As we move into the new month, demand for corporate bonds remains strong. The balance has been skewed for most of 2017, with bonds being easy to sell but difficult to buy. But as primary supply has increased (mostly in institutional markets), this skew has eased slightly. This suggests that credit spreads are likely to trade in a tight range over the next quarter, subject to no material event causing a correction in the broader market. Year to date (YTD) returns have been broadly in-line with expectations, with those willing to take a balanced approach to credit risk and duration benefiting most. Australian markets continue to follow offshore leads with transparency on US policies and reforms being the key driver of market sentiment.

| YTD Return | |

| RBA Cash Rate Index | 0.48% |

| Bloomberg Ausbond Composite Index | 1.99% |

| Bloomberg Ausbond Credit Index | 2.33% |

| Bank Hybrid (Tier 1) Basket | 2.04% |

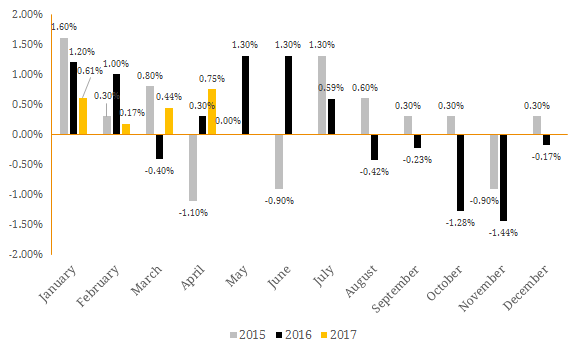

Chart 1: Bloomberg AUSBond Composite Index (Monthly) Chart 2: Bonds vs Equities 2016/2017 (Monthly) Chart 3: Term Deposit Review – March

Corporate News In corporate news, last week we had trading updates from Wesfarmers, Stockland, Mirvac and GPT which were all in line with expectations (Wesfarmers emerging as the pick of the bunch) and credit neutral. This week, we have Woolworths quarterly sales update (Tuesday) and Genworth quarterly update (Wednesday). It is important to note that these updates are generally more meaningful for higher beta names (i.e. Qantas, Crown and Genworth). Meanwhile, the battle for Tatts Group Limited continued last week, with the group announcing that the Pacific Consortium bid was not superior to the proposed merger with Tabcorp. Tatts confirmed that that the merger remained in the best interest of shareholders. Either way, holders of Tatts Bonds (ASX Code: TTSHA) have the right to enforce redemption in a change of control or delisting event.

High Yield In high yield news, NEXTDC announced a potential new $200 million senior unsecured fixed rate bond offering. The new note proceeds will be used to redeem Notes I ($60 million) and Notes II ($100 million) at the next optional call date (16 June 2017). The issuer has appointed NAB as arranger and lead manager on the new deal.

Bank Reporting Season Over the coming weeks, three of the big major banks will present interim results. Interim results for ANZ (Tuesday), NAB (Thursday) and Macquarie (Friday) will be released this week while the Westpac Interim Results and CBA Quarterly Update will be announced next week. APRA Banking Statistics released last week confirm that credit growth is softening and below both APRA’s and S&P’s speed limits. However, earnings are widely expected to improve primarily as a result of recent increases in interest rates for investor and interest-only home loans. Margins, capital requirements and bad debts will be the key themes. From a credit perspective, the highlight will be the banks’ response to recent comments by APRA Chairman stating “at a more strategic level, we intend to review capital requirements for mortgage lending as part of our work on establishing ‘unquestionably strong’ capital standards as recommended by the Financial System Inquiry”. If risk weights on mortgages increase to ~30%, we are likely to see further increases in common equity capital which provides support to senior debt but more specifically to capital instrument holders (Tier 1 and 2).

The Budget Next week, the Treasury is expected to announce the 2016-17 Federal Budget deficit of over $38.3 billion, $1.8 billion worse than the Government’s mid-year forecast. From a credit perspective, poor wage and job growth is likely to impact the top line. Importantly, we will monitor the reaction of the rating agencies partcularly whether this is a sufficient catalyst for downgrade of the sovereign credit rating.