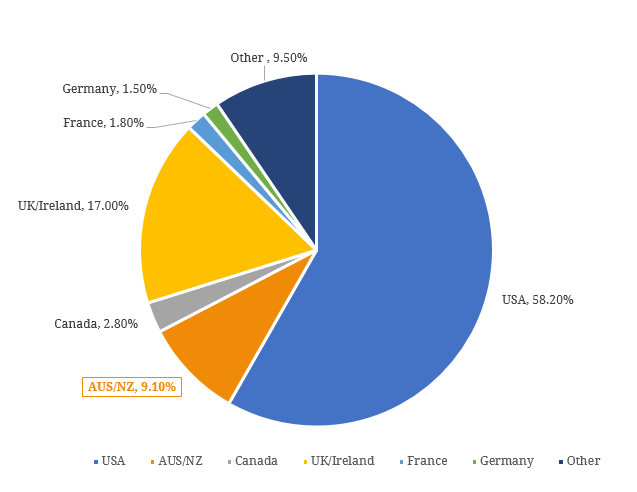

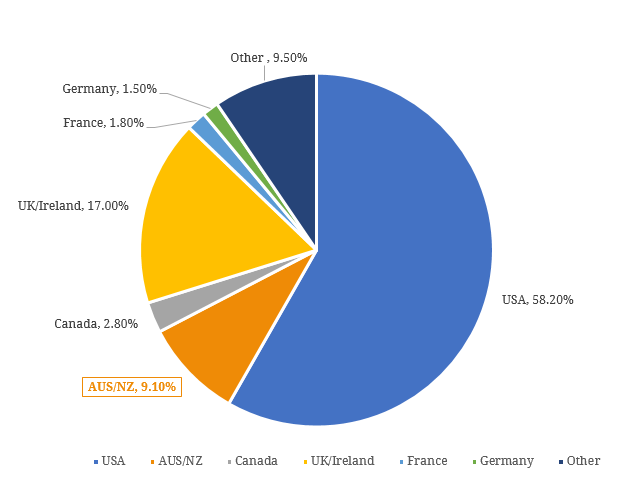

Tabcorp recently announced that it had successfully priced US$1.4 billion long-term notes to investors in the US Private Placement (USPP) market. The placement comprises four USD and two AUD-denominated tranches, with maturities evenly spaced between 8 – 18 years. The notes will be issued in June 2018. All USD proceeds will be swapped into AUD, resulting in total AUD proceeds of $1.82 billion, and which will be used to fully repay the $1.8 billion bridge financing facility put in place for the Tatts acquisition as well as to repay existing bank debt. Assuming reasonable pricing, this successful USPP deal is positive for the new Tabcorp, giving it long-term stable debt funding at lower costs. Whilst the acronym USPP may not be a household term in Australia, it is not unusual to hear news of Australian corporates tapping into the USPP market, leading some to ask – what is the USPP market for issuers and investors? The USPP is a market for privately issued debts in the US. Although it is well established, it is still only a fraction of the total size of the public fixed income market (~5%) and generally receives much less attention from the investing public. Whilst public corporate bonds are almost always rated by credit ratings agencies, USPP market debt is often not. This has led to some often incorrect assumptions of lower quality and higher credit risks of USPP bonds. In fact, many issuers in the USPP market are investment grade rated and it is not uncommon to see them issue debt in both the public bond market and in the USPP market. For issuers who are not rated, they are generally well-established corporates which could be investment grade if they chose to be so. This helps to also explain why predominant investors in the USPP market are insurance companies with low risk tolerance thus it is important not to confuse USPP debt with mezzanine debt or private equity. This nature of the USPP market means that there is usually low or little credit risk premia associated with USPP issuances. There is often, however, an illiquidity premium associated with USPP debt, which can range anywhere between 10 to 50 bps or more over similar-quality, public market bonds. This is despite the fact that liquidity typically is available and a secondary market for USPP debt does exist. This has led to many to label the illiquidity premium as a “perceived” one. On the other hand, there might be some merit in arguing that due to the relatively small size and market participant constraints of the USPP market, a small “perceived” illiquidity premium might be justified. The most important fact about the USPP market, amongst its other features, is its flexibility. Almost every aspect of a bond’s structure can be negotiable: issuers may issue in multiple currencies, with multiple maturities, in customised repayment structures or covenants, just to name a few. In essence, the USPP market determines on a case-by-case basis what such flexibility may cost the issuer. It is thus not surprising that the flexibility offered by the USPP market has attracted issuers with a broad range of needs that may not fall under the “conventional issuance” band. This is exemplified by the Tabcorp issuance – multiple currency tranches (USD and AUD), multiple maturity tranches (8 – 18 years) and for the purpose of funding a major acquisition (or refinance of), rather than the usual purposes of working capital and/or general corporate use. In fact, Australian corporates have been fairly active in the USPP market, well known Australian names such as TransGrid, Monash University, WorleyParsons, Charter Hall, FMG, Scentre, Brisbane Airport and ConnectEast have all been issuers before. Joining Australian issuers are other non-American names, which together frequently comprise almost 50% of total issuances (see Figure 1). Figure 1. Issuer Composition in USPP Market  Source: BondAdviser, PPM DataField Apart from flexibility, the depth and cost of the USPP market are also key considerations for Australian CFOs. Firstly, Australian corporates have long relied heavily on borrowings from local Australian banks, which have traditionally lacked the appetite to lend for very long-term maturities, whereas in the USPP market, bond tenors of 10 years or longer are common. Secondly, the cost of borrowing in the USPP market, although higher than the US public debt market due to the above-mentioned reasons, can usually still be lower than Australian bank borrowings. In the current environment, where Australian banks are under increased prudential regulations and higher cost of capital, this cost advantage has become an increasingly important consideration for Australian CFOs. Whilst the USPP market offers a range of benefits that are attractive to Australian borrowers, it is not without its risks. Underwriting in USPP debt is rare, so most issuers don’t have the peace of mind from investor commitments before pricing, which is by nature volatile, thus timing can be of a bigger factor for an issuance to succeed. It has been common practice for Australian corporates to initially use traditional local bank facilities for major corporate activities, such as funding an acquisition or a major Capex investment, as a temporary or bridging measure, then after the corporate event is complete and de-risked, tap the USPP market for longer term, stable and cheaper “anchor” debt funding. We have seen this model widely used by Australian infrastructure and mining companies, who have often funded the construction stages of major projects with syndicated local Australian bank loans, for 5-7 years, and, post successful completion, refinance the local bank loans with USPP bonds for the remainder of the project’s operational life, usually for another 10 – 20 years. On the investor side, many US life insurers such as MetLife, AIG and Prudential have found that these high-quality, long-term Australian infrastructure & utility issuances work well in matching their expected obligations with added geographical diversification benefits. In summary, there is good reason for Australian CFOs to keep a watchful eye on the USPP market. Since March this year, the local Bank Bill Swap Rate has risen sharply, from ~1.80% at the start of the month to around 2.00% as we type, reflecting higher bank funding costs (see Figure 2), coupled with slow loan growth in the competitive environment and potential negative ramifications from the banking Royal Commission. Borrowing from local banks is likely to become more expensive, potentially further increasing the attractiveness of USPP debt. However, US interest rates are also on the rise which will have the opposite effect, making the dynamic very interesting for the next few Australian issuers thinking of heading to the US. Figure 2. Australian Bank Borrowing Costs – BBSW

