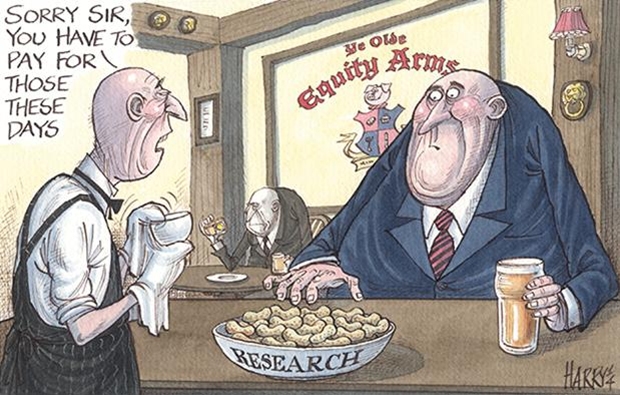

Who should pay for research use when making investment decisions? For a number of years market stakeholders have debated “unbundling” brokerage and research fees stating it promotes competition and transparency. Typically, in Australia, investors pay a flat percentage rate to trade and receive research (and, for professionals, access to company executives via meetings). In a world where the cost of execution is continually dropping, the “advice” component of the overall fee structure is proportionally increasing as part of the bundled model. The advice revolves around matching a clients requirements with appropriate assets and then providing the client with sufficient “unconflicted” information on the assets so they can make an informed decision. In Australia this is done on a best endeavors basis by market participants and has broadly worked. In Europe the market regulators have taken the conflict part of the equation one step further and have introduced research unbundling as part of Markets in Financial Instruments Directive II (MiFiD II). While this is specific to Europe, global regulators will be closely watching its implementation and success. So what is it? Unbundling is the process by which a sell-side firm separates its execution commission from its research spend. Historically, investment managers have used Commission Sharing Agreements (CSA) or other mechanisms to manage that process. This allows a buy-side firm to use the CSAs accrued with its brokers to pay for research from a provider of choice, including independent research houses. MiFID II has proposed a new mechanism known as Research Payment Accounts which allow firms to set an absolute monetary budget to pay for their research to help remove any conflict between between trading activity and research spend. Arguably they are similar mechanisms with slightly different outcomes. Why is it relevant? In August 2016 ASIC released Report 486 “Sell-side research and corporate advisory: Confidential information and conflicts”which touches on research conflicts of interest. The findings of this report are still up for debate but it leads us to believe that ASIC is closely watching the bundling of research services into public offer fees and/or commissions. It will be a long time before any sort of unbundling is enforced in Australia but there are a few forward thinking firms which have already introduced it as best practice. Naturally, many clients wonder why they should pay for research when historically they have not? The answer is simple: research matters and you get what you pay for. Although there is a mass of investment research distributed “free” by investment banks and brokers, the clients, of course, are paying for this through dealing spreads and commissions. But the investment banks and brokers naturally use the distribution of this “free” research to further their own objectives. Independence has always been important in the conduct of research and the provision of advice. These days, though, bearing in mind recent history and the pressures on investment banks, it is probably even more important. One solution is to provide research in-house. This is extremely costly and it is rarely possible to resource internal research departments fully with any quality. It is also easy for an internal research departments to fall into re-affirming the views of senior executives — thereby defeating the object of the exercise. The alternative solution is to buy in independent research from outside—either to complement in-house research services or as a substitute for them. That is the solution we offer. Looking Ahead Against this background, it is difficult to predict just how much the research landscape will evolve in the next few years, but we have no doubt that there will be different configurations to the current market. As with many of industries technology and regulation will change the way research will be consumed in the future. We expect there will be a greater number of independent firms that provide tailored or niche reports, as well as research platforms that amalgamate offerings from different analysts or providers with a varying range of payment options. Whatever the end result, these are positive steps towards an investment research industry that is less fragmented and better able to serve the market.

Who should pay for research use when making investment decisions? For a number of years market stakeholders have debated “unbundling” brokerage and research fees stating it promotes competition and transparency. Typically, in Australia, investors pay a flat percentage rate to trade and receive research (and, for professionals, access to company executives via meetings). In a world where the cost of execution is continually dropping, the “advice” component of the overall fee structure is proportionally increasing as part of the bundled model. The advice revolves around matching a clients requirements with appropriate assets and then providing the client with sufficient “unconflicted” information on the assets so they can make an informed decision. In Australia this is done on a best endeavors basis by market participants and has broadly worked. In Europe the market regulators have taken the conflict part of the equation one step further and have introduced research unbundling as part of Markets in Financial Instruments Directive II (MiFiD II). While this is specific to Europe, global regulators will be closely watching its implementation and success. So what is it? Unbundling is the process by which a sell-side firm separates its execution commission from its research spend. Historically, investment managers have used Commission Sharing Agreements (CSA) or other mechanisms to manage that process. This allows a buy-side firm to use the CSAs accrued with its brokers to pay for research from a provider of choice, including independent research houses. MiFID II has proposed a new mechanism known as Research Payment Accounts which allow firms to set an absolute monetary budget to pay for their research to help remove any conflict between between trading activity and research spend. Arguably they are similar mechanisms with slightly different outcomes. Why is it relevant? In August 2016 ASIC released Report 486 “Sell-side research and corporate advisory: Confidential information and conflicts”which touches on research conflicts of interest. The findings of this report are still up for debate but it leads us to believe that ASIC is closely watching the bundling of research services into public offer fees and/or commissions. It will be a long time before any sort of unbundling is enforced in Australia but there are a few forward thinking firms which have already introduced it as best practice. Naturally, many clients wonder why they should pay for research when historically they have not? The answer is simple: research matters and you get what you pay for. Although there is a mass of investment research distributed “free” by investment banks and brokers, the clients, of course, are paying for this through dealing spreads and commissions. But the investment banks and brokers naturally use the distribution of this “free” research to further their own objectives. Independence has always been important in the conduct of research and the provision of advice. These days, though, bearing in mind recent history and the pressures on investment banks, it is probably even more important. One solution is to provide research in-house. This is extremely costly and it is rarely possible to resource internal research departments fully with any quality. It is also easy for an internal research departments to fall into re-affirming the views of senior executives — thereby defeating the object of the exercise. The alternative solution is to buy in independent research from outside—either to complement in-house research services or as a substitute for them. That is the solution we offer. Looking Ahead Against this background, it is difficult to predict just how much the research landscape will evolve in the next few years, but we have no doubt that there will be different configurations to the current market. As with many of industries technology and regulation will change the way research will be consumed in the future. We expect there will be a greater number of independent firms that provide tailored or niche reports, as well as research platforms that amalgamate offerings from different analysts or providers with a varying range of payment options. Whatever the end result, these are positive steps towards an investment research industry that is less fragmented and better able to serve the market.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Mar 12, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Mar 12, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.