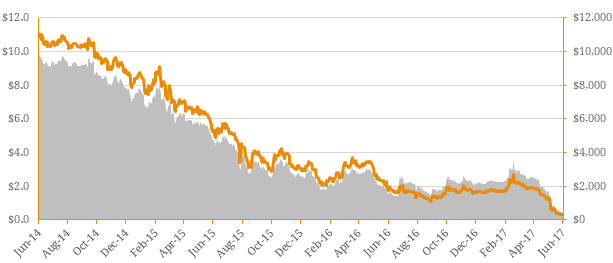

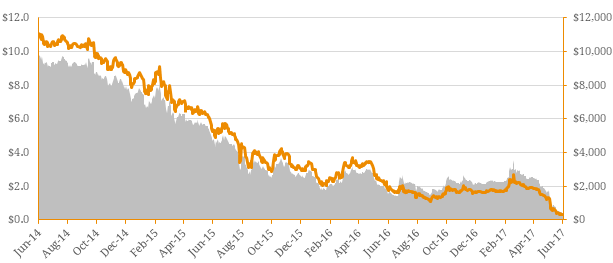

Over the past few years, Noble Group (SGD: NOBL), once Asia’s largest commodity trader, has experienced a significant decline in profitability following a downturn in the commodities market coinciding with accusations of overstating its accounts. After reporting an unexpected quarterly loss, Noble’s woes deepened when it announced that it may not be profitable until 2019, sparking concerns it would not be able to service its $3.2 billion debt pile. In response, the credit rating agencies cut their ratings on the company, expressing concern about the possibility Noble Group may not meet its interest obligations. More specifically, Standard & Poor’s announced that the debt load for the group was unsustainable given current earnings path and flagged a risk of default within a year, triggering a mass sell-off in the company’s stocks and bonds. Figure 1. Noble’s share price and Market Capitalisation  Source: Bloomberg There has been a considerable effort to stay afloat through strict cost discipline and large asset sales and the majority of the capital raised ($3 billion) has been used to repay existing debt. At present, Noble Group has three major maturities over the next 12 months: • $656 million due in 2017, of which $620 million are borrowing facilities due in June 2017; • $379 million under a medium-term note program due in March 2018; and • $1.14 billion in revolving credit facilities due in May 2018. Beyond that, the group has senior unsecured bonds due in 2020 and 2022 (an additional $1.92 billion). While the company has adequate funds to cover maturities in 2017, Moody’s highlighted a $900 million liquidity gap where there is only ~$1.2 billion of accessible funding to pay ~$2.1 billion of obligations due by mid-2018. Figure 2. Group Debt Maturity Profile as at 31st March 2017

Source: Bloomberg There has been a considerable effort to stay afloat through strict cost discipline and large asset sales and the majority of the capital raised ($3 billion) has been used to repay existing debt. At present, Noble Group has three major maturities over the next 12 months: • $656 million due in 2017, of which $620 million are borrowing facilities due in June 2017; • $379 million under a medium-term note program due in March 2018; and • $1.14 billion in revolving credit facilities due in May 2018. Beyond that, the group has senior unsecured bonds due in 2020 and 2022 (an additional $1.92 billion). While the company has adequate funds to cover maturities in 2017, Moody’s highlighted a $900 million liquidity gap where there is only ~$1.2 billion of accessible funding to pay ~$2.1 billion of obligations due by mid-2018. Figure 2. Group Debt Maturity Profile as at 31st March 2017  Figure 3. Group Debt Metrics

Figure 3. Group Debt Metrics  Source: Company Reports, Bloomberg The company has announced a strategic review of the business and is negotiating with banks to sign a new credit line or alternatively roll-over a $2 billion credit facility until the end of the year, secured on its inventories and working capital. This would give Noble further time to find new investors, sell assets, or close unprofitable businesses to remain viable, but the likelihood of the bail-in will depend on how much the lenders believe the credibility of the management and its strategic direction. Figure 4. Year-to-date Performance of Noble securities

Source: Company Reports, Bloomberg The company has announced a strategic review of the business and is negotiating with banks to sign a new credit line or alternatively roll-over a $2 billion credit facility until the end of the year, secured on its inventories and working capital. This would give Noble further time to find new investors, sell assets, or close unprofitable businesses to remain viable, but the likelihood of the bail-in will depend on how much the lenders believe the credibility of the management and its strategic direction. Figure 4. Year-to-date Performance of Noble securities  Source: Bloomberg The risk of default is now priced into both the stock and debt markets by investors. The company’s shares have fallen 83.4% since the beginning of the year, the company’s bonds are now trading at less than 36% of face value and credit default swap prices have soared. The company’s market value has shrunk from $6 billion in early 2015 to a little over $300 million. Even if Noble manages to buy more time from lenders, it is an uphill battle. The steep decline on the back of rating actions and poor performance highlights the negative investor sentiment and demonstrates how sheer momentum can drive a company’s value into the ground at all levels of the capital structure.

Source: Bloomberg The risk of default is now priced into both the stock and debt markets by investors. The company’s shares have fallen 83.4% since the beginning of the year, the company’s bonds are now trading at less than 36% of face value and credit default swap prices have soared. The company’s market value has shrunk from $6 billion in early 2015 to a little over $300 million. Even if Noble manages to buy more time from lenders, it is an uphill battle. The steep decline on the back of rating actions and poor performance highlights the negative investor sentiment and demonstrates how sheer momentum can drive a company’s value into the ground at all levels of the capital structure.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Apr 27, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Apr 27, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.