The concept of liquidity describes the degree to which an asset or security can be quickly bought or sold in the market without having a material impact on price. Similarly, bond market liquidity refers to the extent to which the bond market allows assets to be bought and sold at stable prices. Cash or cash equivalent securities are the most liquid asset while sub-investment grade fixed income securities are less liquid. Whilst the retail bond market is generally more transparent (ASX is a public market place), the wholesale or institutional bond market (although electronic platforms such as Yield Broker & Bloomberg exist to help facilitate price discovery) is less so. Most secondary bond market transactions (especially when dealing in large volume or in less liquid securities) tend to be transacted via voice or private chat rooms to avoid having a negative price impact in the bond market. Institutional bond market liquidity also varies from security to security for a number of reasons, the main ones being:

- Market breadth. The sheer number and diversity of bonds potentially affects liquidity. The market includes corporates, state government and Australian government bonds to name a few, each with different characteristics and risk factors. Different bonds issued by the same company can also have different characteristics (i.e. senior bonds (more liquid) versus hybrids/junior debt (less liquid)) Assigning value and quickly matching buyers and sellers in a market with so many bonds and so little uniformity is not an easy task.

- Dealer inventory. Since the global financial crisis, many dealers have reduced risk appetite and are not buying or holding as many bonds as in the past. This phenomenon is also due to increased regulatory scrutiny aimed at preventing financial institutions from carrying too much illiquid and/or low grade bonds. This can cause large losses and cause an institution failure during times of financial stress. With fewer buyers and sellers in the market, it may be harder for investors, brokers and authorised dealers to find a buyer willing to purchase a particular security, during periods of market volatility.

- Selling pressure. Any time multiple owners of a security collectively seek to sell at the same time, liquidity may be reduced. Market corrections, domestic or global economic shocks, or sharp movements in could trigger a major demand-supply liquidity imbalance in bond markets.

