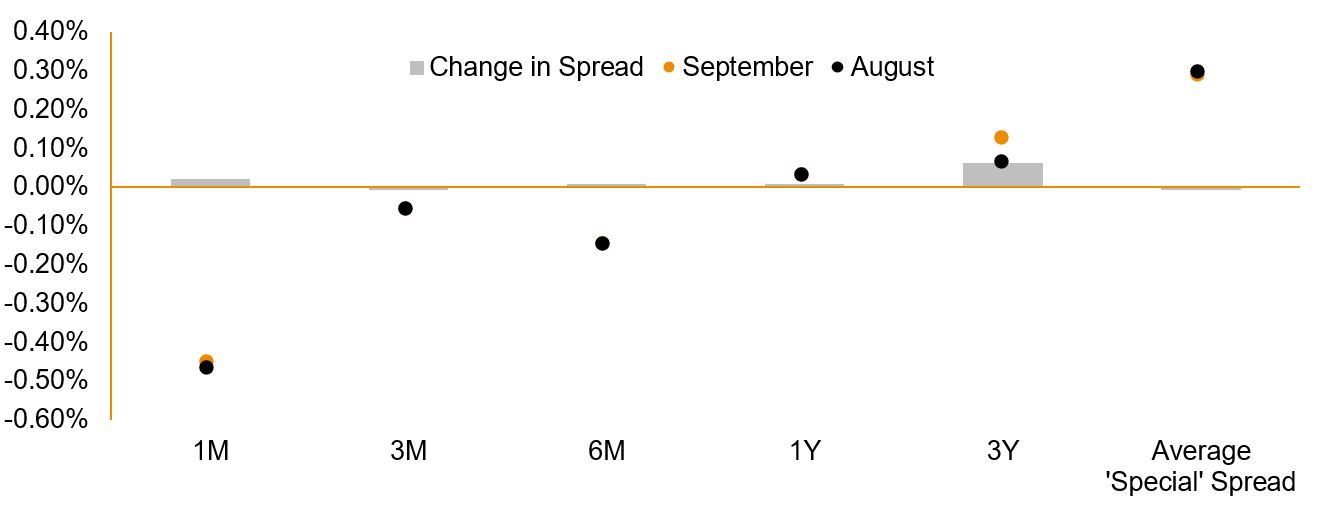

The month of September presented us with many of the same recurring themes, namely the ongoing US-China trade war rhetoric, whilst the RBA continue to hold the overnight cash rate at 1.50%. Commissioner Kenneth Hayne also released his scathing interim report from the Royal Commission, making recommendations including better enforcement of the law by regulators and a simplification of those laws to assist them in doing so. Meanwhile, the US Federal Reserve (“the Fed”) raised the Federal Funds Target Rate by 25 bps to lie within the 2.00-2.25% range. Whilst this move was widely anticipated, the FOMC omitted “accommodative” when describing its monetary policy stance, implying that the Fed Funds rate may be moving towards more “neutral” territory and normalising rates. Furthermore, US Federal Reserve Chairman Jerome Powell stated in his minutes that the inflationary impact of a tight labour market was “greatly reduced, not eliminated”. This is significant, as it indicates the Fed’s belief that inflation is largely contained, and it sees no need to aggressively raise rates. This may provide some relief domestically as it eases the rising funding pressure costs on authorised deposit-taking institutions (ADIs) who have announced out-of-cycle rate hikes over the past few months. Figure 1. Term Deposit Spread Over Relevant BBSW: September 2018 v August 2018  Source: RBA, BondAdviser For full details, charts and commentary, please click here for the full pdf version.

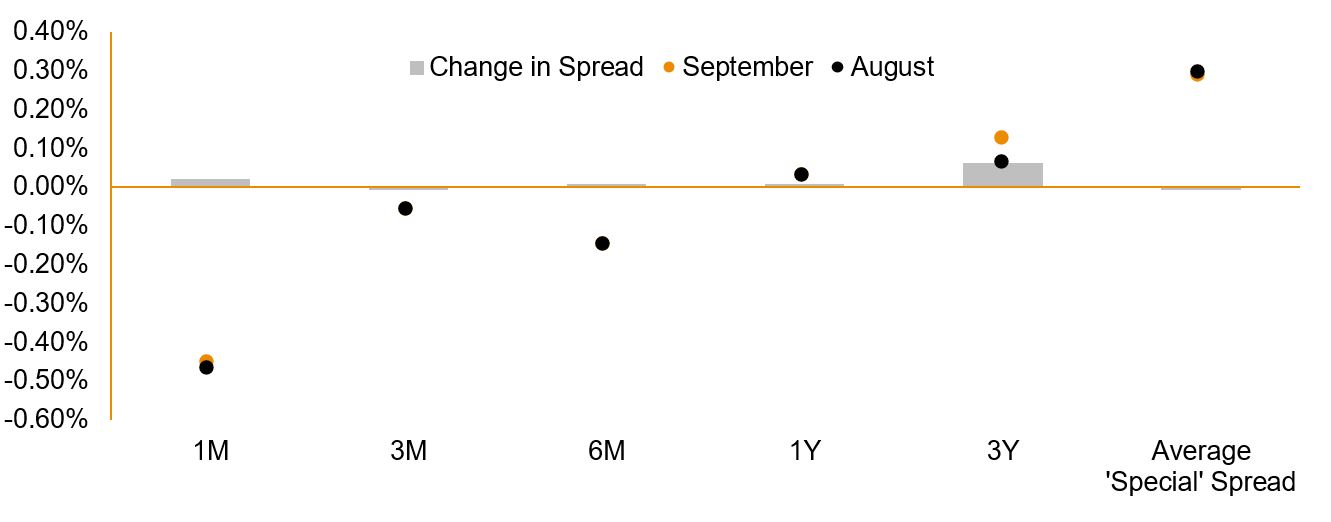

Source: RBA, BondAdviser For full details, charts and commentary, please click here for the full pdf version.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Jul 25, 2026 Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Jul 25, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.