It was a quiet news week in terms of fundamentals for fixed income markets but economic and technical news continues to flow. Over the past week we have had a very large new issue from ANZ (AUD$2.5billion), minutes released from the US Federal Reserve FOMC meeting, implications from the iron ore price collapse and the AOFM selling their first inflation linked bonds at a negative yield.

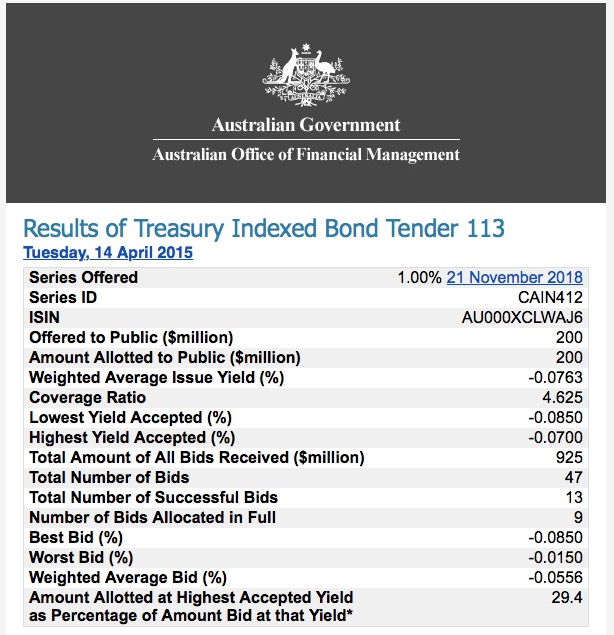

Lets start with negative real yields. On 14 April 2015 the Australian Office of Financial Management (AOFM) sold (see image below) inflation-linked bonds at an average yield below zero (negative 0.076% to be precise). This sale was a tap on an existing funding line (like a line of credit that they can draw on if the price is favourable) and institutional investors ate it up with bids exceeding 4.6x the offer amount. Exceptional but true. What this tells us it that institutional investors (in aggregate) believe there will be no real (that is inflation adjusted) economic growth over the next ~3 years as inflation outpaces growth. This is driven by factors such as higher import (AUD falling) and energy prices (crude oil bouncing off lows) over the past month. The reality is for Australian investors achieving a risk free return over inflation is now very difficult and investors are being forced into higher risk assets to achieve such returns. In our opinion this is unfortunately a sign of things to come and the strategy of buy and hold for deposits and government bonds will most likely in negative real returns in the coming year.

Lets start with negative real yields. On 14 April 2015 the Australian Office of Financial Management (AOFM) sold (see image below) inflation-linked bonds at an average yield below zero (negative 0.076% to be precise). This sale was a tap on an existing funding line (like a line of credit that they can draw on if the price is favourable) and institutional investors ate it up with bids exceeding 4.6x the offer amount. Exceptional but true. What this tells us it that institutional investors (in aggregate) believe there will be no real (that is inflation adjusted) economic growth over the next ~3 years as inflation outpaces growth. This is driven by factors such as higher import (AUD falling) and energy prices (crude oil bouncing off lows) over the past month. The reality is for Australian investors achieving a risk free return over inflation is now very difficult and investors are being forced into higher risk assets to achieve such returns. In our opinion this is unfortunately a sign of things to come and the strategy of buy and hold for deposits and government bonds will most likely in negative real returns in the coming year.

We often get asked the question: “Why does US interest rate policy have an effect on our interest rate market?”. That is a very important question and is currently driven by one key factor: quantitative easing. Historically, there has been a high correlation between the yield in US 10-Year Treasury Bond and the Australian 10-Year Treasury Bond. This is because inflation and economic growth expectations over the long term are driven by the large global economies (not relatively small ones like Australia). For example, if we know that both the United States and China were going to be in recession in 10 years time the probability that we would also be in recession is fairly high. But conversely if we assume the future prosperity was strong then in all likelihood so to would our prosperity be strong. However, over the past few years these traditional dynamics of inflation and economic growth expectations have been distorted by unconventional monetary policy (quantitative easing). This unconventional policy has dictated market performance over the past few years but now this is all starting to unravel.

Last week the Federal Reverse Chairman Janet Yellen’s gave a speech on normalising monetary policy. It basically reiterated that the first hike in US interest rates was likely later this year, but she didn’t get any more specific than that. She stressed that a significant pick-up in core inflation and/or wage growth was not a pre-condition for beginning to raise the fed funds rate and that she only needed to be “reasonably confident” that inflation will climb back to the 2% target within a year or two. So the question remains: How will increasing the fed funds rate impact long term growth expectations? The reality is nobody really knows. Currently markets react sharply to any changes in economic data because small expectation changes result in large % movements in yield. The normalisation of global rates could very easily trigger bond market volatility and broad asset price rebalancing. In our opinion volatility is inevitable but provided US economic data is moving in the right direction we are likely to see our long term growth expectations follow the US and hence long term bond yield will remain highly correlated.

We can talk about US economic policy till the cows come home but it doesn’t change that fact that our preferred investment strategy is to remain invested in short duration investments. Which means investors should be thinking about what the RBA will do rather than what the Fed will do. The recent decision by the RBA to not cut rates is puzzling to all market participants. What it does say is that the RBA is much more cautious with monetary policy than we previously thought and that the hurdle for rate cuts may be higher than what the market thinks. If you are a forced investor who doesn’t know where to invest excess cash we continue to favour “old style” Tier 2 bank debt. These securities are available on and off exchange and generally demand exceeds supply so you will have confidence in limited capital volatility.

Figure 1. Historical Trading Margin (Listed Tier 2 Capital (transitional) vs Listed Tier 2 Capital (Basel 3 compliant))

Finally, to iron ore. Over the past year we have seen the collapse of the Iron Ore trading price as demand from China has effectively dried up and supply from BHP, RIO and Vale has increased substantially (this is probably tactical from there perspective). This price collapse has been predicted by numerous commentators and now even the Federal Treasury is suggesting a price of $35 per tonne is not out of the question. Victims of this price crash are now becoming evident. In the last week Atlas Iron (AS Code: AGO) announced a review of its operations and that it was in discussions with creditors about a resolution – note that it is not yet in “technical” default to its borrowers. On the 13th April Standard and Poor’s announced a second review of its long term iron ore price assumptions which resulted in a number of major Australian issuers being placed on review for downgrade. S&P revised its iron-ore price for 2015 to US$45 a tonne (from US$65 a tonne) and US$50 a tonne for 2016 (from US$65 a tonne). This change should not impact the issuers with solid balance sheets and diversified earnings streams (i.e BHP, RIO) but those leveraged to Iron Ore are at serious risk of default and/or being shut out of capital markets so they will be forced to restructure. This is reflected in the price of some bonds for Fortescue. The chart below shows the traded price (Source: FINRA Trace Database) of the FMG 6.875% 2022 bond (callable in 2017). As you can see there has been a significant selloff in price over the past year but it has fallen sharply over the past month. We do not cover Fortescue as an issuer but if you do have exposure to this issuer we recommend you carefully look at its fundamentals.

The final part of this iron ore puzzle was the second announcement today from Standard and Poor’s saying that the credit rating of Western Australia but may be cut as the states mining royalties weaken which in turn will weaken its budget position over coming years. Timing could be better for the WA premier as the GST distribution debate goes into overdrive.

Figure 2. Iron Ore Price Index