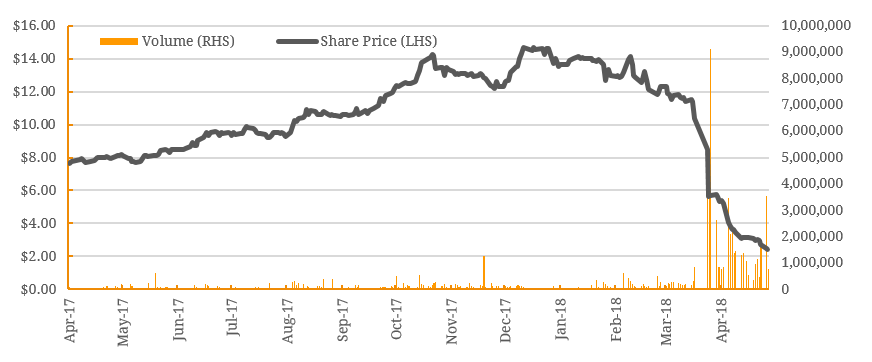

Look-through earnings was a concept widely attributed to legendary investor Warren Buffet, famed for his ability to value companies and achieve exceptional returns. The idea behind “look-through earnings” is that an investor should not just look at a company’s reported accounting earnings, but instead analyse earnings from subsidiaries and associated parties that would flow through to shareholders in the form of dividends, either paid or reinvested. The same concept of earnings can similarly be applied to debt, which is particularly important for fixed income investors to manage their total risk exposure. The recent case of alternative asset manager Blue Sky Alternative Investments Limited (ASX: BLA) provides an indication of why look-through debt can be so important for investors. BLA has reported Assets Under Management (AUM) of ~$4 billion, a number that has been disputed in a fierce and public battle with U.S. hedge fund and short-seller, Glaucus Research (“Glaucus”), which has had a devastating effect on BLA’s share price, seen below. Figure 1. Investors haven’t been impressed with Blue Sky’s poor disclosure  Source: BondAdviser, Bloomberg The reason for this spectacular plummet from $14.12 on 20 February 2018 to $2.40 on 8 May 2018, representing an 83% decline in less than 3 months was largely due to opaque reporting and look-through debt. BLA recently admitted that up to 20% of its reported AUM is in the form of undrawn debt facilities, a revelation that has led many analysts to question how faithfully this represents the true financial position of the company. Additionally, BLA recently disclosed a number of loan agreements with their private subsidiaries (i.e. Blue Sky La Trobe Street Fund), with several funds taking intercompany loans from BLA at 10% interest, which flows to reported earnings. Whilst within the bounds of disclosure requirements, opaque information makes it difficult for investors to determine what the risk and return profile of an entity such as BLA (and its funds) may truly be. Figure 2. Example of Blue Sky intercompany lending

Source: BondAdviser, Bloomberg The reason for this spectacular plummet from $14.12 on 20 February 2018 to $2.40 on 8 May 2018, representing an 83% decline in less than 3 months was largely due to opaque reporting and look-through debt. BLA recently admitted that up to 20% of its reported AUM is in the form of undrawn debt facilities, a revelation that has led many analysts to question how faithfully this represents the true financial position of the company. Additionally, BLA recently disclosed a number of loan agreements with their private subsidiaries (i.e. Blue Sky La Trobe Street Fund), with several funds taking intercompany loans from BLA at 10% interest, which flows to reported earnings. Whilst within the bounds of disclosure requirements, opaque information makes it difficult for investors to determine what the risk and return profile of an entity such as BLA (and its funds) may truly be. Figure 2. Example of Blue Sky intercompany lending  Source: BondAdviser, Company Reports So how can investors determine what their risk exposure truly is? Whilst BLA is a unique case, it is important to consider what is really underlying a company before investing, whether that be in equity or credit. The most important factor is understanding the capital structure of the company, including delving into any subsidiaries, and the terms of the debt on issue to these parties. For instance, if a subsidiary owes a debt, is the parent company required to pay up in the event of default? What recourse do creditors have to the parent or controlling entity in the event of default? These are the questions that investors should be considering to truly understand the look-through debt of the company. Searching further abroad, one good example of a company with significant look-through debt is The Coca-Cola Company (NYSE:KO), one of the biggest food and beverage organisations in the world. The Coca-Cola Company, based out of Atlanta, Georgia in the United States, is a complicated conglomerate of companies and brands across the globe, with subsidiaries listed in Japan (2579: Tokyo), Germany (WKN 850663), the U.K. (LON: CCH) and Australia (ASX: CCA). Whilst KO has high levels of disclosure, given the complex nature of the business the question remains: do investors in KO, or its many subsidiaries, understand the risk profile of the company as a whole, and what is their individual exposure? Figure 3. Net Debt Statistics from Coca-Cola and subsidiaries

