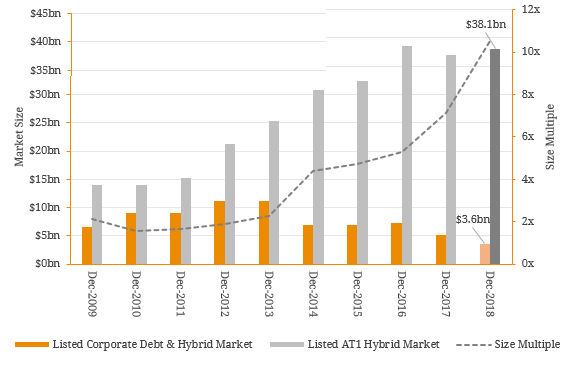

For the past few years, ASX-listed corporate debt and hybrid securities have dwindled leaving investors with a shrinking opportunity set to diversify outside the AT1 capital instrument market. This reduction in supply began with the Origin and Woolworths Subordinated Notes (ASX: ORGHA, WOWHC) being called at the end of 2016. This was followed by Caltex, Goodman and Tabcorp redeeming their respective listed hybrid securities in 2017 without a reinvestment option. Last week, APA Group (ASX: APA) released its interim results (1H18) and revealed it would be opting to redeem its listed subordinated notes (ASX: AQHHA) at the first optional call date (31 March 2018). Management stated this redemption would be funded by a new equity placement to ensure the equity credit component of the notes (~50%) did not affect the group’s credit rating. Consequently, AQHHA holders were not offered a reinvestment offer leaving effectively $515 million of funds uninvested by the end of March. The Crown Subordinated Notes (ASX: CWNHA) are next on the maturity schedule (September 2018) in which 25% has already been bought back by the group on market. Given the significant capacity in Crown’s balance sheet following a number of divestments and subsequent debt reduction, it is likely the remaining notes will redeemed for cash or refinanced at a lower cost of debt into the unlisted market. If Crown proceeds with this action, the listed corporate debt and income market is expected to shrink to ~$3.6 billion by the end of 2018 (Figure 1). To put this in perspective, this is ~10.5 times smaller than the listed AT1 hybrid market making sectoral diversification challenging. Figure 1. Listed Debt & Hybrid Market (Corporate v AT1 Instruments)  Source: BondAdviser Despite this significant reduction in the listed corporate market, it is interesting to see that hybrids are still being considered as a funding option for some ASX200 companies. This was evident in last month’s reporting season where Seven Group announced a new 7-year convertible bond to refinance the debt facilities of its recent full acquisition of Coates Hire. While there is a fairly deep appetite for these instruments, particularly in the US, we note that this specific type of structure is rare in the Australian fixed income market. Since the Global Financial Crisis (GFC), only a handful of corporate convertible notes have existed, issued by the likes of the Australian Foundation Investment Company, Beach Energy, Cromwell Property Group (€ denominated) and Peet Limited. Seven Group has always been relatively esoteric in its funding approach. The Seven TELSY4 (ASX: SVWPA) have been a pillar to the group’s capital structure for over a decade as Seven’s underlying business model has morphed from a pure-play media company into a conglomerate with investments across a number of industrial sectors. Although Seven’s new hybrid instrument is unlisted and restricted to wholesale investors, hybrid capital is still a viable option for corporate treasurers. As a result, this convertible bond transaction may pave the way for more corporate hybrids but unfortunately these instruments may be again targeted to offshore and/or wholesale investors. Overall, the sharp decline of listed corporate issuance is a feature of Australian debt markets. The corporate loan market remains the dominant debt funding source for Australian companies (~41%). However, our analysis illustrates that international debt markets, in particular the US Private Placement Market (USPP), are growing in popularity (~51%). Consequently, domestic debt securities comprise just ~7% of all ASX200 corporate debts which highlights the corporate credit reality facing the Australian fixed income market, especially retail investors (~0.6%). On this basis, listed corporate issuance is not a priority choice for many ASX200 corporates. Figure 2. ASX200 Corporate Debt Waterfall*

Source: BondAdviser Despite this significant reduction in the listed corporate market, it is interesting to see that hybrids are still being considered as a funding option for some ASX200 companies. This was evident in last month’s reporting season where Seven Group announced a new 7-year convertible bond to refinance the debt facilities of its recent full acquisition of Coates Hire. While there is a fairly deep appetite for these instruments, particularly in the US, we note that this specific type of structure is rare in the Australian fixed income market. Since the Global Financial Crisis (GFC), only a handful of corporate convertible notes have existed, issued by the likes of the Australian Foundation Investment Company, Beach Energy, Cromwell Property Group (€ denominated) and Peet Limited. Seven Group has always been relatively esoteric in its funding approach. The Seven TELSY4 (ASX: SVWPA) have been a pillar to the group’s capital structure for over a decade as Seven’s underlying business model has morphed from a pure-play media company into a conglomerate with investments across a number of industrial sectors. Although Seven’s new hybrid instrument is unlisted and restricted to wholesale investors, hybrid capital is still a viable option for corporate treasurers. As a result, this convertible bond transaction may pave the way for more corporate hybrids but unfortunately these instruments may be again targeted to offshore and/or wholesale investors. Overall, the sharp decline of listed corporate issuance is a feature of Australian debt markets. The corporate loan market remains the dominant debt funding source for Australian companies (~41%). However, our analysis illustrates that international debt markets, in particular the US Private Placement Market (USPP), are growing in popularity (~51%). Consequently, domestic debt securities comprise just ~7% of all ASX200 corporate debts which highlights the corporate credit reality facing the Australian fixed income market, especially retail investors (~0.6%). On this basis, listed corporate issuance is not a priority choice for many ASX200 corporates. Figure 2. ASX200 Corporate Debt Waterfall*  *Prference Shares Excluded From Analysis Source: BondAdviser As we have stated in the past, the Corporate segment of ASX-Listed Debt & Hybrid Market continues to face an uphill battle. Structural, fundamental and technical factors all continue to impede corporate issuers from coming to the listed debt market for funding. It is difficult to see this changing anytime soon without a massive overhaul of the retail fixed income market and for this reason, investors may have to look at alternative options to diversify their portfolios away from the bank-dominated investment universe. This is being partially solved by the introduction of fixed income exchange traded products such as the recent suite of new income exchange-traded funds (ETFs) and notable success of the MCP Master Income Trust (ASX: MXT). However, more alternatives are required to help investors diversify risk.

*Prference Shares Excluded From Analysis Source: BondAdviser As we have stated in the past, the Corporate segment of ASX-Listed Debt & Hybrid Market continues to face an uphill battle. Structural, fundamental and technical factors all continue to impede corporate issuers from coming to the listed debt market for funding. It is difficult to see this changing anytime soon without a massive overhaul of the retail fixed income market and for this reason, investors may have to look at alternative options to diversify their portfolios away from the bank-dominated investment universe. This is being partially solved by the introduction of fixed income exchange traded products such as the recent suite of new income exchange-traded funds (ETFs) and notable success of the MCP Master Income Trust (ASX: MXT). However, more alternatives are required to help investors diversify risk.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.