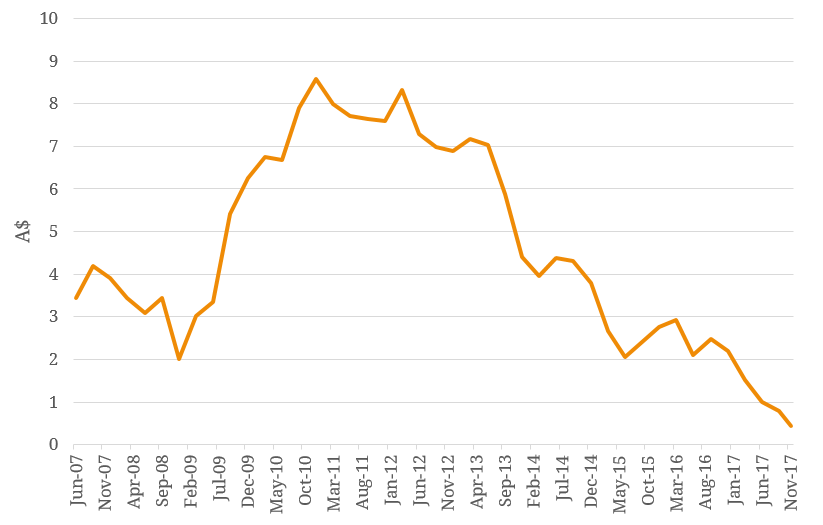

The seventy-nine year-old luxury handbag retailer Oroton became the latest high-profile victim of the changing retail landscape in Australia, when it entered voluntary administration on 29 November 2017. Its’ stores will continue to trade and employ staff on a business-as-usual basis while administrators attempt to find a resolution, most likely through a white-knight buyer. Oroton first listed on the ASX in 1987 and its shares have climbed steadily ever since, reaching an all-time high of $8.50 at the end of 2010. Since then, the company’s shares have declined to just $0.44 (as at the date of suspension due to the voluntary administration announcement), reflecting the current troubles plaguing the brand and the sector (Figure 1 below). Figure 1: Oroton Share Price (ASX)  Source: BondAdvisor, Bloomberg While the decline in profitability of Oroton’s is nothing new to equity followers, its woes became irrecoverable in 2017. First-half results in March saw revenues down 10%, EBITDA reduced by 44% and NPAT severely decreased by 52%. At this point, the company carried no debt and had $5.2m in cash. Its full-year results in September showed a $5.4m net debt liability and $14m in drawn bank facilities provided by Westpac (part-supported by a substantial shareholder) and the company made a net loss of $14.3m, after teetering on the edge of loss for the two prior years. What were the forces causing Oroton’s demise? It is not unreasonable to argue that Oroton’s decline was less of a financial or operational mis-management than more a brand mis-positioning coupled with poor strategic focus. The group had been largely debt-free for most of the past 10 years and had been successfully retaining earnings up until 2013. Its credit and liquidity metrics had also not been too out of line. From an operational perspective, it had not been a poor performer either. In fact, its key operational efficiency metrics have generally been much stronger than some listed international peers in the luxury fashion segment (Figures 2 and 3 below). Figure 2. Cash Conversion Cycle – Oroton vs LVMH

Source: BondAdvisor, Bloomberg While the decline in profitability of Oroton’s is nothing new to equity followers, its woes became irrecoverable in 2017. First-half results in March saw revenues down 10%, EBITDA reduced by 44% and NPAT severely decreased by 52%. At this point, the company carried no debt and had $5.2m in cash. Its full-year results in September showed a $5.4m net debt liability and $14m in drawn bank facilities provided by Westpac (part-supported by a substantial shareholder) and the company made a net loss of $14.3m, after teetering on the edge of loss for the two prior years. What were the forces causing Oroton’s demise? It is not unreasonable to argue that Oroton’s decline was less of a financial or operational mis-management than more a brand mis-positioning coupled with poor strategic focus. The group had been largely debt-free for most of the past 10 years and had been successfully retaining earnings up until 2013. Its credit and liquidity metrics had also not been too out of line. From an operational perspective, it had not been a poor performer either. In fact, its key operational efficiency metrics have generally been much stronger than some listed international peers in the luxury fashion segment (Figures 2 and 3 below). Figure 2. Cash Conversion Cycle – Oroton vs LVMH  Source: BondAdvisor, Bloomberg Figure 3. Inventory to Cash Days – Oroton vs LVMH