Source: BondAdviser, Company Reports So how can investors determine what their risk exposure truly is? Whilst BLA is a unique case, it is important to consider what is really underlying a company before investing, whether that be in equity or credit. The most important factor is understanding the capital structure of the company, including delving into any subsidiaries, and the terms of the debt on issue to these parties. For instance, if a subsidiary owes a debt, is the parent company required to pay up in the event of default? What recourse do creditors have to the parent or controlling entity in the event of default? These are the questions that investors should be considering to truly understand the look-through debt of the company. Searching further abroad, one good example of a company with significant look-through debt is The Coca-Cola Company (NYSE:KO), one of the biggest food and beverage organisations in the world. The Coca-Cola Company, based out of Atlanta, Georgia in the United States, is a complicated conglomerate of companies and brands across the globe, with subsidiaries listed in Japan (2579: Tokyo), Germany (WKN 850663), the U.K. (LON: CCH) and Australia (ASX: CCA). Whilst KO has high levels of disclosure, given the complex nature of the business the question remains: do investors in KO, or its many subsidiaries, understand the risk profile of the company as a whole, and what is their individual exposure? Figure 3. Net Debt Statistics from Coca-Cola and subsidiaries  Source: BondAdviser, Company Reports Whilst the above provide just a sample of the many Variable Interest Entities (“VIEs”) that the Coca-Cola Company holds a stake in, there is no doubt that truly understanding the debt structure and risk profile of such a company is very time-consuming and difficult. Buried in the Notes to the KO Financial Statements investors can read that, “creditors of our VIEs do not have recourse against the general credit of the Company, regardless of whether they are accounted for as consolidated entities”. Bingo! So KO don’t act as guarantors for their subsidiaries’ debts, and the parent shareholders are therefore not exposed to this additional risk. Clearly, look-through debt analysis can be a complicated business. Thankfully for the average investor, there are mechanisms in place to reduce the information asymmetry gap between them and the companies in which they want to invest in. A new accounting standard, IFRS 16, aims to effectively eliminate nearly all off balance sheet accounting for lessees, thus making reported information easier to understand and ultimately more comparable across companies. Whilst this may help to resolve the problem of opaque reporting in the form of off balance sheet items, and assist investors looking at companies such as Blue Sky, the Coca-Cola example cited above remains largely unaffected. For these large companies, which have amplified consequences for credit and default risk given the scope and scale of their lending operations, these leases could now be legitimately listed on the subsidiaries’ balance sheets. This means unless you’re trawling through the balance sheets of all of Coca-Cola’s listed VIEs across the world, it remains a difficult proposition to recognise the downstream effect of a company’s intercompany lending.

Source: BondAdviser, Company Reports Whilst the above provide just a sample of the many Variable Interest Entities (“VIEs”) that the Coca-Cola Company holds a stake in, there is no doubt that truly understanding the debt structure and risk profile of such a company is very time-consuming and difficult. Buried in the Notes to the KO Financial Statements investors can read that, “creditors of our VIEs do not have recourse against the general credit of the Company, regardless of whether they are accounted for as consolidated entities”. Bingo! So KO don’t act as guarantors for their subsidiaries’ debts, and the parent shareholders are therefore not exposed to this additional risk. Clearly, look-through debt analysis can be a complicated business. Thankfully for the average investor, there are mechanisms in place to reduce the information asymmetry gap between them and the companies in which they want to invest in. A new accounting standard, IFRS 16, aims to effectively eliminate nearly all off balance sheet accounting for lessees, thus making reported information easier to understand and ultimately more comparable across companies. Whilst this may help to resolve the problem of opaque reporting in the form of off balance sheet items, and assist investors looking at companies such as Blue Sky, the Coca-Cola example cited above remains largely unaffected. For these large companies, which have amplified consequences for credit and default risk given the scope and scale of their lending operations, these leases could now be legitimately listed on the subsidiaries’ balance sheets. This means unless you’re trawling through the balance sheets of all of Coca-Cola’s listed VIEs across the world, it remains a difficult proposition to recognise the downstream effect of a company’s intercompany lending.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Apr 29, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Apr 29, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.