Last week’s highlight was the announcement on Monday of the replacement of CBA’s PERLS III issue (due for rollover/redemption in April ’16) with the replacement Tier 1 PERLS VIII (indicated interest margin 5.20-5.35%, first call Oct 2021) due for settlement 31st March 2016. Prior to the announcement, the market had seen a protracted ‘blowout’ in hybrid trading margins of the four major banks to 5.80% plus. Following the announcement there was significant secondary market buying despite some negative sentiment towards the indicated issue margin. As an example PERLS VII narrowed from a margin of 5.80% over swap to 5.20% during the week. The question here is whether investors feel the margins on Tier 1 hybrids have peaked and represent value or whether further supply will again put pressure on hybrid margins. In an interesting article from Bloomberg this week they outlined that the average cost of new debt issued by the four largest lenders in Australia last week climbed to 0.29% more than the four largest American banks. This is the widest gap on record (since 2004) and is a result of a number of factors including the expectation of high issuance, a cheap hedge against the resource sector and China but also a major shift in bank regulations globally. In our opinion senior debt issued by Australia is unlikely to ever be “bailed in” and therefore widening spreads represent an opportunity to enter a defensive sector at a reasonable price.  Reporting Season We are now approximately 50% through reporting season and results to date have maintained reasonable momentum with no major surprises from companies we cover. Reporting this week: 22/02/2016 – G8 Education Limited 22/02/2016 – PMP Ltd 22/02/2016 – BHP Billiton Ltd 23/02/2016 – Caltex Australia Ltd 23/02/2016 – McPherson’s Ltd 23/02/2016 – Qantas Airways Ltd 24/02/2016 – APA Group 24/02/2016 – Wesfarmers Ltd 25/02/2016 – Crown Resorts Ltd 25/02/2016 – Ramsay Health Care Ltd 25/02/2016 – Seven Group Holdings Ltd 26/02/2016 – Woolworths Ltd

Reporting Season We are now approximately 50% through reporting season and results to date have maintained reasonable momentum with no major surprises from companies we cover. Reporting this week: 22/02/2016 – G8 Education Limited 22/02/2016 – PMP Ltd 22/02/2016 – BHP Billiton Ltd 23/02/2016 – Caltex Australia Ltd 23/02/2016 – McPherson’s Ltd 23/02/2016 – Qantas Airways Ltd 24/02/2016 – APA Group 24/02/2016 – Wesfarmers Ltd 25/02/2016 – Crown Resorts Ltd 25/02/2016 – Ramsay Health Care Ltd 25/02/2016 – Seven Group Holdings Ltd 26/02/2016 – Woolworths Ltd

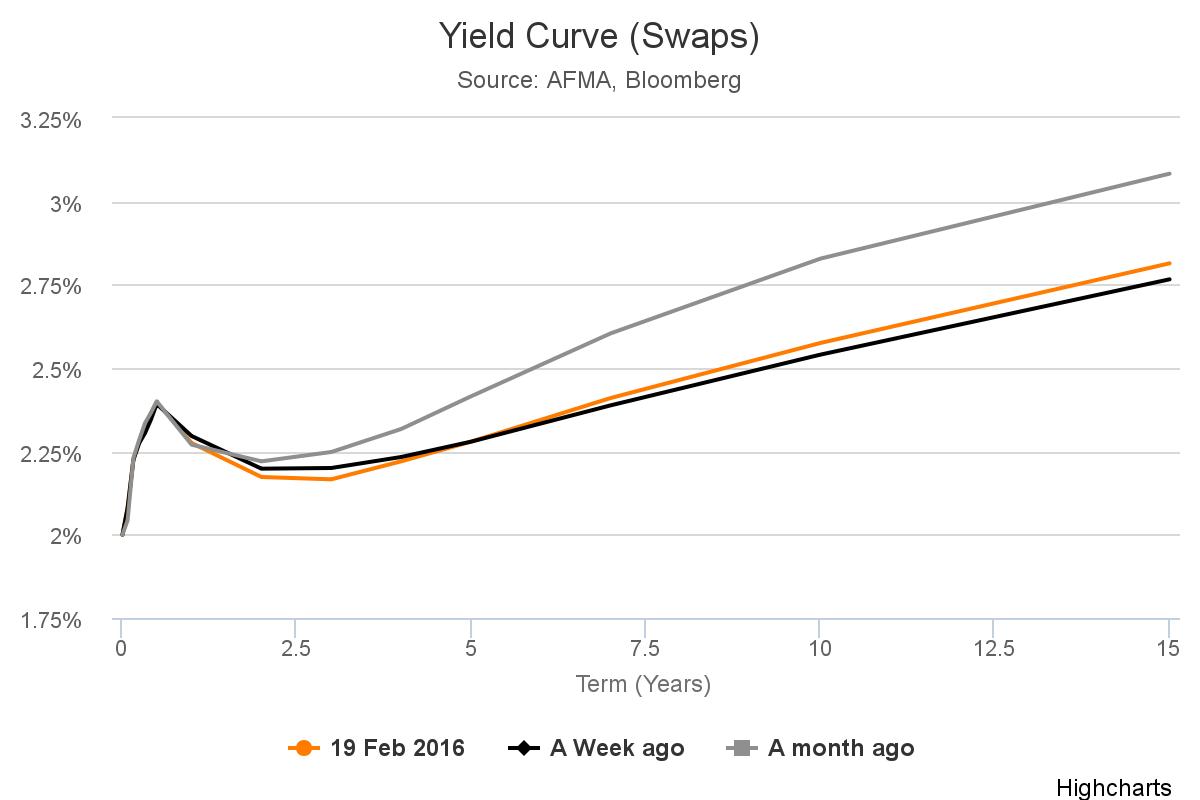

Click below for Interactive Charts Chart 1: Bloomberg AUSBond Composite Index (Monthly) Chart 2: Bonds vs Equities 2014/15 (Monthly) Interest Rates As stated last week interest rate expectations remain in a state of flux. The US Federal Reserve is facing increasing pressure from interest rate markets to adjust down its plan for future interest rate rises. However, there is no guarantee policy makers will change their position and hence volatility is likley to persist in the short term. Some of this uncertainty was resolved late last week in the Federal Reserve Chairman’s address to Capitol Hill but there is now news flow about negative interest rates and further quantitative easing. While this may be fact in some countries we don’t think the US will reverse its policy decision in the short term. The RBA continues to sit on the fence and follow the trajectory of employment, credit and inflation data. On Tuesday last week the minutes to the last Reserve Bank board meeting were released and the result was much of the same rhetoric with low inflation providing scope to ease policy but for the moment they are happy watching the employment trend and fincial market turbulence. In February 2015, the 10-year bond yield hit an all-time low of 2.27% before lifting to highs near 3.15% on 11 June 2015. In early November 2015 there was a progressive increase in yield from ~2.60% to a high of 2.99%. However, since mid-December the flight to quality has meant the 10-year yield has given back the changes in Q4 2015 and on 11 February 2016 hit a 6 month low of 2.37% (current 2.46%). The 3-year bond has followed a similar pattern and broke out of its recent yield range (1.90 – 2.1%) in November/December 2015 reaching a high of 2.18% on 7 December 2015. It has now retraced back to 1.80%. On 19 February 2016, the ASX 30 Day Interbank Cash Rate Futures March 2016 contract was trading at 98.02 indicating a 8% expectation of an interest rate decrease to 1.75% at the next RBA Board meeting (down from 19% previous week).