Equity markets remained turbulent last week with ASX200 trading in a 200 point range (5073 – 4873) while the flight to quality saw the Bloomberg AUSBond Composite Index up 0.34%. Year to date the bond index has outperformed equtiies by 7.6% even as credit has deteriorted. This is almost exclusively because the risk free yield curve (government bonds) has flattened significantly (we note the front end of the curve has become inverted again). This is a result of mounting expectation that the RBA will be forced into cutting rates due to the deterioating economic outlook of the global economy. While this may prove to be true it does not align with the RBA’s economic forecasts as outlined in Fridays monetary policy statement. Its unemployment forecast was cut and maintained an expectation for accelerating growth as services drive job creation. The interest rate market is less optimistic than the RBA and is pricing in an 80% probability that the central bank will cut its benchmark interes rate of 2% within the next six months. Our opinion on rates remains unchanged and we expect the RBA will remain on hold in 2016 subject to inflation remaining broadly stable. The performance of markets have become dependent on central bank easing policies worldwide. Expanding balance sheets of central banks cannot go on forever and at some point markets will force a change in policy which could result in violent market reactions. The RBA is in a very good position relative to its counterparts and to date they have remained relatively conservative in easing policy even though markets have been trying to force them lower. Since the start of January 2015 the 3-Year Government Bond yield has been under 2% on more than 66% of days. On Friday, the US market was weaker following employment data which was below expectations. The US non-farm payrolls report showed an increase of 151 thousand jobs in January but a negative adjustment of 10 thousand jobs to the previous two months. This had the effect of lowering the three-month moving average from a very strong 279 thousand to 231 thousand. This simply added to market fears and US interest rate futures are now only pricing about a 50% probability of a rate increase this year. Reporting Season Reporting season started last week with mixed results Genworth Mortgage Insurance Australia Limited (GMIAL) reported on Friday with result broadly in line with expectations.After the Australian share market closed on Friday, Genworth Financial Inc (the majority shareholder) said that it could pursue more divestures to help pay down more than US$500 million in debt maturing in 2018. The limited ability of GFI to refinance maturing debt following recent credit market turmoil has increased the probability of further divesture of GMIAL. This would be a credit positive for GMIAL as the influence of the lower credit rated GMI would be reduced. For the full report click here. The Tabcorp earnings result wasn’t brilliant on a statutory basis due to one off costs but their balance sheet is in good shape. There is more than sufficient liquidity to meet its obligations and in our opinion the primary risk in 2016 is even risk (possible Tatts merger). Macquarie’s update was also below expectations with weakness in the Commodities and Financial markets division. The outlook was also neutral against fairly high expectations and therefore the stock price experienced a correction. From a credit perspective nothing much has changed. However, more clarity is needed on the balance sheet. Ansell is not a name we cover but its results highlighted the impact of currency and oil price volatility. They reported a decline of 21% in comparable first half earnings but maintained it’s dividend at US20 cents. The company cited the more challenging global economic environment where the demand for medical brands was softer in emerging markets such as Russia & Brazil. The Commonwealth Bank of Australia is the first of the major banks to report first-half results on Wednesday. Equity analysts will be closely examining how the banks have fared in maintaining margins following last year’s equity capital raisings and, more importantly, the outlook for dividends going forward. From a hybrid investor’s point of view, the CBA is expected to also announce the redemption and replacement of the PERLs III hybrid before deciding whether the size & pricing of a new issuance will have an impact on secondary market trading. 10/02/2016 – AGL (1H16) 10/02/2016 – Commonwealth Bank (1H16) 11/02/2016 – Goodman Group (1H16) 11/02/2016 – Mirvac (1H16) 11/02/2016 – Suncorp (1H16) 11/02/2016 – Transurban (1H16)

Click below for Interactive Charts

Chart 1: Bloomberg AUSBond Composite Index (Monthly)

Chart 2: Bonds vs Equities 2014/15 (Monthly)

