Equity markets continued their poor start to 2016 last week with the ASX 200 dropping a further 98 points (1.96%) led once again by BHP (down 7.8%). Domestic bond markets fared much better in the flight to quality as benchmark government bond yields entered their second straight weekly drop. The global sell-off in stocks and commodities extended with WTI crude oil falling more than 9% to reach the lowest point since 2003 – the key driver was that sanctions were lifted on Iranian oil exports. From a timing perspective this couldn’t be worse as global over supply increaseses further. Although Oil is the stand out underperformer, all commodities are under pressure with Bloomberg reporting that investment managers have increased their short positions across 18 raw materials (doubling the negative bets in just two weeks). Return on the commodity basket last week slid to its lowest level in 25 years with market turmoil in China (the world largest consumer of commodities) meaning the marginal buyer no longer exists across mutliple commodities.

This is of significant interest to bond/hybrid markets where Standard and Poors (S&P) further revised its assumptions for Brent crude to $US40 a barrel (from $US55) in 2016, $US45 (from $US67) in 2017 and $US50 (from US$70) thereafter. This will put significant pressure on the corporate ratings of domestic oil producers such as Santos, Woodside and Origin Energy despite significant capital raisings in 2H2016. While we accept these price assumptions from S&P are supposed to look through the cycle, the spot and forward prices are well below these assumptions and at the moment the agencies are chasing their tails to keep up. In the US, corporate defaults in the energy space are on the increase and the upcoming bank reporting season will be crucial to see what sort of provisions are being taken. Some small lenders in the U.S. (i.e BOK Financial) have already disclosed major loan impairments and it’s almost impossible to see how oil producers wont have major drops in free-cash-flow which is likley to trigger bank covenants. In our opinion there will be significant restructuring required in the Oil & Gas sector in 2016, some by choice and some forced by lenders.

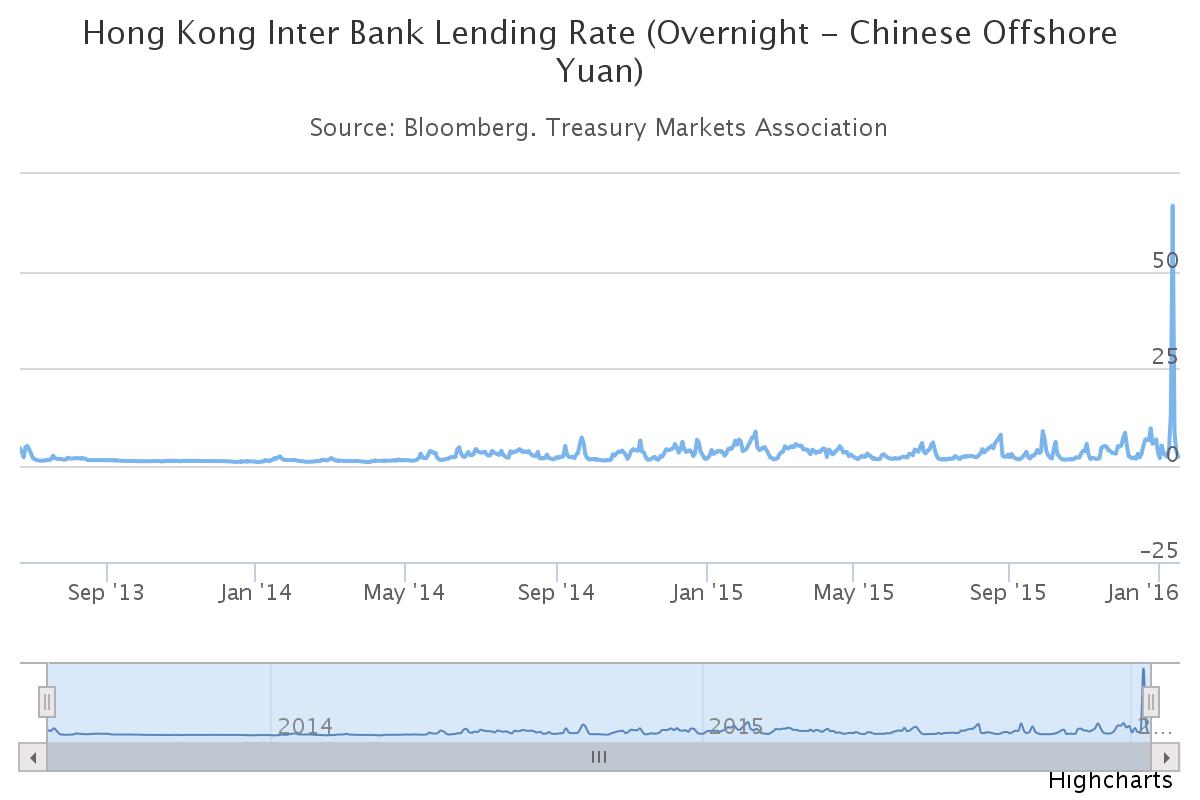

Another concern last week was the spike in the overnight CNH-Hong Kong Interbank Offer Rate (Hibor). This lending rate is similar to Libor in the US and BBSW in Australia and is a daily benchmark for offshore renminbi interbank lending. On Tuesday last week this rate hit a record high of 66.81% (according to Bloomberg) up from only 4% the Friday before. This is the highest level since the benchmark was launched in 2013. While this is obviously not a positive for the market it is a reflection of money imbalance for the dual currency system (CNH (offshore) and CNY (Onshore). However, unlike Libor which is a crucial benchmark for loans that global banks rely on, most Chinese Banks don’t depend on CNH-Hibor-linked loans.

Reporting season is now in full swing in the US with the average results coming out of the banking system giving us an indication of what is to come this reporting season. We remain confident in our recommendations in the lead up to the February reporting season but are cautious of underwhelming results.

Interactive Charts Below

Interactive Charts Below

Click below for Interactive Charts

Chart 1: Bloomberg AUSBond Composite Index (Monthly)

Chart 2: Bonds vs Equities 2014/15 (Monthly)

Interest Rates

In economic news the standout release over the past week was the December 2015 employment numbers. The employment figures beat expectations again recording loss of 1k jobs vs an expectation a loss of 10K jobs. We expected a downward revision to the November figures but were pleasantly surprised to see a revision up from 71.4k to 74.9k. Also pleasing were full time jobs increasing by 17,600 and part time jobs reducing by 18,500. This means the thesis of full time job increases across the eastern seabord continues to increase while the participation rate remains stable. We feel the RBA is gaining confidence the economy is transitioning away from mining and provided growth in employment is maintained, the probability of further rate cuts is low (even if inflation is below target). The only downside risk to this thesis are further shocks in financial markets requiring the RBA to intervene.

In February, the 10-year bond yield hit an all-time low of 2.27% before lifting to highs near 3.15% on June 11. In early November 2015 there was a progressive increase in yield from ~2.60% to a high of 2.99%. However, since mid December the flight to quality has meant the 10Y yield has dropped to 2.64%. The 3-year bond has followed a similar pattern and broke out of its recent yield range (1.90 – 2.1%) in November/December 2015 reaching a high of 2.18% on 7 December 2015 but has since collapsed back to 1.85%. On 15 January 2016, the ASX 30 Day Interbank Cash Rate Futures February 2016 contract was trading at 98.035 indicating a 15% expectation of an interest rate decrease to 1.75% at the next RBA Board meeting (broadly unchanged on the week).

Interactive Charts Below

Interactive Charts Below