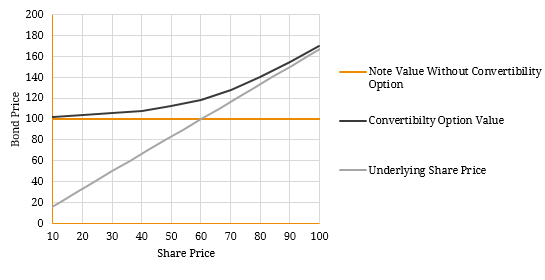

Over the past decade there have been a number of securities that feature the option to convert into ordinary equity at a pre-defined date. The conditions that trigger convertibility vary with each security but given this exposure, the price of security can be impacted by the underlying share price. The ratio of shares the investor receives for each security is generally pre-specified at the issue date and can be adjusted to reflect changes to common equity such as rights issues, share buybacks and stock splits. This is typically known as the conversion price which can be set or variable over the tenor of the security. These types of securities have been more prominent in the past. Some examples include Healthscope Notes I & II (ASX: HLNG, HLNGA) and MYOB Subordinated Notes (ASX: MYBG) which were both partially converted into ordinary equity via an initial public offering of the issuer. Some structured securities give the issuer the option to convert their hybrid securities into ordinary shares. However, the option can also be given to the investor and they can decide what is the most profitable option (redemption, convertibility or some other special scheme). If the option to convert is at the issuer’s discretion, the convertibility component of the security can be viewed as a call option from the company’s perspective (the option to buy the outstanding notes at a pre-set price which are then converted to equity). This is common across some regulated capital securities (i.e. Tier 2 and Tier 1 hybrids). This creates uncertainty around the underlying security, particularly if the notes are trading at a premium to the callable price or if the underlying share price is trading at a discount to the pre-defined conversion price. In general terms, issuers attempt to avoid conversion as it dilutes ordinary shareholders but if a company is in extreme financial distress, it may have no choice. If this occurs, then it is likely the underlying share price has fallen and security holders are now worse off (i.e. the underlying share price is below the conversion price). For this reason, convertibility at the option of the issuer makes a security less valuable than an identical note which does not contain convertibility (known as the Straight Value): Value of Convertible Note = Straight Value – Issuer’s Convertibility Option Value If the option to convert is at the holder’s discretion, the convertibility component of the security can be viewed as a call option from the investor’s perspective (the option to buy the underlying equity at a pre-set price) and will become more valuable as the underlying share price appreciates relative to the conversion price. This is because the investor can convert the hybrid securities at a share price lower than the current market price quoted in the stock market (also referred to as being ‘in-the-money’). However, as the optionality of the security allows the investor to choose whether to convert or continue hold the security until maturity/call date and receive face value. For this reason, the security’s value will be floored by the hypothetical value of an identical note which does not contain convertibility (known as the Straight Value): Value of Convertible Note = Straight Value + Holder’s Convertibility Option Value Figure 1. Convertible Note Components assuming Conversion Price of $50.00 for Issuer Call Option Scenario  Source: BondAdviser A good simple example of the impact convertibility can have on the price of a security is the AFIC Notes (ASX: AFIG) which were issued at the end of 2011. Under the terms of the notes, holders may redeem on maturity or convert the notes into ordinary shares on each Interest Payment Date at a fixed conversion price of $5.0864 per ordinary share. This conversion price was set at a 25% premium to the volume weighted average price of AFIC Ordinary Shares traded during the 5 trading days prior to the issue date of the Notes. Given the security’s semi-annual interest payments, the convertibility of the notes can view as a 6-monthly recurring call option (from the holder’s perspective) on the underlying share price (ASX: AFI). As the AFI share price rose above $5.08 in 2012, the call option component of the security increased in value significantly and became “in-the-money”. This has had a profound impact on valuation as it has distorted the yield and spread on the notes which does not reflect the true credit risk of the underlying issuer. To illustrate this, we graph the historical spread of AFIC notes before and after adjusting for convertibility as well as the price components. Figure 2. Historical AFIC Share Price and Note Price History

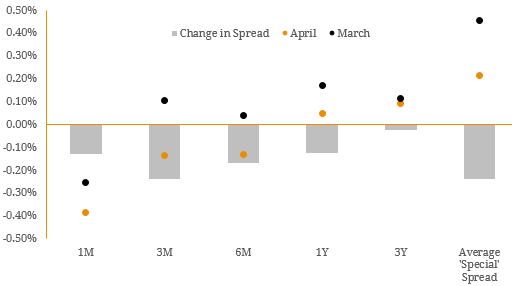

Source: BondAdviser A good simple example of the impact convertibility can have on the price of a security is the AFIC Notes (ASX: AFIG) which were issued at the end of 2011. Under the terms of the notes, holders may redeem on maturity or convert the notes into ordinary shares on each Interest Payment Date at a fixed conversion price of $5.0864 per ordinary share. This conversion price was set at a 25% premium to the volume weighted average price of AFIC Ordinary Shares traded during the 5 trading days prior to the issue date of the Notes. Given the security’s semi-annual interest payments, the convertibility of the notes can view as a 6-monthly recurring call option (from the holder’s perspective) on the underlying share price (ASX: AFI). As the AFI share price rose above $5.08 in 2012, the call option component of the security increased in value significantly and became “in-the-money”. This has had a profound impact on valuation as it has distorted the yield and spread on the notes which does not reflect the true credit risk of the underlying issuer. To illustrate this, we graph the historical spread of AFIC notes before and after adjusting for convertibility as well as the price components. Figure 2. Historical AFIC Share Price and Note Price History  Source: BondAdviser, ASX Figure 3. Standard Spread Vs Option-Adjusted Spread for AFIC Notes

Source: BondAdviser, ASX Figure 3. Standard Spread Vs Option-Adjusted Spread for AFIC Notes  Source: BondAdviser As shown above, the price of AFIG rose as high as ~$120 and it not surprising this resulted in a negative yield to maturity and spread. While these securities are becoming less popular, it is still important to understand the mechanics of optionality and how different convertibility scenarios can impact the price of the security. Due to the exposure the underlying share price, convertibility is another key feature that differentiates hybrid securities from traditional fixed income instruments. Although this feature resulted in a positive outcome for AFIG, the opposite can occur which can result in substantial capital losses. For this reason, investors should have a clear understanding around the structure of the hybrid security they are investing in as another key input into the investment decision making process.

Source: BondAdviser As shown above, the price of AFIG rose as high as ~$120 and it not surprising this resulted in a negative yield to maturity and spread. While these securities are becoming less popular, it is still important to understand the mechanics of optionality and how different convertibility scenarios can impact the price of the security. Due to the exposure the underlying share price, convertibility is another key feature that differentiates hybrid securities from traditional fixed income instruments. Although this feature resulted in a positive outcome for AFIG, the opposite can occur which can result in substantial capital losses. For this reason, investors should have a clear understanding around the structure of the hybrid security they are investing in as another key input into the investment decision making process.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Jul 16, 2026 Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Jul 16, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.