The Australian Banking sector has had a difficult few days on the sharemarket after APRA’s (Australian Prudential Regulation Authority) Chairman Wayne Byres said the recommendation by the Financial Systems Inquiry on increasing mortgage risk weights can be “dealt with sooner rather than later.” To most people this means nothing at all but in technical terms it will make `it significantly harder for banks to achieve the same sort of return on equity they have over the past few years. But from a debt and hybrid investors perspective it just creates a greater capital cushion for for any unexpected losses.

OK, so lets break this down into reality. Currently, the big four banks (and Macquarie) use whats known as an “advanced internal ratings based model” to assess the risk of residential mortgages on their balance sheet, whereas other banks use a standardised model. These models were approved for use in 2009 by APRA as part of the Basel II accord which was implemented to address a fairly archaic risk model in Basel I.

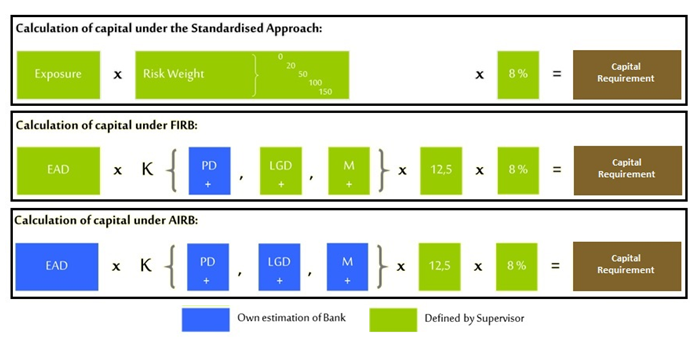

This internal ratings based model can be broken down into:

This internal ratings based model can be broken down into:

- the ‘foundation’ model where the probability of default data is supplied by the bank but the other default data is provided by formula set by the Basel II committee.

- the ‘advanced’ model, which is the choice of all majors primarily because they can choose and / or influence the majority of inputs into the model.

While this is a bit technical and confusing, the reality is these models are the primary driver of leverage within a bank and hence they are very important in terms of the risk / reward across the capital structure. Part of the reason bank shares have been selling off is because of the “PD” part of the equation above. The “PD” is probability of default and over the past few years the banks have been slowly reducing this measure as they claim that the risk in their mortgage books reflect strong historical mortgage data. While this is true the problem is the banks improved technology allows them to use these models to their advantage by changing the composition of the loan portfolios so they can hold less capital against mortgages. In December the Financial System Inquiry recommended lenders hold an average mortgage risk weight of 25 – 30% relative to the current average of 18% held by the biggest four banks. Since then all kinds of numbers have been discussed about what would be the capital cost for full implementation of the financial system inquiry’s recommendations. In our opinion its about $15bn in extra capital requirements (across the big four) which translates to an increase in core equity tier 1 (CET1) ratios of ~50bps-110bps for NAB and ANZ and ~80bps-150bps for WBC and CBA. This might sound like a lot but in reality it’s about 12-18 months of organic capital contribution (assuming all contributing factors stay the same).