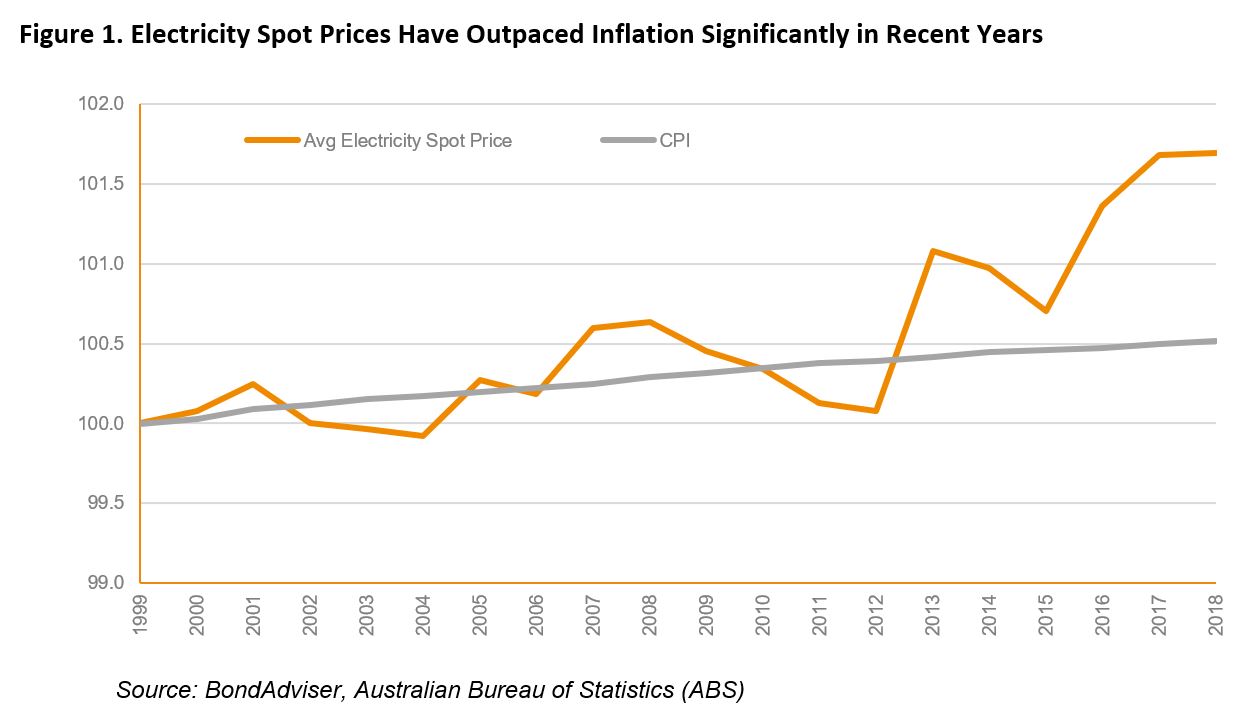

Given the prominence of the Financial Services Royal Commission and increased foreign activity in the M&A space so far this year, regulators such as the Australian Securities and Investments Commission (ASIC) and the Australian Prudential Regulation Authority (APRA) have regularly appeared in our news feeds. Last week, however, it was the Australian Energy Regulator (AER) and the Australian Competition and Consumer Commission (ACCC) making waves in the Utilities sector in two important, yet independent, releases in consecutive days. Figure 1. Electricity Spot Prices Have Outpaced Inflation Significantly in Recent Years  Source: BondAdviser, Australian Bureau of Statistics (ABS) Domestic electricity and gas prices have risen significantly over the past decade, putting the squeeze on Australian households and the end consumer. Energy bills can be broken down into three broad components: wholesale costs, network charges and a retail margin. Whilst retail margins have compressed significantly due to heightened competition, the other two components have together contributed to the outpacing of utilities charges relative to household income seen in figure 1 below. Wholesale energy costs are largely benchmarked by the energy regulator, the AER and Australian Energy Market Commission (AEMC). The cost level is largely driven by macro factors including domestic supply and demand, as well as the cost of broader commodities such as oil. The largest change has come from network charges, being the cost of delivering the energy via infrastructure, which has been the vehicle of choice in which network operators pass on the costs to the end consumer. In doing so, network operators such as AusNet Services (ASX: AST) and APA Group (ASX: APA) have been able to maintain profitability margins and in the case of the latter, become an attractive M&A target for foreign investment. Figure 2. Spreads on Debt Instruments Stable amid Equity Slump

