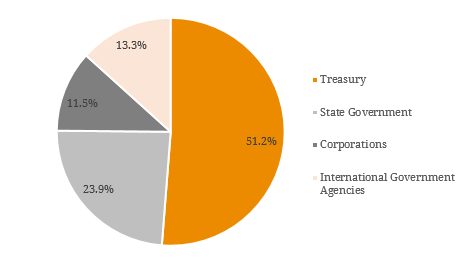

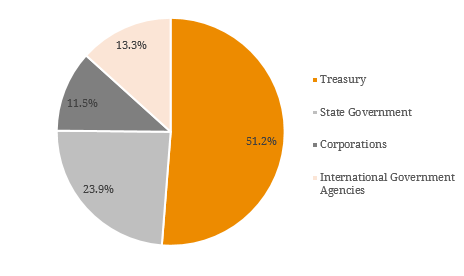

The Bloomberg AusBond Index Family is generally viewed as the leading benchmark for the Australian fixed income market and is used by asset managers, asset owners and investment consultants in Australia and across the world. It was originally developed by UBS and later acquired by Bloomberg as part of its expansion into the index industry. Media companies like Bloomberg are viewed as less conflicted custodians than banks of such relied-upon data since they have no obvious stake in the direction of prices. The index is available on the Bloomberg Professional service as well as on other distribution platforms. It includes more than 500 bonds that are used as benchmarks for the majority of fixed income portfolios in Australia. Bloomberg independently prices the index family using its evaluated pricing and will calculate and publish the indexes daily. As illustrated by Figure 1, the Bloomberg AusBond Composite Index focuses heavily on government and wholesale senior bonds and as a result, tracks the performance of the vast unlisted wholesale market. But what about the listed market? Currently, there is no market recognised standardised measure of performance for the ASX-Listed Debt & Hybrid Market making excess returns or relative performance difficult to quantify. Figure 1. Composition of AusBond Composite Index  Source: Bloomberg (June 2017) As an alternative, we have adopted a simple yet practical methodology whereby we use the RBA cash rate plus a margin as an approximate benchmark (RBA cash rate + 1.5% in our Income Plus Model Portfolio and RBA cash rate + 3% in our Income Opportunities Model Portfolio). As can be seen from the below charts, our RBA cash rate plus margin approach tracks our model portfolio performances but this benchmark is not a true reflection of the underlying market. Figure 2. Income Opportunities Portfolio Relative to Bloomberg Indices

Source: Bloomberg (June 2017) As an alternative, we have adopted a simple yet practical methodology whereby we use the RBA cash rate plus a margin as an approximate benchmark (RBA cash rate + 1.5% in our Income Plus Model Portfolio and RBA cash rate + 3% in our Income Opportunities Model Portfolio). As can be seen from the below charts, our RBA cash rate plus margin approach tracks our model portfolio performances but this benchmark is not a true reflection of the underlying market. Figure 2. Income Opportunities Portfolio Relative to Bloomberg Indices  Source: BondAdviser, Bloomberg Figure 2. Income Plus Portfolio Relative to Bloomberg Indices

Source: BondAdviser, Bloomberg Figure 2. Income Plus Portfolio Relative to Bloomberg Indices  Source: BondAdviser, Bloomberg Overall, the ASX-Listed Income Market primarily comprises hybrid securities which are typically floating rate, higher yielding and more volatile. As a blend of these debt and equity-like traits, market performance has not yet been standardised for all market participants which is needed to accurately track relative returns for accurate attribution and analysis.

Source: BondAdviser, Bloomberg Overall, the ASX-Listed Income Market primarily comprises hybrid securities which are typically floating rate, higher yielding and more volatile. As a blend of these debt and equity-like traits, market performance has not yet been standardised for all market participants which is needed to accurately track relative returns for accurate attribution and analysis.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.