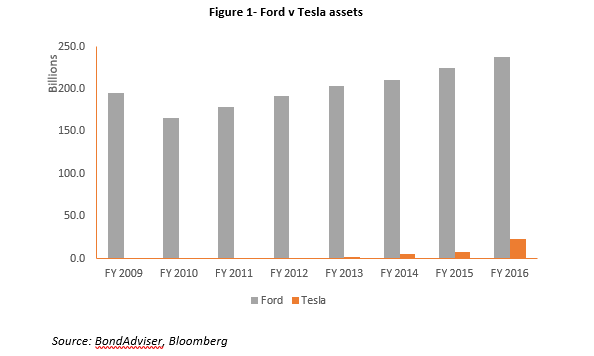

Over the past few years, futuristic car-maker Tesla has grown into arguably the market leader in energy-efficient auto-manufacturing. The group’s equity market capitalisation reached US$45.5 billion earlier this year in March, surpassing Ford’s US$45.4 billion for the first time. However, given the latter boasts revenue and assets of US$151.8 billion and US$238 billion respectively versus Tesla’s US$7 billion and US$22.7 billion in FY16, equity investors are clearly pricing the company’s significant growth expectations. Figure 1. Ford v Telsa Assets  Source: BondAdviser, Bloomberg Investors high expectations of company performance in the not-to-distant-future is largely based on the growing number of people transitioning towards eco-friendly products in response to (not least) climate change concerns. For the auto industry, this clearly means a higher adoption of high-tech hybrid and electric vehicles as battery prices decline and governments ban or plan to ban new petrol cars in around 20 years or so (notably Britain and France but with China recently indicating this too). The highly likely ultimate replacement of carbon-based fuels with stored electricity (ignoring the initial electrical generation source) to power the wheels is attracting more and more investors. In August 2017, Tesla embarked on a capital raising to finance its “Model 3” product line and create a larger cash buffer for existing investors. Rather than again tapping equity or hybrid markets, this time Tesla opted to issue an inaugural senior debt instrument, offering US$1.5 billion of 8-year high-yield bonds. Figure 1. US Corporate Bond Yield Curves by Credit Ratings

Source: BondAdviser, Bloomberg Investors high expectations of company performance in the not-to-distant-future is largely based on the growing number of people transitioning towards eco-friendly products in response to (not least) climate change concerns. For the auto industry, this clearly means a higher adoption of high-tech hybrid and electric vehicles as battery prices decline and governments ban or plan to ban new petrol cars in around 20 years or so (notably Britain and France but with China recently indicating this too). The highly likely ultimate replacement of carbon-based fuels with stored electricity (ignoring the initial electrical generation source) to power the wheels is attracting more and more investors. In August 2017, Tesla embarked on a capital raising to finance its “Model 3” product line and create a larger cash buffer for existing investors. Rather than again tapping equity or hybrid markets, this time Tesla opted to issue an inaugural senior debt instrument, offering US$1.5 billion of 8-year high-yield bonds. Figure 1. US Corporate Bond Yield Curves by Credit Ratings  Source: BondAdviser, Bloomberg Interestingly, the initial yield of 5.30% (which is also the coupon rate given that the security issued at par) appeared to be considerably lower than comparable securities. As Tesla’s bond was rated B3/B- by the credit rating agencies, the market-based yield for this risk level should be around 5.8% according to the relevant US high-yield yield curve (Figure 1). However, the approximate 0.50% yield differential did not compromise investors’ confidence on the issuer’s prospective performance and the offering was even upsized to US$1.8 billion due to this high demand. In addition, this offering has placed Tesla in a similar ballpark to BB rated corporates (the approximate yield for BB rated corporates is 5.1%) regardless of Tesla’s weaker financial performances (it has made substantial losses for the past few years). Tesla’s issue readily demonstrates the differing viewpoints on companies by investors and credit rating agencies. More specifically, credit rating agencies are very evidence-based and their thoughts will be more backward loomoking. From a credit rating perspective, an upgrade (or downgrade) often only occurs when the financial situations of a company have soundly evidenced improvement (or deterioration). In contrast, investors would probably consider more prospective factors into the decision making process as they are the ones who actually bear the risk (and potential loss). This highlights that credit ratings are only one piece of the credit analysis puzzle and should be utilised as one of many inputs in the investment process. Overall, Tesla’s successful high-yield bond sale was attributable to investors being positive on the corporates’ outlook over a longer-term and its ability to partially address global concerns on environmental issues. For our part, we would be concerned about Tesla’s continued lack of profits, high capital expenditure requirements, significant project risk and substantial cash-burn. And that’s not even including creditor-protective bond terms normally found in high-yield issues. We believe that we could very well be revisiting the Tesla bond story in 2018 and perhaps not in a positive light.

Source: BondAdviser, Bloomberg Interestingly, the initial yield of 5.30% (which is also the coupon rate given that the security issued at par) appeared to be considerably lower than comparable securities. As Tesla’s bond was rated B3/B- by the credit rating agencies, the market-based yield for this risk level should be around 5.8% according to the relevant US high-yield yield curve (Figure 1). However, the approximate 0.50% yield differential did not compromise investors’ confidence on the issuer’s prospective performance and the offering was even upsized to US$1.8 billion due to this high demand. In addition, this offering has placed Tesla in a similar ballpark to BB rated corporates (the approximate yield for BB rated corporates is 5.1%) regardless of Tesla’s weaker financial performances (it has made substantial losses for the past few years). Tesla’s issue readily demonstrates the differing viewpoints on companies by investors and credit rating agencies. More specifically, credit rating agencies are very evidence-based and their thoughts will be more backward loomoking. From a credit rating perspective, an upgrade (or downgrade) often only occurs when the financial situations of a company have soundly evidenced improvement (or deterioration). In contrast, investors would probably consider more prospective factors into the decision making process as they are the ones who actually bear the risk (and potential loss). This highlights that credit ratings are only one piece of the credit analysis puzzle and should be utilised as one of many inputs in the investment process. Overall, Tesla’s successful high-yield bond sale was attributable to investors being positive on the corporates’ outlook over a longer-term and its ability to partially address global concerns on environmental issues. For our part, we would be concerned about Tesla’s continued lack of profits, high capital expenditure requirements, significant project risk and substantial cash-burn. And that’s not even including creditor-protective bond terms normally found in high-yield issues. We believe that we could very well be revisiting the Tesla bond story in 2018 and perhaps not in a positive light.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Dec 12, 2025Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Dec 12, 2025Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.