The Elders Hybrid (ASX: ELDPA) story is an interesting one as it highlights the complexity of capital management. Following Elders’ announcement last week to undergo an equity capital raising to facilitate the on-market buy-back of its outstanding hybrid securities, we believe it is a good opportunity to revisit Elders’ recent history for future reference in regards to perpetual securities. The History Back in April 2006, Futuris Corporation Limited (named changed to Elders Limited in 2009) issued ELDPA raising $150 million. The securities were structured perpetual, subordinated, convertible, unsecured notes and distributions were discretionary, floating rate, preferred and non-cumulative. The interest rate margin was set at 2.20% p.a. above the 90-Day BBSW until the First Remarketing Date on the 30th of June 2011. Under the terms of the hybrids Elders had the right (but not the obligation) to Convert or Resell some or all ELDPA units on the last business day before any Remarketing Date (every 5 years), or at other times under special circumstances. Like many companies leading up to the Global Financial Crisis (GFC), Elders grew too quickly and was hit hard by the accelerated deterioration in global economic conditions and customer confidence. As a result, reported gearing peaked at 112% at the end of 2008 and the group was forced to sell non-core assets to ensure viability. To recapitalise and refinance the company, the following key initiatives were completed:

- Equity raising of up to $550 million

- Restructure of debt funding with bulk of term debt on 3-year term

- Gross proceeds of $700 million from asset sales

Under the debt restructuring, Elders became subject to 3-year covenant package as shown in the table below. This included ceasing distributions on ELDPA until the 30th of September 2011. The knock on effect of this was that common equity dividends and capital distributions may not be made to Elders ordinary shareholders until the last 12 months of unpaid distributions are paid to noteholders (this was part of the terms of the hybrid transaction). As a result, payment of dividends to ordinary shareholders were suspended also. Table 1. Covenant Package

| Covenant Package | FY10 | FY11 | FY12 | |

| Gross Debt/EBITDA | Less than | 6.0x | 3.75x | 2.5x |

| EBITDA/Interest | Greater than | 1.2x | 2.5x | 3.25x |

| Gearing (Gross Debt/Equity) | Less than | 60% | 55% | 45% |

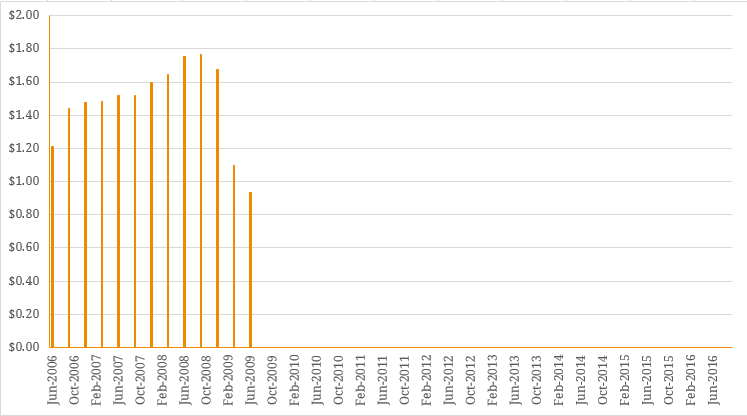

Source: Company Reports During the suspension period, the first Remarketing Date passed (June 2011) and Elders announced that it had elected not to initiate a remarketing process as it was not in financial position to do so. Therefore, the margin on suspended distributions stepped by 2.50% p.a. under the terms of the issue and value of ELPDA declined sharply. The next remarketing date was on the 30th of June 2016 and would result in additional 2.50% p.a. margin step-up if the notes were not resold or converted into ordinary shares (or bought back on-market as they currently are). Leading up to the end of the suspension period, Elders refinanced into a new 1-year facility under much less restrictive terms including no restriction on the payment of distributions to ELDPA holders. However, as “debt reduction (was $346 million at the time) remained the primary concern” of Elders, management announced that the resumption of hybrid distributions would not be considered until the end of the 2012 financial year. Once this point was reached, Elders was still in the process of strategic asset sales and needed to extend the debt facilities before they could be repaid with the proceeds. This was granted but included the prohibitions on the on the payment of distribution to hybrid holders and resulted in another emphatic price decline as shown in the price graph below. As a result, suspended distributions continued until the debt facility was repaid. The debt facility was finally repaid in 2014 and management refocused the direction of the business. This included a fresh equity raising that announced the “priority for the short to medium term is to direct cashflow back into re-invigorating and strengthening the business to grow earnings and returns”. As a result, management outlined that hybrid distributions were unlikely to resume in the next 2-3 years which continued up to last week’s on-market buy-back offer. This was welcomed by the market and the hybrids increased in price significantly over the next 2-year period until August 2015 where Elders notified the ASX of its on-market purchase of 375,000 hybrids at a price of $80 ($30 million buy-back) in an attempt to “normalise its capital structure”. Following this purchase 1,125,000 hybrid securities were left outstanding. Figure 1. ELDPA Cash DistributionsSource: Company Reports With the second Remarketing Date approaching (30 June 2016) and the company’s intention to re-commence paying ordinary dividends by September 2016, Elders underwent an equity capital raising to facilitate the on-market purchase of the majority, if not all, of the remaining hybrids. The only clear motive for this action, rather than conversion on the last business day before the 30th of June 2016, is that management believe they can buy back the hybrids at a price below par value ($100). Elders has outlined the buy-back price at $95. As at the 17th of June, Elders had bought back more than 52% of the hybrids. Figure 2. ELDPA Price History  Source: Bloomberg The implications As shown in the price graph above, capital management can have a major influence on price action. Bank debt and other debt obligations (i.e. senior bonds) rank above subordinated perpetual securities and as a result, covenants and conditions embedded in higher-ranking debt can restrict the flexibility of hybrid securities. This can occur especially when the issuer is in financial distress as seen in the Elders case. The restriction of dividends in an effort to recapitalise the company over a 5-year transitional period while protecting more senior creditors forced the price of ELDPA to less than $10. The restrictive covenants, along with the overall credit profile of the company were the primary drivers of the hybrids over their lifetime and were both dictated heavily by Elders’ capital management policies. Therefore, when analysing any hybrid security (especially perpetuals) it is essential to understand the underlying issuer’s debt facilities and securities and how different terms and conditions have an impact on other parts of the capital structure.

Source: Bloomberg The implications As shown in the price graph above, capital management can have a major influence on price action. Bank debt and other debt obligations (i.e. senior bonds) rank above subordinated perpetual securities and as a result, covenants and conditions embedded in higher-ranking debt can restrict the flexibility of hybrid securities. This can occur especially when the issuer is in financial distress as seen in the Elders case. The restriction of dividends in an effort to recapitalise the company over a 5-year transitional period while protecting more senior creditors forced the price of ELDPA to less than $10. The restrictive covenants, along with the overall credit profile of the company were the primary drivers of the hybrids over their lifetime and were both dictated heavily by Elders’ capital management policies. Therefore, when analysing any hybrid security (especially perpetuals) it is essential to understand the underlying issuer’s debt facilities and securities and how different terms and conditions have an impact on other parts of the capital structure.