Source: BondAdviser, Australian Bureau of Statistics (ABS) Domestic electricity and gas prices have risen significantly over the past decade, putting the squeeze on Australian households and the end consumer. Energy bills can be broken down into three broad components: wholesale costs, network charges and a retail margin. Whilst retail margins have compressed significantly due to heightened competition, the other two components have together contributed to the outpacing of utilities charges relative to household income seen in figure 1 below. Wholesale energy costs are largely benchmarked by the energy regulator, the AER and Australian Energy Market Commission (AEMC). The cost level is largely driven by macro factors including domestic supply and demand, as well as the cost of broader commodities such as oil. The largest change has come from network charges, being the cost of delivering the energy via infrastructure, which has been the vehicle of choice in which network operators pass on the costs to the end consumer. In doing so, network operators such as AusNet Services (ASX: AST) and APA Group (ASX: APA) have been able to maintain profitability margins and in the case of the latter, become an attractive M&A target for foreign investment. Figure 2. Spreads on Debt Instruments Stable amid Equity Slump  Source: BondAdviser, Bloomberg As Australian energy reliability and affordability has risen to prominence, the issue has become not only an affordability crisis, but also a public relations and political football. This has manifested in many forms, from Tasmania’s infamous Basslink issues to the Australian New Energy Guarantee (NEG) debate to the “Battle of the Billionaires”, in which Sanjeev Gupta and Elon Musk have gently (so far) tussled for supremacy in the South Australian renewables sector. Figure 3. Australia’s Energy Production is Heavily Reliant on Non-Renewable Sources

Source: BondAdviser, Bloomberg As Australian energy reliability and affordability has risen to prominence, the issue has become not only an affordability crisis, but also a public relations and political football. This has manifested in many forms, from Tasmania’s infamous Basslink issues to the Australian New Energy Guarantee (NEG) debate to the “Battle of the Billionaires”, in which Sanjeev Gupta and Elon Musk have gently (so far) tussled for supremacy in the South Australian renewables sector. Figure 3. Australia’s Energy Production is Heavily Reliant on Non-Renewable Sources  Source: BondAdviser, ABS With last week’s drafting of the Rate of Return Guidelines, the AER has finally taken steps to regulate and act in the face of these ongoing developments. AER Chair Paula Conboy announced that the outlined changes could reduce household energy bills by $30-40 per annum, whilst the network operators would experience a 0.45% decrease in the Rate of Return compared to the existing 2013 Guidelines. We note that this is simply a draft at present, with the final report due in December 2018, and await confirmation before determining the credit implications of the regulation (which we expect to be mildly credit negative at worst). Figure 4. Electricity Futures Indicate Lower, More Stable Prices on the Horizon

Source: BondAdviser, ABS With last week’s drafting of the Rate of Return Guidelines, the AER has finally taken steps to regulate and act in the face of these ongoing developments. AER Chair Paula Conboy announced that the outlined changes could reduce household energy bills by $30-40 per annum, whilst the network operators would experience a 0.45% decrease in the Rate of Return compared to the existing 2013 Guidelines. We note that this is simply a draft at present, with the final report due in December 2018, and await confirmation before determining the credit implications of the regulation (which we expect to be mildly credit negative at worst). Figure 4. Electricity Futures Indicate Lower, More Stable Prices on the Horizon  Source: BondAdviser, ABS For its part, the ACCC released its final report on Retail Electricity Pricing on Thursday, to conclude the double whammy to the Utilities sector just one day after the AER’s release. The report can be found here, and it discusses the drivers of rising prices and (limited) recommendations for action going forward. Some of the key recommendations centre on State and Federal government involvement in the Australian Energy Market (AEM)but more of an industry-wide, structural focus than the AER. It is also worth noting that much of the report acknowledges that actual changes will be largely driven by the AER Guidelines. On Monday 16th July, ratings agency Moody’s noted that the proposed regulation was credit negative for “unregulated utilities such as AGL Energy and Origin Energy”, stating that the introduction of a “government-set retail offer price” is likely to result in lower sectoral earnings due to lower retail electricity margins. Overall, detailed and objective analysis of the Australian energy markets is often muddied by the media and political usage of the situation. The true impact of the latest regulatory changes in the sector will likely remain unknown until early 2019, but we believe this represents an important step to begin to address some key issues outside of the political arena, whilst also acknowledging the likely credit negative impact of the proposed changes.

Source: BondAdviser, ABS For its part, the ACCC released its final report on Retail Electricity Pricing on Thursday, to conclude the double whammy to the Utilities sector just one day after the AER’s release. The report can be found here, and it discusses the drivers of rising prices and (limited) recommendations for action going forward. Some of the key recommendations centre on State and Federal government involvement in the Australian Energy Market (AEM)but more of an industry-wide, structural focus than the AER. It is also worth noting that much of the report acknowledges that actual changes will be largely driven by the AER Guidelines. On Monday 16th July, ratings agency Moody’s noted that the proposed regulation was credit negative for “unregulated utilities such as AGL Energy and Origin Energy”, stating that the introduction of a “government-set retail offer price” is likely to result in lower sectoral earnings due to lower retail electricity margins. Overall, detailed and objective analysis of the Australian energy markets is often muddied by the media and political usage of the situation. The true impact of the latest regulatory changes in the sector will likely remain unknown until early 2019, but we believe this represents an important step to begin to address some key issues outside of the political arena, whilst also acknowledging the likely credit negative impact of the proposed changes.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© May 31, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© May 31, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.