Last Friday the latest European bank stress test results were released. The test covered 51 European banks from 15 European Union (EU) and European Economic Area (EEA) countries and were designed to highlight potential capital shortfalls under both mild and severely stressed economic conditions. The macroeconomic scenarios assumed were that the EU real GDP growth rates over the three years of the exercise were ‐1.2%, ‐1.3% and 0.7% respectively (a deviation of 7.1% from its baseline level in 2018) and EEA economic contraction of between 1.0% – 1.3% in 2016-17. The objective of the stress test is to provide supervisors, banks and other market participants with a common analytical framework to consistently compare and assess the resilience of large EU banks to adverse economic developments. The results of these tests also assist the European Central Bank (ECB) in setting bank-specific minimum capital requirements, including Pillar 2 Guidance. From a starting point of an average Transitional Common Equity Tier 1 (CET1) ratio of 13.2%, the stress test recorded a fall in the average Transitional CET1 ratio of 3.80%, highlighting a fair degree of resilience and assuring most European banks’ ability to issue and service additional Tier 1 (AT1) hybrid capital. Only one bank’s capital ratio consistently fell below the 5.5% CET1 minimum threshold, although a number of banks showed more signs of stress as the scenarios were stretched out to 2018.  Source: 2016 EU-Wide Stress Test Results The Italian bank Banca Monti dei Paschi (the world’s oldest bank still in existence) was the only bank to fall below 5.5% CET1 threshold on a consistent basis, with shareholders capital being wiped out according to the results. These tests were more severe than the last ones conducted (2014) due to the better starting point (higher CET1 levels) of the banks. Only two banks saw their CET1 ratio fall below 7%, which will be the new minimum CET1 level under Pillar 1 at the end of 2019. Around 14 of the tested banks saw an adverse (>5%) CET1 impact, with the main driver in these instances being related to credit and market risk (credit risk-related loses of €349bn accounted for the vast majority of simulated losses under the adverse scenario). The tests highlighted several banking systems as being significantly weaker than others, these including Austria, Ireland and Italy. The key stress point for the former being cross-border sensitivities, while for the latter two it was domestic market weaknesses. The strongest banks were the Scandinavian banks. Both S&P and Moody’s stated the test results were broadly in line with their own current assessments. The Australian Prudential Regulation Authority (APRA) also conduct regular stress tests upon the Australian banking system with the 13 largest ADI’s being tested against two scenarios involving a significant housing market downturn in 2014 although individual bank results were not published. The aggregated losses resulting under APRA’s 2014 stress scenarios produced a material decline in the capital ratio of the Australian banking system with the key outcomes being:

Source: 2016 EU-Wide Stress Test Results The Italian bank Banca Monti dei Paschi (the world’s oldest bank still in existence) was the only bank to fall below 5.5% CET1 threshold on a consistent basis, with shareholders capital being wiped out according to the results. These tests were more severe than the last ones conducted (2014) due to the better starting point (higher CET1 levels) of the banks. Only two banks saw their CET1 ratio fall below 7%, which will be the new minimum CET1 level under Pillar 1 at the end of 2019. Around 14 of the tested banks saw an adverse (>5%) CET1 impact, with the main driver in these instances being related to credit and market risk (credit risk-related loses of €349bn accounted for the vast majority of simulated losses under the adverse scenario). The tests highlighted several banking systems as being significantly weaker than others, these including Austria, Ireland and Italy. The key stress point for the former being cross-border sensitivities, while for the latter two it was domestic market weaknesses. The strongest banks were the Scandinavian banks. Both S&P and Moody’s stated the test results were broadly in line with their own current assessments. The Australian Prudential Regulation Authority (APRA) also conduct regular stress tests upon the Australian banking system with the 13 largest ADI’s being tested against two scenarios involving a significant housing market downturn in 2014 although individual bank results were not published. The aggregated losses resulting under APRA’s 2014 stress scenarios produced a material decline in the capital ratio of the Australian banking system with the key outcomes being:

- Starting the scenario at 8.9%, the aggregate CET1 ratio of the participant banks fell under Scenario A to a trough of 5.8% in the 2nd year of the crisis (that is, there was a decline of 3.1%), before slowly recovering after the peak of the losses had passed.

- From the same starting point, under Scenario B the trough was 6.3%, and experienced in the 3rd year.

- The ratios for Tier 1 and Total Capital followed a similar pattern as CET1 under both scenarios.

- At an individual bank level there was a degree of variation in the peak-to-trough fall in capital ratios, but importantly all remained above the minimum CET1 capital requirement of 4.5%.

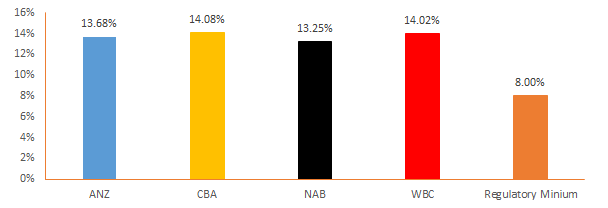

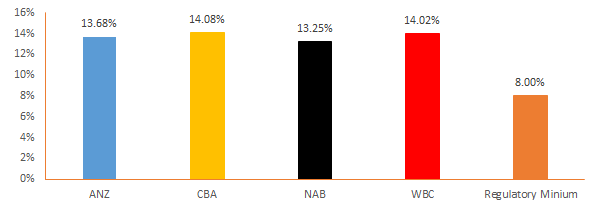

It is also important to remember that the four major Australian banks during 2015 have collectively raised over A$20 billion in additional CET1 capital during 2015 and consequently hold a level of capital that is in excess of the 8% regulatory minimum as shown in the Chart 1. Chart 1. Major Australian bank total capital ratio versus the Regulatory Minimum  Source: Bank Pillar III Reports (March 2016) APRA are currently conducting stress testing of credit unions, building societies and mutual banks.

Source: Bank Pillar III Reports (March 2016) APRA are currently conducting stress testing of credit unions, building societies and mutual banks.