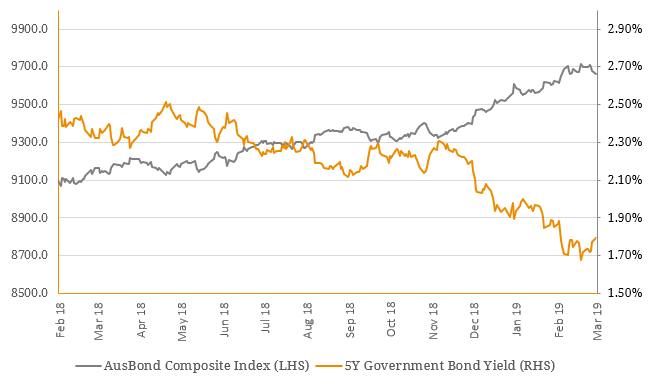

If you have been keeping up to date with comments about and from the Reserve Bank in 2019, you have almost certainly heard speculation about a possible cash rate cut. Though the RBA has stated that the cash rate is ‘expected to remain unchanged for a considerable period’, the February shift to a ‘more evenly balanced’ stance on any cash rate changes implies that Australian investors should at least be prepared for a lower cash rate. Although there have been a number of shifts to the downside, current overall market consensus is that Australian investors should now be generally preparing for a cash rate move in either direction (it at all in our view). Already at its lowest level in over half a century, the effects of further cash rate cuts could be far reaching. Markets do have plenty of recent data on this type of directional change, with the RBA having progressively cut the target cash rate from its recent high of 4.75% in October 2011. However, what might be prevalent is the magnitude of such an event given how low rates are now; a reduction of 25 basis points (0.25%) from 1.50% is relatively more impactful than a 25 basis point cut from 4.75%. Australian investors should consider what effects a falling interest rate environment would have on Additional Tier 1 (AT1) hybrids. Traditional fixed income instruments possess an inverse relationship with interest rates. Specifically, fixed rate bonds will decrease in value in a rising interest rate environment and increase in value in a decreasing interest rate environment. This correlation represents an instrument’s price sensitivity to underlying movements in interest rates, referred to as ‘duration’. Evidence can be easily found demonstrating this relationship throughout the past year, where interest rate volatility has been negatively correlated to the flagship AusBond Composite Index, which is comprised of almost 100% fixed rate securities (Figure 1). Figure 1. AusBond Composite Index v 5Y Government Bond Yield  Source: BondAdviser, Bloomberg The reason for this inverse correlation is comparative market yield sensitivity – when market interest rates rise above a security’s (fixed) coupon rate over the same tenor, the market will be offering a superior yield to the instrument. The result is a decline in security value, reflected by a falling price below par. The same correlation is present in the inverse scenario, with rate cuts increasing the fixed rate security’s attractiveness compared with current market yields, causing a price increase. This sensitivity to interest rate changes increases for longer-term instruments; the duration of the AusBond Government Bond Index has historically always been higher than the AusBond Corporate Credit Index, which includes relatively shorter-dated corporate bonds (Figure 2). Figure 2. Duration of AusBond Indices

Source: BondAdviser, Bloomberg The reason for this inverse correlation is comparative market yield sensitivity – when market interest rates rise above a security’s (fixed) coupon rate over the same tenor, the market will be offering a superior yield to the instrument. The result is a decline in security value, reflected by a falling price below par. The same correlation is present in the inverse scenario, with rate cuts increasing the fixed rate security’s attractiveness compared with current market yields, causing a price increase. This sensitivity to interest rate changes increases for longer-term instruments; the duration of the AusBond Government Bond Index has historically always been higher than the AusBond Corporate Credit Index, which includes relatively shorter-dated corporate bonds (Figure 2). Figure 2. Duration of AusBond Indices  Source: BondAdviser, Bloomberg However, as Figure 2 illustrates above, the duration of the AusBond Credit FRN Index has remained close to zero since inception, generally unaffected by the interest rate environment. This index comprises only floating rate securities where the coupon rate resets periodically (typically either quarterly or semi-annually). For this reason, any movements in interest rates will be soon captured when the floating rate component of the coupon next resets. Whilst the downside risk is removed should an interest rate rise occur so too is any possible price gains from an interest rate cut. Everything else being equal, should an interest rate cut appear more likely to occur, traditional fixed income securities will be seen as more attractive than those with a floating rate component. The above logic applies to all listed AT1 hybrid instruments which are floating rate (plus a margin). While interest rate duration remains low throughout the security’s term, it will follow a distinct pattern reflecting the decline in duration during the current coupon period before the floating rate resets. However, as demonstrated in Figure 2, duration is considerably lower in comparison to fixed rate securities. Figure 3. Example of AT1 Historical Hybrid Duration

Source: BondAdviser, Bloomberg However, as Figure 2 illustrates above, the duration of the AusBond Credit FRN Index has remained close to zero since inception, generally unaffected by the interest rate environment. This index comprises only floating rate securities where the coupon rate resets periodically (typically either quarterly or semi-annually). For this reason, any movements in interest rates will be soon captured when the floating rate component of the coupon next resets. Whilst the downside risk is removed should an interest rate rise occur so too is any possible price gains from an interest rate cut. Everything else being equal, should an interest rate cut appear more likely to occur, traditional fixed income securities will be seen as more attractive than those with a floating rate component. The above logic applies to all listed AT1 hybrid instruments which are floating rate (plus a margin). While interest rate duration remains low throughout the security’s term, it will follow a distinct pattern reflecting the decline in duration during the current coupon period before the floating rate resets. However, as demonstrated in Figure 2, duration is considerably lower in comparison to fixed rate securities. Figure 3. Example of AT1 Historical Hybrid Duration  Source: BondAdviser The interest rate environment may not be the largest driver of future AT1 hybrid valuations. As we have discussed previously, it may be that a more appropriate risk parameter is credit duration. In comparison to interest rate duration, credit duration measures an instrument’s sensitivity to changes in its trading margin (and perceived riskiness). We expect any RBA target cash rate movement to have a limited direct impact on hybrid valuations but any change will of course be reflected in new distribution rates and there will likely be tailwinds to equity valuations and possibly some lower demand in secondary trading. We continue to believe that BBSW rates will remain elevated relative to the cash rate, reflecting higher inter-bank borrowing costs and which directly benefit hybrid debt holders.

Source: BondAdviser The interest rate environment may not be the largest driver of future AT1 hybrid valuations. As we have discussed previously, it may be that a more appropriate risk parameter is credit duration. In comparison to interest rate duration, credit duration measures an instrument’s sensitivity to changes in its trading margin (and perceived riskiness). We expect any RBA target cash rate movement to have a limited direct impact on hybrid valuations but any change will of course be reflected in new distribution rates and there will likely be tailwinds to equity valuations and possibly some lower demand in secondary trading. We continue to believe that BBSW rates will remain elevated relative to the cash rate, reflecting higher inter-bank borrowing costs and which directly benefit hybrid debt holders.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.