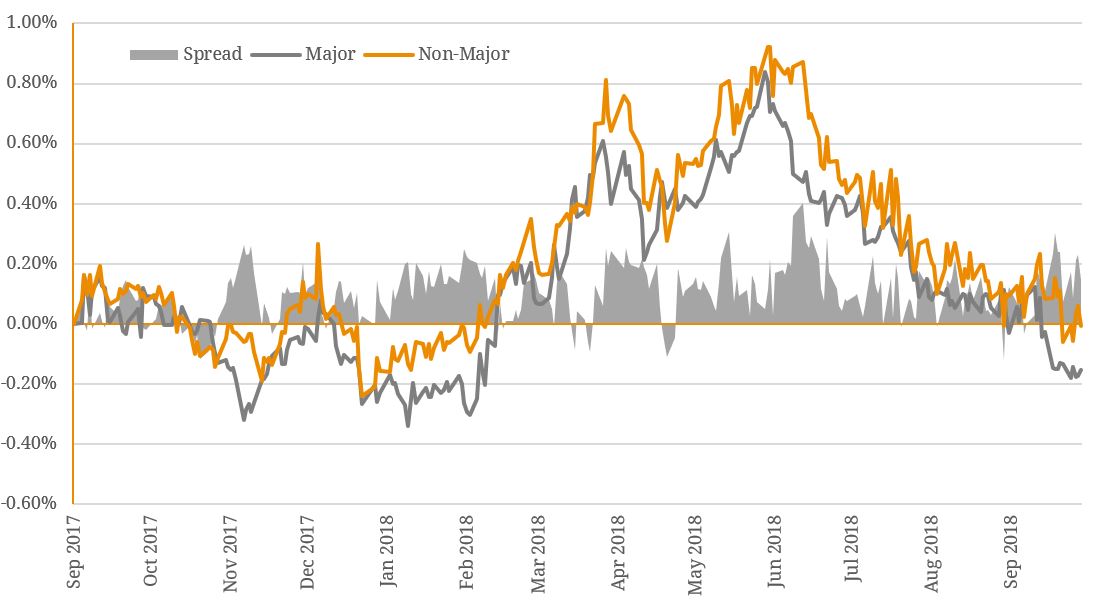

Ever since the Global Financial Crisis (GFC), funding costs in capital markets for both major and regional Australian banks have been steadily declining. This was first sparked by the Australian Government Guarantee Scheme which reduced the underlying risk in Australian authorised deposit-taking institutions (ADIs). In this post-GFC era, funding costs have broadly moved in line with changes in the RBA cash rate, which reached a record-low of 1.50% in August 2016 and has since remained at its trough for 26 consecutive RBA meetings. Whilst the yields on new debt instruments continue to tighten in a period of ‘easy credit’, it is the major banks (ANZ, CBA, NAB, WBC and MQG) that continue to enjoy the competitive advantage when raising funds. This has seen the regional banks (AMP, BOQ, BEN, ME and SUN) unite on multiple occasions in recent years through their submissions to the Australian Productivity Commission, citing a ‘distorted playing field’ in favour of the majors. Key areas of concern include the increasing compliance cost burden imposed on regionals with smaller customer bases, material differences in risk-weighted mortgage assets and APRA’s macroprudential restrictions that have the effect of ‘locking in market share’. However, perhaps the factor of most significance to the spread differential between the two groups, is the ‘too big to fail’ implicit subsidy which gives the majors a distinct credit rating advantage on wholesale debt, with the ‘Big 4’ (ANZ, CBA, NAB, WBC) enjoying a AA-/Aa3 rating, whilst BEN and BOQ sit several notches below at BBB+/A3. However, despite the concerns expressed by the leaders of the regionals and the comparative disadvantage they face, trading margins in the Additional Tier 1 (AT1) market have compressed in recent times, particularly for the major bank instruments (figure 1). Figure 1. Average Trading Margins of Additional Tier 1 Capital Securities  Source: BondAdviser, Bloomberg Furthermore, in the Tier 2 senior unsecured market, recent issuances in 2018 have seen initial pricings set at a relatively tight 25 bps spread, which infers a disappearing of the risk premia traditionally seen in credit markets based on divergent issuer profiles and credit ratings (figure 2). Figure 2. Tier 1 Financial Securities – Current Trading Margins

Source: BondAdviser, Bloomberg Furthermore, in the Tier 2 senior unsecured market, recent issuances in 2018 have seen initial pricings set at a relatively tight 25 bps spread, which infers a disappearing of the risk premia traditionally seen in credit markets based on divergent issuer profiles and credit ratings (figure 2). Figure 2. Tier 1 Financial Securities – Current Trading Margins  Source: BondAdviser, Bloomberg This raises the question of whether we could potentially see the regional bank primary issuance price below the majors in the near future, defying the ‘too big to fail’ designation the majors currently possess. With significant headwinds facing the major banks, most notably the unknown fallout from the Royal Commission (noting that the regionals themselves did emerge unscathed), dwindling credit supply due to increased regulatory oversight and tighter lending conditions, it is perhaps not so far-fetched to foresee a regional bank pricing convergence. Furthermore, as APRA continues to raise the requirements for average risk weightings on Australian residential mortgage exposures for ADIs using the internal ratings-based (IRB) approach (i.e. the approach adopted the Big 4) towards that of the standard ratings approach (i.e. regional banks), the material difference between the two is now approaching 15 bps. Whilst the regionals continue to make strides towards advanced accreditation (and therefore approval to use the IRB approach), it is hard to envision a future where the regional banks are the beneficiary of favourable borrowing terms. Given the firmly entrenched banking hierarchy in Australia, where the major banks hold ~80% of all residential mortgage exposure on their balance sheets, it appears it would take something extraordinary to uproot the status-quo. Lastly, the current 15 bps differential between the IRB and standardised approaches will allow the majors to leverage their scale and liquidity depth to generate higher profit margins from the same asset class. This, coupled with the diversification benefits enjoyed due to the sheer size of the major banks, should allow them to maintain their competitive advantage in the issuance space.

Source: BondAdviser, Bloomberg This raises the question of whether we could potentially see the regional bank primary issuance price below the majors in the near future, defying the ‘too big to fail’ designation the majors currently possess. With significant headwinds facing the major banks, most notably the unknown fallout from the Royal Commission (noting that the regionals themselves did emerge unscathed), dwindling credit supply due to increased regulatory oversight and tighter lending conditions, it is perhaps not so far-fetched to foresee a regional bank pricing convergence. Furthermore, as APRA continues to raise the requirements for average risk weightings on Australian residential mortgage exposures for ADIs using the internal ratings-based (IRB) approach (i.e. the approach adopted the Big 4) towards that of the standard ratings approach (i.e. regional banks), the material difference between the two is now approaching 15 bps. Whilst the regionals continue to make strides towards advanced accreditation (and therefore approval to use the IRB approach), it is hard to envision a future where the regional banks are the beneficiary of favourable borrowing terms. Given the firmly entrenched banking hierarchy in Australia, where the major banks hold ~80% of all residential mortgage exposure on their balance sheets, it appears it would take something extraordinary to uproot the status-quo. Lastly, the current 15 bps differential between the IRB and standardised approaches will allow the majors to leverage their scale and liquidity depth to generate higher profit margins from the same asset class. This, coupled with the diversification benefits enjoyed due to the sheer size of the major banks, should allow them to maintain their competitive advantage in the issuance space.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© May 24, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© May 24, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.