On 10th January 2018, financial markets around the world took serious notice of reported “threats” from an unnamed Chinese official to slow down or halt the country’s US Treasury purchases. China, which holds approximately US$1.2 trillion of US Treasuries as part of its US$3.1 trillion in foreign exchange reserves and is America’s biggest creditor, is widely seen to be veiling the threat as a warning to the Trump administration, ahead of possible enactment of fresh import restrictions on Chinese steel and aluminium later in January. The two had been engaged in a bitter row in recent weeks over trade, a key political issue for both sides. On the same day, major listed Australian Real Estate Investment Trusts, or AREITs, almost uniformly lost ground. This included Vicinity Centres, Dexus, Abacus, Growthpoint, GPT, Stockland, Shopping Centres Australasia, Charter Hall Retail REIT and Mirvac ( figure 1). In fact, since the middle of December, listed property names have reversed with the key indicator, the S&P/ASX 200 AREIT, losing close to 6%. Figure 1: Major Listed AREITs (ASX Code)

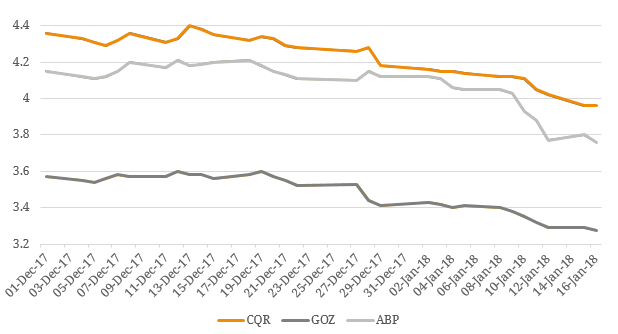

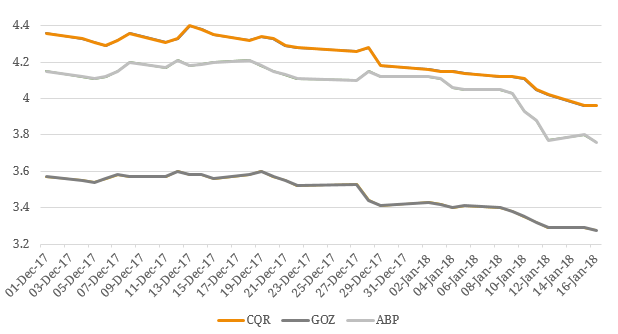

Source: BondAdviser, Bloomberg What links the US-China trade tension with the performance of AREITs? At the heart of the story is the broad correlation between government bonds and investments into bond proxies, typically property and infrastructure stocks. The level of broader interest rates, or bond yields, are the transmission mechanism between the two. Although the gradual upward trend in yields is now well known since the Fed started to gradually unwind its QE program, the benchmark US 10-year Treasury yield has hit a 10-month high of 2.59% following the Chinese threat. What’s more, Japan, the second largest creditor of the US, has also reduced its buying of US Treasuries this week and the ECB moved to cut its monthly bond-buying in half from January. The historic tax cut announced by Trump recently also adds to the growth environment and strengthens the case for rate rises in the US. As money exits from bonds, it also leaves the better-returning bond proxy stocks of real estate and infrastructure, as the discount rate used to value future rental income increases along with benchmark risk-free interest rates, for which government bonds are the common proxy. 10-year benchmark Australian government bond yields have tracked their US counterparts closely and have risen in a staggered fashion since December. As the US itself continues to raise its own rates and other developed economies such as Canada and the EU follow suit, pressure will eventually build for Australia to do the same (figure 2). Figure 2. Australian and US 10-Year Yields

Source: BondAdviser, Bloomberg What links the US-China trade tension with the performance of AREITs? At the heart of the story is the broad correlation between government bonds and investments into bond proxies, typically property and infrastructure stocks. The level of broader interest rates, or bond yields, are the transmission mechanism between the two. Although the gradual upward trend in yields is now well known since the Fed started to gradually unwind its QE program, the benchmark US 10-year Treasury yield has hit a 10-month high of 2.59% following the Chinese threat. What’s more, Japan, the second largest creditor of the US, has also reduced its buying of US Treasuries this week and the ECB moved to cut its monthly bond-buying in half from January. The historic tax cut announced by Trump recently also adds to the growth environment and strengthens the case for rate rises in the US. As money exits from bonds, it also leaves the better-returning bond proxy stocks of real estate and infrastructure, as the discount rate used to value future rental income increases along with benchmark risk-free interest rates, for which government bonds are the common proxy. 10-year benchmark Australian government bond yields have tracked their US counterparts closely and have risen in a staggered fashion since December. As the US itself continues to raise its own rates and other developed economies such as Canada and the EU follow suit, pressure will eventually build for Australia to do the same (figure 2). Figure 2. Australian and US 10-Year Yields  Source: BondAdviser, Bloomberg Although whether current cap rates fully reflect the trajectory in interest rates is up for investors’ own judgements, understanding the relationship between bond proxies and what’s happening to the wider world economy is very important in the increasingly inter-connected world that we live in today.

Source: BondAdviser, Bloomberg Although whether current cap rates fully reflect the trajectory in interest rates is up for investors’ own judgements, understanding the relationship between bond proxies and what’s happening to the wider world economy is very important in the increasingly inter-connected world that we live in today.

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Jul 28, 2026 Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Jul 28, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.