Source: BondAdvisor, Bloomberg Figure 3. Inventory to Cash Days – Oroton vs LVMH  Source: BondAdvisor, Bloomberg It follows that Oroton’s troubles may have stemmed from external factors in which it did not have the capacity or ability to cope with. Firstly, Australia is geographically distant from major fashion centres in the northern hemisphere, and it has not produced a lasting, dominant and internationally recognised brand name. Oroton’s attempted high-end brand positioning, which came complete with the accompanying high margins, failed to gain a foothold in international markets. For domestic efforts, given Australia’s calendar-climate-reversal with the northern hemisphere, it has become the ideal ground for top international high-end brands to clear off-season inventory and engage in price wars which Oroton had little answer for. Unable to compete with top-end brands for premium-paying customers both offshore and onshore, Oroton lost ground to second-tier, so-called “light luxury” brands from overseas such as Kate Spade, Marc Jacobs and Michael Kors. Given the ongoing internationalisation of fashion, Australian brands, which do not come with instant brand recognition and do not have a competitive supply chain, cannot compete on price. This reality is not just confined to the higher-end of the market. At the discount-end, ASX-listed Specialty Fashion Group (with brands including Rivers, Millers, Katies and City Chic) has also been struggling recently with large-scale store closures. On a brighter note for expansionary Australian retailers, there have been a few encouraging examples in the market – Smiggle is now established in the UK market thanks to its innovative designs on the back of impressive profits. Forever New has similarly branched into China, Indonesia and India. This could show that the rational way forward for Australian retailers may be to pursue a differentiation strategy that seeks to find a unique position in a niche market, rather than pursue international markets on a blanket-basis, given the limited breathing space in the local Australian market.

Source: BondAdvisor, Bloomberg It follows that Oroton’s troubles may have stemmed from external factors in which it did not have the capacity or ability to cope with. Firstly, Australia is geographically distant from major fashion centres in the northern hemisphere, and it has not produced a lasting, dominant and internationally recognised brand name. Oroton’s attempted high-end brand positioning, which came complete with the accompanying high margins, failed to gain a foothold in international markets. For domestic efforts, given Australia’s calendar-climate-reversal with the northern hemisphere, it has become the ideal ground for top international high-end brands to clear off-season inventory and engage in price wars which Oroton had little answer for. Unable to compete with top-end brands for premium-paying customers both offshore and onshore, Oroton lost ground to second-tier, so-called “light luxury” brands from overseas such as Kate Spade, Marc Jacobs and Michael Kors. Given the ongoing internationalisation of fashion, Australian brands, which do not come with instant brand recognition and do not have a competitive supply chain, cannot compete on price. This reality is not just confined to the higher-end of the market. At the discount-end, ASX-listed Specialty Fashion Group (with brands including Rivers, Millers, Katies and City Chic) has also been struggling recently with large-scale store closures. On a brighter note for expansionary Australian retailers, there have been a few encouraging examples in the market – Smiggle is now established in the UK market thanks to its innovative designs on the back of impressive profits. Forever New has similarly branched into China, Indonesia and India. This could show that the rational way forward for Australian retailers may be to pursue a differentiation strategy that seeks to find a unique position in a niche market, rather than pursue international markets on a blanket-basis, given the limited breathing space in the local Australian market.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© May 2, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© May 2, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.