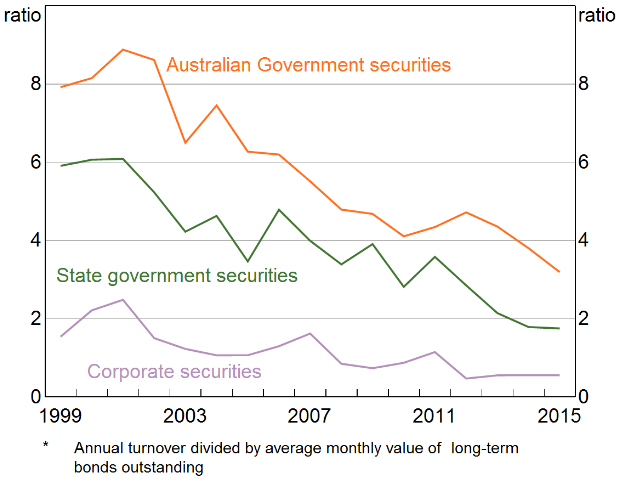

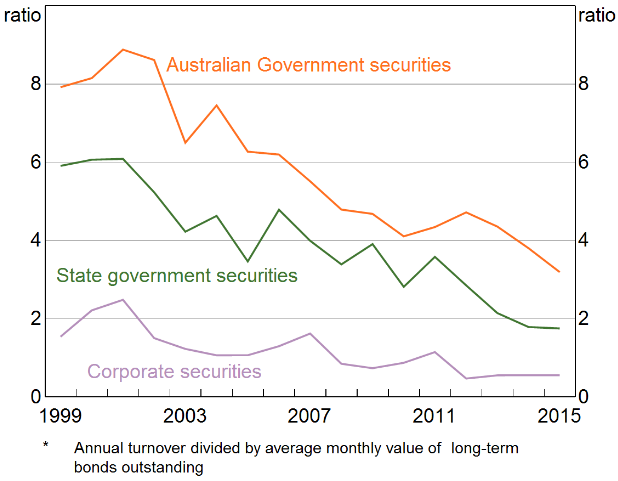

Measuring bond market liquidity is also not an easy exercise in Australia. Most of institutional bond transactions traded in the secondary market are executed over the phone or via chat rooms rather than through an electronic platform, meaning trade data is less readily available. Whilst it would be good to see more trade data on transactions in the market, transparency can make it difficult to move a large parcel. Large parcels can result in bonds’ bid/offer spread widening (reduced liquidity) even if market conditions are benign. Guy Debelle (RBA Assistant Governor – Financial Markets) commented upon the state of “Liquidity in Australian Fixed Income Markets’ on 21 June 2016 in an address to the 4th Australian Regulatory Summit. Assistant Governor Debelle showed that a smaller proportion of bonds are being being transacted relative to the past (Figure 1). Figure 1 – Annual Bond Turnover Ratios*  Source: ABS, AFMA, Austraclear & RBA While Figure 1 shows that the turnover ratio (the ratio of the value of transactions undertaken in bond markets over the course of a year relative to the average outstanding amount of bonds on issue over the year) for AGS bonds has declined over time, supply has grown significantly at the same time. This is due to increased issuance. Overall, this means that the absolute amount of turnover in dollar terms has not changed significantly. Of concern however, is the decline in the turnover of corporate securities over the past 16 years. The banks dominate corporate security issuance. Assistant Governor Debelle also quantified turnover in the following manner:

Source: ABS, AFMA, Austraclear & RBA While Figure 1 shows that the turnover ratio (the ratio of the value of transactions undertaken in bond markets over the course of a year relative to the average outstanding amount of bonds on issue over the year) for AGS bonds has declined over time, supply has grown significantly at the same time. This is due to increased issuance. Overall, this means that the absolute amount of turnover in dollar terms has not changed significantly. Of concern however, is the decline in the turnover of corporate securities over the past 16 years. The banks dominate corporate security issuance. Assistant Governor Debelle also quantified turnover in the following manner:

- “the share of the government bond market that used to turnover in an average month now takes a bit over six weeks”

- “the average share of the corporate securities market that used to turnover in one month now takes closer to two months”

- “We also hear from market participants that it is, in general, a bit more difficult to transact in size.”

That being said, Australia has been fortunate that the withdrawal of dealers from the local bond market has not had as sizeable an impact as seen elsewhere. Whilst regulatory change has contributed to the reduced capacity in the local market (e.g. some overseas investment banks operating within Australia no longer hold as much corporate bond inventory as they did prior to the GFC), it has so far not been to the detriment of overall market functionality. The decline in the presence of foreign banks reflects both a change of business strategy and also a response to regulations. Certain foreign banks are now subject to increased capital requirements and the leverage ratio in their home markets which has led to a lower level (or greater rationing) of principal-based market-making. This is a direct result of decreased appetite for warehouse risk particularly for securities that are not very liquid. Another reason why Australian fixed income markets continue to function smoothly is that the derivative market have been operating effectively. Figure 2 shows that market depth (the size of a trade that can be executed for a given trade size) in the Australian government 10 year futures market. It appears to be at a similar prevailing level to that prior to the Global Financial Crisis. Figure 2 – Market Depth*  Source: AFMA, ASX & the RBA The Australian bond market continues to be supported by market makers. According to AFMA data and pointed out Governor Debelle, banks account for around 45% of all trades in Australian Government Securities (AGS) market, compared to ~60% in the decade to 2011. At 45%, banks account for a slightly larger share of transactions in the semi government bond market than they did in the past whilst their share of transactions in non-government bond markets has declined slightly from 50% to 45%. This is reflective in the bank bond inventories. Banks have switched non-government bond holdings for government bond holdings. This is partly driven by a decrease in willingness to warehouse bonds that do not satisfy liquidity requirements in the secondary market. It also relates to the incentive for banks to hold more liquid securities to satisfy their Liquidity Coverage Ratio (LCR). Bank holdings of government bonds have increased to around 30% of the market. The RBA has assessed this and have suggested holding greater than 30% may impair the functioning of the government bond markets. However, another consideration is the sizeable share of government securities held by offshore investors. In total, this currently amounts to more than 60% of the stock. Many of these investors are buy-and-hold investors and generally do not undertake in securities lending. As a result, these holding offer limited market liquidity. The RBA have maintained the assumption that the domestic banks can reasonably hold 25% of the stock of AGS and semis in 2017 without damaging market liquidity. Foreign banks operating in the local market hold around another 5% of the stock to meet their LCR requirement. This implies that in total this remains at 30%. Based on budget projections of the Commonwealth and State governments the RBA expect the domestic banks could reasonably hold $220 billion without impairing the market, an increase of $25 billion compared to the holdings in 2016. We expect, this will be closely monitored by the Council of Financial Regulators (i.e. APRA, ASIC, the RBA and the Treasury). Conclusions: While the Australian fixed income market has continued to function satisfactorily whilst some overseas markets have experienced increased concerns over their capacity to function effectively, there is no room for complacency. Turnover in both Australian government and state government related bonds remains respectable due to their high quality nature, i.e. rated in the AAA or AA+ category and are held as unencumbered high quality liquid assets (HQLA) for LCR purposes by financial institutions. However, turnover in Australian corporate bonds (comprising mainly of bank and insurance company issued securities) has also declined. Any shocks to the global financial system (such as the GFC) that leads to lower turnover and therefore higher secondary market trading margins of bank related bonds would also be reflected in primary issuance margins.

