The docile bond market of the past 20+ years is gone. Whilst many professional managers, allocators and advisors have been burned this past year, we expected underperformance but are now in the process of capitalising on higher yields. Whilst risks to rates and credit spreads remain, the possibility of moving up the capital structure (i.e. lower risk) to get a near equivalent income return (i.e. equity to debt, AT1 hybrid to Tier 2 bond, senior to covered) is a clear sign to accumulate in a misunderstood and underappreciated local asset class. Big super and our sovereign wealth funds are quickly increasing their bond allocations, investors should be seriously considering this also.

Hell hath no fury like the bond market scorned

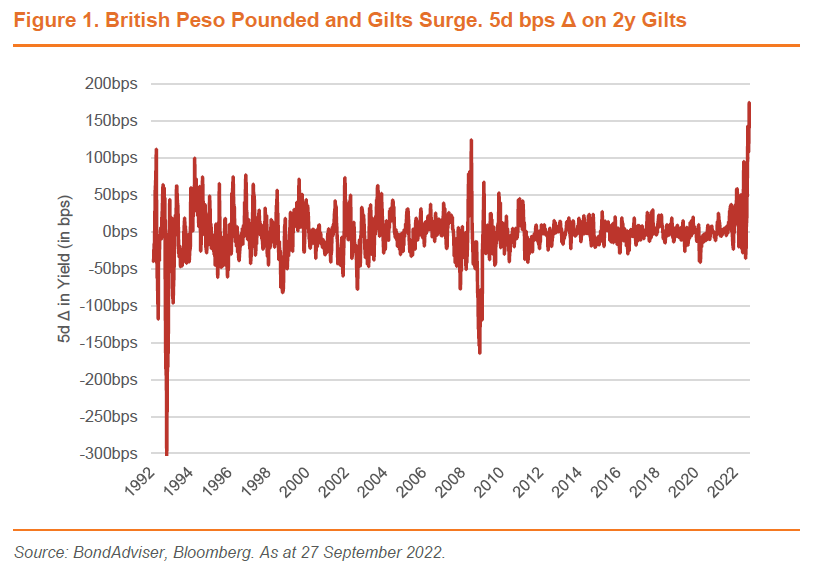

Bond vigilantes have emerged from deep hibernation, forcing British bonds, also known as Gilts, to yield levels not seen since the GFC. The 2-year Gilt has risen +175bps in the past five days (all article data as of 10am 27-September 2022 unless otherwise stated). This is an upwards move without parallel, going back to 1992. The 2-year Gilt now yields 4.5%, at the start of the year this was 0.4%.

Furthermore, the Pound Sterling has dropped to its lowest level on record against the dollar (last: GBPUSD 1.077). These moves have been caused by the dilemma facing policy makers: drive growth through fiscal expansion but risk embedding inflation; or allow growth to nosedive, unemployment to increase and inflation to deflate. The new UK government has revealed an enormous stimulus plan to punt on growth, a noble bet, but foolish through our lens, given the Bank of England expects inflation to continue increasing to 11% in October this year.

These moves, in addition to Fed decisions last week, have seen our local bond yields correspondingly move upwards. As of this morning (27/9/22) our 3mBBSW, 2y and 10y yields are respectively 3.02%, 3.53% and 4.05%.

Credit where its due

The biggest story in credit is currently the buyout and associated financing of Citrix Systems (NASDAQ: CTXS), where banks have lost ~US$600 million in underwriting the deal. The majority of these losses were associated with the US$4 billion secured bond portion of the funding package. The bonds eventually priced at a yield of around 10% and price discount of ~84 cents on the dollar.

When simplified, it is typical in the US leveraged buyout (LBO) market for banks to commit to financing for private equity sponsors in the months before a deal closes. Once finalised, the banks then offload these commitments to the loan and bond market. If pricing moves the wrong way, banks are forced to offer price discounts to entice investors.

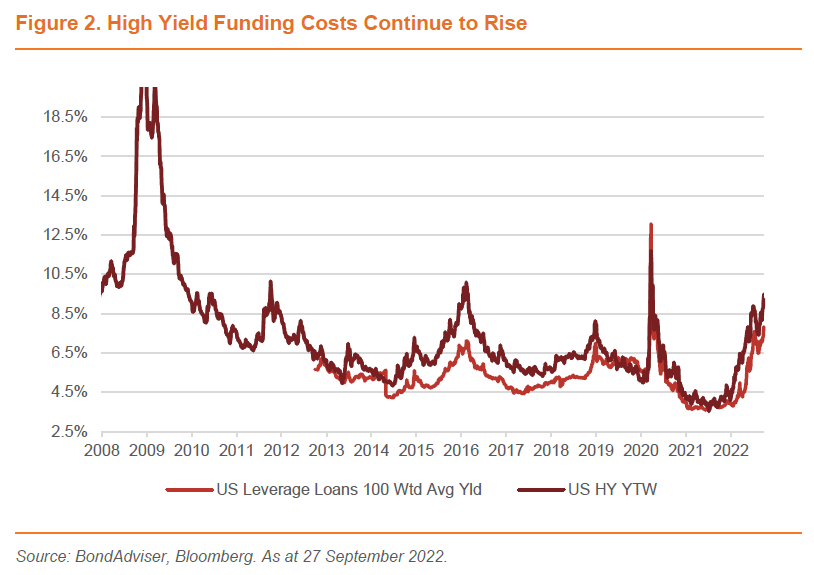

Those with longer memories will recall the big losses banks were forced to take in the GFC under such circumstances. As Figure 2 illustrates, funding costs have not shown any real relief this year in high yield. Further losses on funding deals to banks this year include Intertape and Entegris which collectively totalled $85 million.

The key takeaway is that higher financing costs are placing greater pressure on banks seeking to offload commitments. This casts an ominous shadow on the LBO market and ultimately will drive higher volatility in high yield credit spreads across loans and bonds.

Whilst this is similar in signal to a pure comparison to MXT’s net asset value, it provides a traded market overlay, which we see as useful from an opportunity cost perspective. We note this relationship has turned negative yesterday – indicating relative levels of cheapness (albeit moderate).

Locally, our corporate credit funding costs have returned to 5-year highs. Spreads have moderated, particularly in financials, meaning the driver of higher funding costs have been higher risk-free rates. Such levels now for investors are getting too cheap to ignore, especially relative to an ASX200 dividend yield of 5.08% – effectively the same as the yield on an investment grade bond – but for far less volatility and market risk.

Emphasising this point is Figure 9 (not displayed online – clients only), which is illustrating that compensation for interest rate risk is at levels not seen in the prior 5-years.

Bonds are back. Fear is creating opportunities for the informed, the likes of which has not seen in decades.

Click here to see some of Charlie’s recent video commentary on ausbiz.