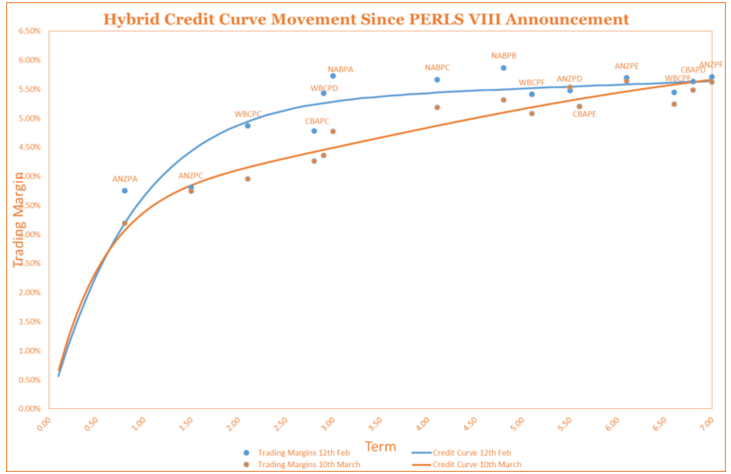

The first chart shows the move in trading margins over the past week: Whilst the rally in securities with an expected call date of less than a year has stalled a little, investors have continued to buy securities between two and three years to the expected call date; and Generally investors continued to ignore longer dated hybrids (i.e. hybrids with a call dates beyond 2020). Chart 1: Major Bank Tier 1 Hybrid Trading Margin Movement (3rd to 10th March 2016) Source: BondAdviser as at 10th March 2016 The second chart looks at the shape of the hybrid yield curve and how it has changed over the month. Hybrids have enjoyed a ‘bull steepener’ as shorter-dated hybrid trading margins have fallen faster than longer-dated hybrid trading margins. Chart 2: Month on Month Hybrid Credit Curve Shift Source: BondAdviser as at 10th March 2016 The third chart again shows how the hybrid credit curve has shifted over the last month. The CBAPE now looks only a little on the expensive side. More importantly, investors who allocated new capital towards short to mid dated hybrids via the secondary market (rather than subscribing to the CBAPE’s) should be ahead. Of course if the curve continues to shift lower over the coming weeks, as we get closer to the listing date of the CBAPE’s, all hybrid holders will benefit. Chart 3: The Hybrid Credit Curve Has Shifted To Meet The New CBA Hybrid  Source: BondAdviser as at 10th March 2016 We remain cautious of longer dated hybrids despite the apparent attractive margins and outright yeilds on offer. As the hybrid credit curve remains relatively flat once you go past four years, investors are not necessarily being rewarded for taking on the additional term risk, i.e. the NABPC hybrid is trading with a margin of 5.19% with an expected term of 4 years whilst the ANZPF is trading at a margin of 5.63% with an expected term of 7 years, a pick up of only 44 basis points for an additional 3 years of risk. Banks balance sheets could look very different over the longer term especially as they continue to come under pressure to respond and restructure due to regulatory and competitive forces.

Source: BondAdviser as at 10th March 2016 We remain cautious of longer dated hybrids despite the apparent attractive margins and outright yeilds on offer. As the hybrid credit curve remains relatively flat once you go past four years, investors are not necessarily being rewarded for taking on the additional term risk, i.e. the NABPC hybrid is trading with a margin of 5.19% with an expected term of 4 years whilst the ANZPF is trading at a margin of 5.63% with an expected term of 7 years, a pick up of only 44 basis points for an additional 3 years of risk. Banks balance sheets could look very different over the longer term especially as they continue to come under pressure to respond and restructure due to regulatory and competitive forces.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.