Source: AFMA, ASX & the RBA The Australian bond market continues to be supported by market makers. According to AFMA data and pointed out Governor Debelle, banks account for around 45% of all trades in Australian Government Securities (AGS) market, compared to ~60% in the decade to 2011. At 45%, banks account for a slightly larger share of transactions in the semi government bond market than they did in the past whilst their share of transactions in non-government bond markets has declined slightly from 50% to 45%. This is reflective in the bank bond inventories. Banks have switched non-government bond holdings for government bond holdings. This is partly driven by a decrease in willingness to warehouse bonds that do not satisfy liquidity requirements in the secondary market. It also relates to the incentive for banks to hold more liquid securities to satisfy their Liquidity Coverage Ratio (LCR). Bank holdings of government bonds have increased to around 30% of the market. The RBA has assessed this and have suggested holding greater than 30% may impair the functioning of the government bond markets. However, another consideration is the sizeable share of government securities held by offshore investors. In total, this currently amounts to more than 60% of the stock. Many of these investors are buy-and-hold investors and generally do not undertake in securities lending. As a result, these holding offer limited market liquidity. The RBA have maintained the assumption that the domestic banks can reasonably hold 25% of the stock of AGS and semis in 2017 without damaging market liquidity. Foreign banks operating in the local market hold around another 5% of the stock to meet their LCR requirement. This implies that in total this remains at 30%. Based on budget projections of the Commonwealth and State governments the RBA expect the domestic banks could reasonably hold $220 billion without impairing the market, an increase of $25 billion compared to the holdings in 2016. We expect, this will be closely monitored by the Council of Financial Regulators (i.e. APRA, ASIC, the RBA and the Treasury). Conclusions: While the Australian fixed income market has continued to function satisfactorily whilst some overseas markets have experienced increased concerns over their capacity to function effectively, there is no room for complacency. Turnover in both Australian government and state government related bonds remains respectable due to their high quality nature, i.e. rated in the AAA or AA+ category and are held as unencumbered high quality liquid assets (HQLA) for LCR purposes by financial institutions. However, turnover in Australian corporate bonds (comprising mainly of bank and insurance company issued securities) has also declined. Any shocks to the global financial system (such as the GFC) that leads to lower turnover and therefore higher secondary market trading margins of bank related bonds would also be reflected in primary issuance margins.