Over the past couple of years there has been increased focus on high yield securities as government bonds have fallen to all time lows. A portfolio of high yielding securities therefore requires an understanding of the different types of securities available. Investors have definitely moved up the risk spectrum into high yield bonds and/or hybrids. While we are not suggesting this is a foolproof income strategy our clients are increasingly asking us which option is better, a high yield bond or a high yield hybrid security? So what is the difference? If on one hand (hypothetically) Bank A Capital Security offers ~7% yield and on the other Corporate B offers 7% yield ……which one is the best?

| Last Price | Capital Price | Running Yield | Yield to Maturity | Expected Maturity Date | |

| Bank A Capital Security (Bank Hybrid) | 103.001 | 100.552 | 7.41% | 6.96% | 13 December 2017 |

| Corporate B Security (High Yield) | 103.281 | 101.95 | 7.50% | 6.98% | 7 August 2019 |

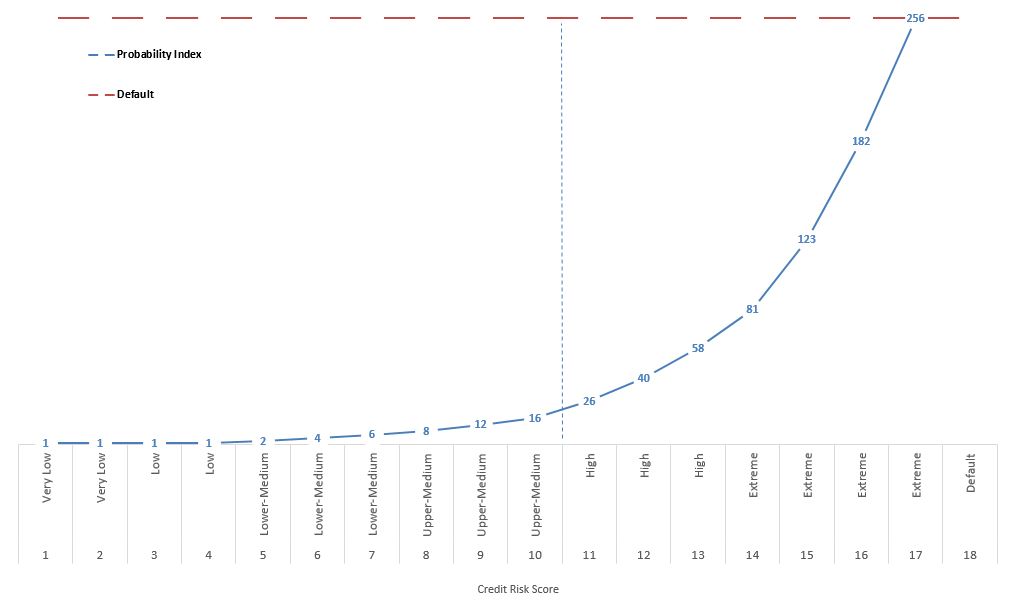

The first thing to check is if the security yield being offered is a running yield or a yield to maturity. The running yield will give you an estimate on the income of the security (it could change if the security is floating rate) but you could be left with a material capital loss at maturity (because the purchase price may be above the redemption price). Therefore we always recommend investors look at the yield to maturity. This is an accurate measure of yield over the life of the security. Having established this, what is the lowest risk security?c The truth is that you cannot easily do this without doing some background analysis on both. In our analysis we standardise measures of default risk to compare one security versus another. In the chart below you can see that as the risk score of the issue increases (that is going from left to right across the x-axis) the probability of the issuer defaulting (i.e. not meeting its obligations to pay the security holder or other creditors) increases. The key here is that the risk is not linear – its exponential and the further up the risk curve you go the more analysis is required.  So where do bank hybrids fit on this curve? Historically bank hybrids ranked between 8 and 10 on this curve but more recently issued securities (i.e. the Basel III complaint issues) are more complex. Holders of these instruments actually convert to equity prior to default (known as the non-viability and capital triggers). But does this make them more risky? Not necessarily – the banks run highly sophisticated risk models and have access to capital markets to offset potential risks whereas Corporate A, ranked in the extreme risk category, does not have these risk mitigants and any operating failure is likely to result in a restructure or default. Does this suggest that bank hybrid is lower risk? Again not necessarily. The management team of a strong high yield corporate issuer is working hard to push down the risk curve (i.e. from right to left). This will reduce their cost of funding (and capital) which will in turn mean shareholders will be happy. On the other hand a poorly managed high yield corporate issuer will be going the other way and struggle to avoid default. Confused? This is why independent credit analysis is important. If you exclude valuation, we generally prefer a high yield corporate with an improving outlook over a bank hybrid with a deteriorating outlook because the issuers are moving in opposite directions along the credit risk curve and could potentially meet in the middle. What about valuation? Both securities are effectively offering the same yield to maturity. But Bank A is much lower on the credit risk scale than corporate B. Therefore, we recommend Bank A Capital Security over Corporate B Security. The key to credit investing is picking the issuers (and securities) which are moving from right to left on the credit risk scale. Successfully picking these securities will maximize your return while reducing credit risk…..its not as simple as it looks!

So where do bank hybrids fit on this curve? Historically bank hybrids ranked between 8 and 10 on this curve but more recently issued securities (i.e. the Basel III complaint issues) are more complex. Holders of these instruments actually convert to equity prior to default (known as the non-viability and capital triggers). But does this make them more risky? Not necessarily – the banks run highly sophisticated risk models and have access to capital markets to offset potential risks whereas Corporate A, ranked in the extreme risk category, does not have these risk mitigants and any operating failure is likely to result in a restructure or default. Does this suggest that bank hybrid is lower risk? Again not necessarily. The management team of a strong high yield corporate issuer is working hard to push down the risk curve (i.e. from right to left). This will reduce their cost of funding (and capital) which will in turn mean shareholders will be happy. On the other hand a poorly managed high yield corporate issuer will be going the other way and struggle to avoid default. Confused? This is why independent credit analysis is important. If you exclude valuation, we generally prefer a high yield corporate with an improving outlook over a bank hybrid with a deteriorating outlook because the issuers are moving in opposite directions along the credit risk curve and could potentially meet in the middle. What about valuation? Both securities are effectively offering the same yield to maturity. But Bank A is much lower on the credit risk scale than corporate B. Therefore, we recommend Bank A Capital Security over Corporate B Security. The key to credit investing is picking the issuers (and securities) which are moving from right to left on the credit risk scale. Successfully picking these securities will maximize your return while reducing credit risk…..its not as simple as it looks!