Source: BondAdviser, PPM DataField Apart from flexibility, the depth and cost of the USPP market are also key considerations for Australian CFOs. Firstly, Australian corporates have long relied heavily on borrowings from local Australian banks, which have traditionally lacked the appetite to lend for very long-term maturities, whereas in the USPP market, bond tenors of 10 years or longer are common. Secondly, the cost of borrowing in the USPP market, although higher than the US public debt market due to the above-mentioned reasons, can usually still be lower than Australian bank borrowings. In the current environment, where Australian banks are under increased prudential regulations and higher cost of capital, this cost advantage has become an increasingly important consideration for Australian CFOs. Whilst the USPP market offers a range of benefits that are attractive to Australian borrowers, it is not without its risks. Underwriting in USPP debt is rare, so most issuers don’t have the peace of mind from investor commitments before pricing, which is by nature volatile, thus timing can be of a bigger factor for an issuance to succeed. It has been common practice for Australian corporates to initially use traditional local bank facilities for major corporate activities, such as funding an acquisition or a major Capex investment, as a temporary or bridging measure, then after the corporate event is complete and de-risked, tap the USPP market for longer term, stable and cheaper “anchor” debt funding. We have seen this model widely used by Australian infrastructure and mining companies, who have often funded the construction stages of major projects with syndicated local Australian bank loans, for 5-7 years, and, post successful completion, refinance the local bank loans with USPP bonds for the remainder of the project’s operational life, usually for another 10 – 20 years. On the investor side, many US life insurers such as MetLife, AIG and Prudential have found that these high-quality, long-term Australian infrastructure & utility issuances work well in matching their expected obligations with added geographical diversification benefits. In summary, there is good reason for Australian CFOs to keep a watchful eye on the USPP market. Since March this year, the local Bank Bill Swap Rate has risen sharply, from ~1.80% at the start of the month to around 2.00% as we type, reflecting higher bank funding costs (see Figure 2), coupled with slow loan growth in the competitive environment and potential negative ramifications from the banking Royal Commission. Borrowing from local banks is likely to become more expensive, potentially further increasing the attractiveness of USPP debt. However, US interest rates are also on the rise which will have the opposite effect, making the dynamic very interesting for the next few Australian issuers thinking of heading to the US. Figure 2. Australian Bank Borrowing Costs – BBSW  Source: BondAdviser, Bloomberg

Source: BondAdviser, Bloomberg

An employee-owned financial services provider focused on the Debt Capital Markets.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Jun 22, 2026Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Jun 22, 2026Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.