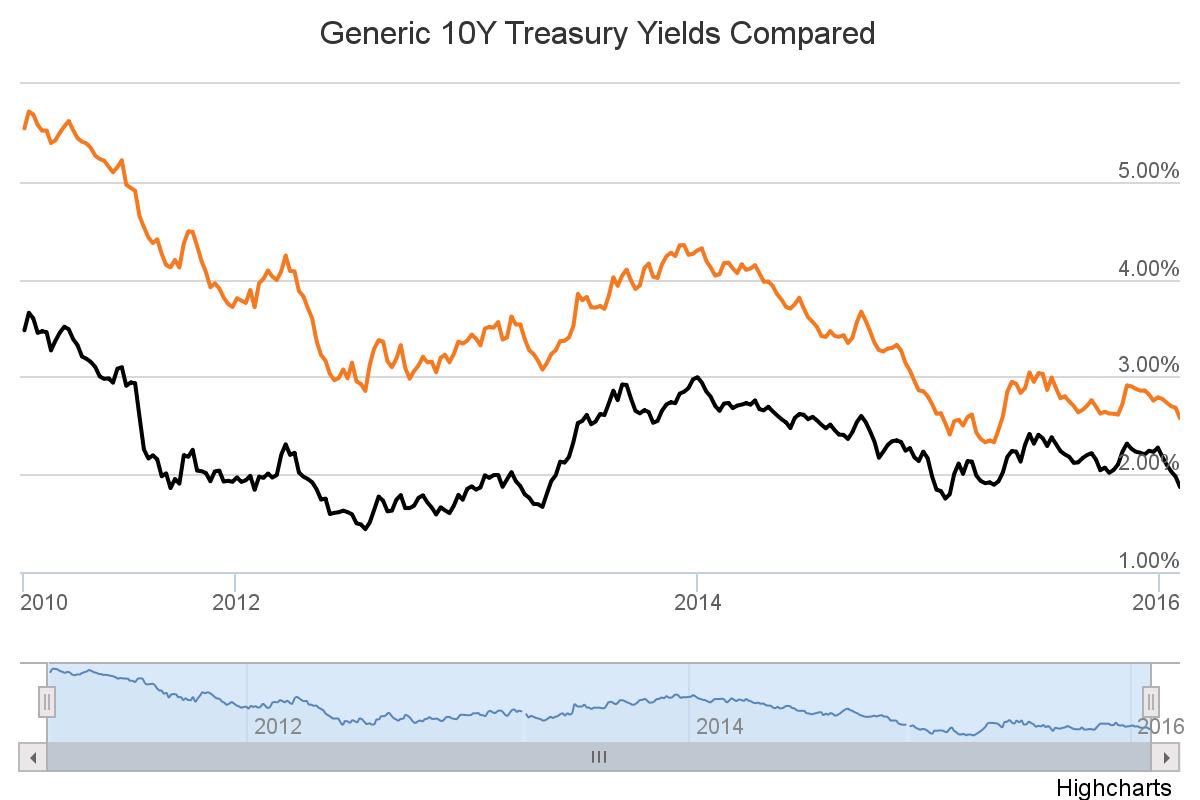

Interest Rates Interest rate expectations remain in a state of flux as futures markets and central banks are opposed to each others views. Conventionary monetary policy would suggest the market is being overly punitive but there is nothing conventional about modern monetary policy. Last week the RBA maintained the cash rate target at 2.0% but kept the door open to cuts based on the trajectory of inflation data. The monetary policy statement gave us insight into all input assumptions for 2016 but these are the ones of note. GDP growth expectatation are braodly unchanged changed from the November Statement. GDP growth is forecast to be 2.5 – 3.5% over the year to December 2016, and to increase to 3 – 4 % over the year to June 2018. Wage growth has been broadly in line with expectations and is not expected to increase much over the next couple of years, given continued spare capacity in the labour market. In terms of inflation there are very few signs of improvement. The prices of nontradable items is forecast to pick up gradually but will remain below its target in 2016. The prices of tradable items are expected to rise over the next few years, as the lower AUD leads to increases in import prices, which are expected to be gradually passed on to the prices paid by consumers.  In February 2015, the 10-year bond yield hit an all-time low of 2.27% before lifting to highs near 3.15% on 11 June 2015. In early November 2015 there was a progressive increase in yield from ~2.60% to a high of 2.99%. However, since mid December the flight to quality has meant the 10-year yield has given back the changes in Q4 2015 and last week hit a 6 month low of 2.52% (current 2.58%). The 3-year bond has followed a similar pattern and broke out of its recent yield range (1.90 – 2.1%) in November/December 2015 reaching a high of 2.18% on 7 December 2015 but is now back to 1.85%. On 5 February 2016, the ASX 30 Day Interbank Cash Rate Futures March 2016 contract was trading at 98.045 indicating a 19% expectation of an interest rate decrease to 1.75% at the next RBA Board meeting (up from 6% the previous week).

In February 2015, the 10-year bond yield hit an all-time low of 2.27% before lifting to highs near 3.15% on 11 June 2015. In early November 2015 there was a progressive increase in yield from ~2.60% to a high of 2.99%. However, since mid December the flight to quality has meant the 10-year yield has given back the changes in Q4 2015 and last week hit a 6 month low of 2.52% (current 2.58%). The 3-year bond has followed a similar pattern and broke out of its recent yield range (1.90 – 2.1%) in November/December 2015 reaching a high of 2.18% on 7 December 2015 but is now back to 1.85%. On 5 February 2016, the ASX 30 Day Interbank Cash Rate Futures March 2016 contract was trading at 98.045 indicating a 19% expectation of an interest rate decrease to 1.75% at the next RBA Board meeting (up from 6% the previous week).